বিটকয়েনের বহু নির্দেশক সমন্বিত দৈনিক ট্রেডিং কৌশল

সারসংক্ষেপ

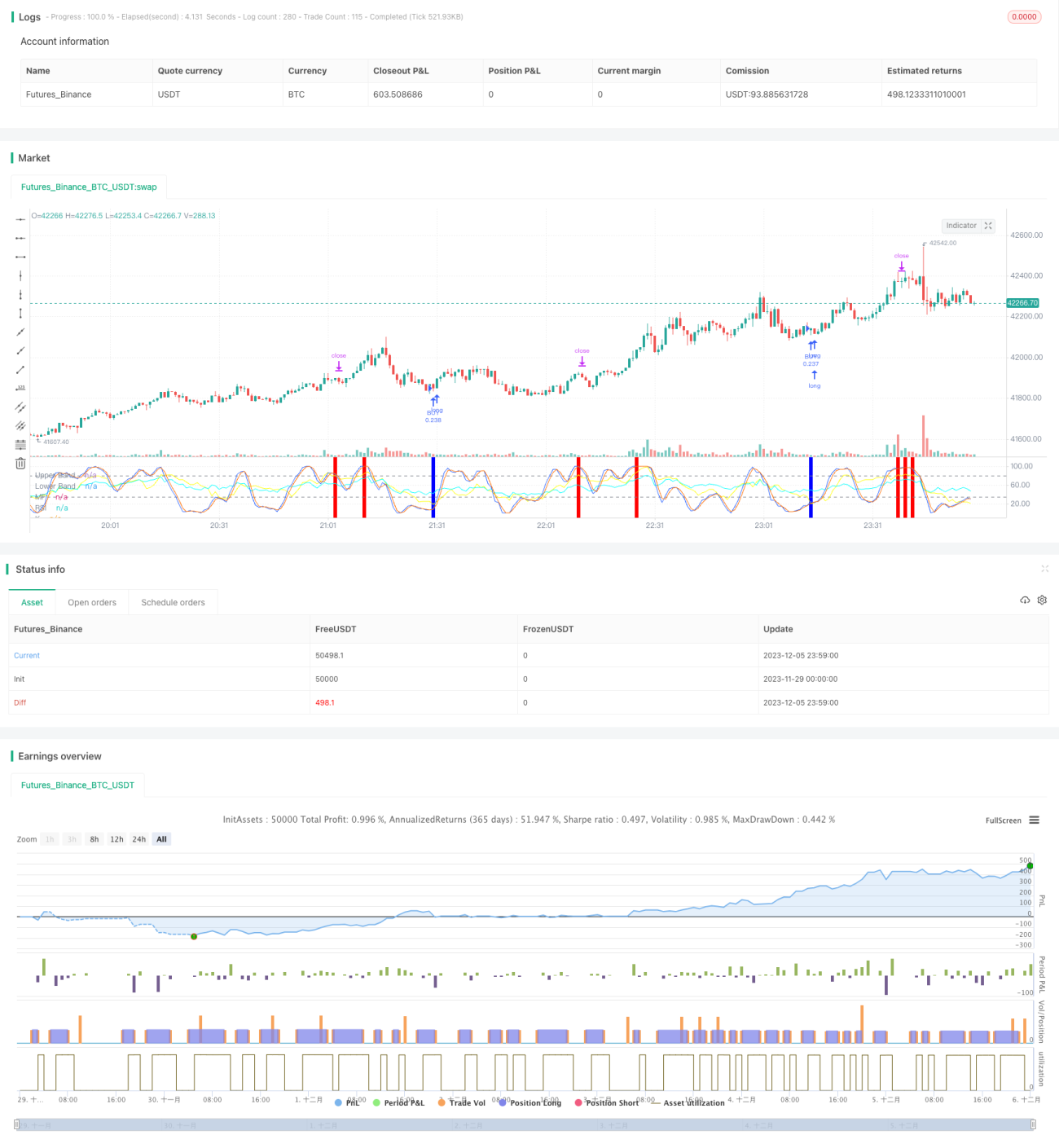

এই কৌশলটি RSI, MFI, Stoch RSI এবং MACD – এই চারটি সূচককে একত্রিত করে বিটকয়েনের ইন্ট্রাডে ট্রেডিং পরিচালনা করে। যখন একাধিক সূচক একইসাথে ক্রয় বা বিক্রয় সংকেত দেয়, তখনই কৌশলটি অর্ডার দেয়, যাতে ঝুঁকি নিয়ন্ত্রণ করা যায়।

কৌশলের মূলনীতি

-

RSI সূচক বাজার ওভারবট বা ওভারসোল্ড কিনা তা নির্ধারণ করতে ব্যবহৃত হয়। RSI ৪০-এর নিচে থাকলে ক্রয় সংকেত, এবং ৭০-এর উপরে থাকলে বিক্রয় সংকেত তৈরি হয়।

-

MFI সূচক বাজারের অর্থপ্রবাহ নির্ধারণ করে। MFI ২৩-এর নিচে থাকলে ক্রয় সংকেত, এবং ৮০-এর উপরে থাকলে বিক্রয় সংকেত তৈরি হয়।

-

Stoch RSI সূচক বাজার ওভারবট বা ওভারসোল্ড কিনা তা নির্ধারণ করে। K লাইন ৩৪-এর নিচে থাকলে ক্রয় সংকেত, এবং ৮০-এর উপরে থাকলে বিক্রয় সংকেত তৈরি হয়।

-

MACD সূচক বাজারের প্রবণতা এবং momentum নির্ধারণ করে। ফাস্ট লাইন স্লো লাইনের নিচে থাকলে এবং কলাম নেগেটিভ হলে ক্রয় সংকেত, বিপরীত অবস্থায় বিক্রয় সংকেত তৈরি হয়।

সুবিধা বিশ্লেষণ

-

চারটি প্রধান সূচক একত্রিত করে সংকেতের নির্ভুলতা বৃদ্ধি পায়, যা একক সূচকের ব্যর্থতার কারণে ক্ষতি এড়ায়।

-

শুধুমাত্র যখন একাধিক সূচক একইসাথে সংকেত দেয়, তখনই অর্ডার দেওয়া হয়, যার কারণে ভুয়া সংকেতের সম্ভাবনা ব্যাপকভাবে হ্রাস পায়।

-

ইন্ট্রাডে ট্রেডিং কৌশল ব্যবহার করা হয়, যা রাতারাতি ঝুঁকি এড়ায় এবং মূলধনের খরচ কমায়।

ঝুঁকি ও সমাধান

-

কৌশলের ট্রেডিং ফ্রিকোয়েন্সি কম হতে পারে, যার কারণে কিছু সময়গত ঝুঁকি থাকে। সূচকের প্যারামিটার সামান্য শিথিল করে ট্রেডের সংখ্যা বাড়ানো যেতে পারে।

-

সূচকগুলির ভুল সংকেত দেওয়ার সম্ভাবনা এখনও বিদ্যমান। মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে সূচক সংকেতের নির্ভরযোগ্যতা যাচাই করা যেতে পারে।

-

ওভারবট/ওভারসোল্ডের কিছু ঝুঁকি বিদ্যমান। সূচকের প্যারামিটার সামঞ্জস্য করে বা অন্য সূচকের যুক্তি যোগ করে তা নিয়ন্ত্রণ করা যেতে পারে।

অপ্টিমাইজেশনের দিক

-

অভিযোজিত সূচক প্যারামিটার ফিচার যুক্ত করা। বাজারের অস্থিরতা ও পরিবর্তনের গতির উপর ভিত্তি করে রিয়েল-টাইমে সূচকের প্যারামিটার সামঞ্জস্য করা।

-

স্টপ লস লজিক যুক্ত করা। যেমন নির্দিষ্ট শতাংশ ক্ষতি হলে স্টপ লস কার্যকর করে একক ট্রেডের ক্ষতি নিয়ন্ত্রণ করা।

-

আবেগ সূচক যুক্ত করা। বাজারের উত্তাপ, আতঙ্ক ইত্যাদি বহুমাত্রিক বিচার যোগ করে কৌশলের লাভের সম্ভাবনা বৃদ্ধি করা।

সারসংক্ষেপ

এই কৌশলটি চারটি প্রধান সূচকের পারস্পরিক যাচাইয়ের মাধ্যমে সংকেত জারি করে, যা ভুয়া সংকেতের হার কার্যকরভাবে হ্রাস করে। এটি তুলনামূলকভাবে স্থিতিশীল একটি উচ্চ-ফ্রিকোয়েন্সি লাভজনক কৌশল। প্যারামিটার ও মডেলের ক্রমাগত অপ্টিমাইজেশনের মাধ্যমে কৌশলের জয়ের হার ও লাভজনকতা আরও বাড়ানোর সম্ভাবনা রয়েছে।

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('John Day Stop Loss', overlay=false, pyramiding=1, default_qty_type=strategy.cash, default_qty_value=10000, initial_capital=10000, currency='USD', precision=2)

strategy.risk.allow_entry_in(strategy.direction.long) - 1