তিন-চার কে-লাইন ব্রেকআউট রিভার্সাল কৌশল

সংক্ষিপ্ত বিবরণ

তিন বা চার কে-লাইন ব্রেকআউট রিভার্সাল কৌশলটি উল্লেখযোগ্য ঊর্ধ্বমুখী গতি সম্পন্ন তিন বা চারটি কে-লাইন চিহ্নিত করে, তার পরবর্তী কয়েকটি ছোট পরিসরের কে-লাইন সমর্থন বা প্রতিরোধ গঠন করার পর, রিভার্সাল কে-লাইন ঘটলে বিপরীত প্রবণতায় বাণিজ্য করে। এটি একটি বিপরীত প্রবণতা ট্রেডিং কৌশল।

কৌশলের নীতি

এই কৌশলের মূল চিহ্নিতকরণ যুক্তি নিম্নলিখিত অংশগুলি নিয়ে গঠিত:

-

বর্ধিত পরিসরের কে-লাইন (গ্যাপ বার) চিহ্নিত করা: গড় ATR-এর 1.5 গুণ অতিক্রম করে এবং বডির অংশ 0.65-এর বেশি। এই কে-লাইনটির শক্তিশালী ঊর্ধ্বমুখী বা নিম্নমুখী গতি আছে বলে বিবেচিত হয়।

-

সংকুচিত পরিসরের কে-লাইন (কালেক্টিং বার) চিহ্নিত করা: গ্যাপ বারের পরে আসা 1-2টি ছোট পরিসরের ওঠানামা করা কে-লাইন, যার উচ্চ বা নিম্ন বিন্দু গ্যাপ বারের কাছাকাছি। এই কে-লাইনগুলি প্রবণতার মন্থরতা এবং সংহতকরণের প্রতিনিধিত্ব করে, যা সমর্থন বা প্রতিরোধ গঠন করে।

-

রিভার্সাল সিগন্যাল কে-লাইন চিহ্নিত করা: সংহতকরণ কে-লাইনের পরে, যদি এমন একটি কে-লাইন দেখা যায় যার বডি পূর্ববর্তী কয়েকটি কে-লাইনের উচ্চ বা নিম্ন বিন্দু ভেঙে দেয়, তাহলে এটি একটি রিভার্সাল সিগন্যাল হিসাবে বিবেচিত হয়। বডির দিক অনুসারে লং বা শর্ট করার সিদ্ধান্ত নেওয়া হয় এবং সেই কে-লাইনে পজিশন খোলা হয়।

-

স্টপ-লস এবং টেক-প্রফিট: স্টপ-লস গ্যাপ কে-লাইনের নিম্ন বিন্দুর নিচে বা উচ্চ বিন্দুর উপরে সেট করা হয়; টেক-প্রফিট স্টপ-লস বিন্দুকে নির্ধারিত লাভ-ক্ষতি অনুপাত দ্বারা গুণ করে নির্ধারিত হয়।

সুবিধা বিশ্লেষণ

এই কৌশলটির নিম্নলিখিত প্রধান সুবিধাগুলি রয়েছে:

-

কে-লাইনের নিজস্ব বৈশিষ্ট্য ব্যবহার করে প্রবণতা এবং রিভার্সাল পয়েন্ট নির্ধারণ করা, কোনো ইন্ডিকেটরের উপর নির্ভর করে না। এটি "ইন্ডিকেটর-মুক্ত" কৌশল হিসেবে কাজ করে।

-

গ্যাপ বার এবং কালেক্টিং বারের নির্বাচনের শর্ত কঠোর, যা কার্যকরভাবে প্রকৃত প্রবণতা এবং সংহতকরণ চিহ্নিত করতে পারে।

-

রিভার্সাল সিগন্যাল নির্ধারণে বডিকে মানদণ্ড হিসেবে ব্যবহার করা, যা মিথ্যা সিগন্যালের সম্ভাবনা হ্রাস করে।

-

মাত্র 3-4টি কে-লাইনের সমন্বয়ে একটি ট্রেড সম্পন্ন করা যায়, সময়কাল ছোট, ফ্রিকোয়েন্সি বেশি।

-

স্টপ-লস এবং টেক-প্রফিট স্পষ্টভাবে নির্ধারিত, ড্রডাউন এবং লাভ-ক্ষতি অনুপাত নিয়ন্ত্রণ করা সহজ।

ঝুঁকি বিশ্লেষণ

এই কৌশলটির নিম্নলিখিত কিছু ঝুঁকিও রয়েছে:

-

প্যারামিটার সেটিংয়ের মানের উপর নির্ভরশীল; যদি প্যারামিটার খুব আলগা হয়, তবে মিথ্যা সিগন্যাল এবং ক্ষতিকর ট্রেডের সম্ভাবনা বাড়ায়।

-

উচ্চ ফ্রিকোয়েন্সির মিথ্যা ব্রেকআউট দ্বারা সহজেই প্রভাবিত হয় এবং সমস্ত মিথ্যা সিগন্যাল কার্যকরভাবে ফিল্টার করতে পারে না।

-

আটকে পড়ার ঝুঁকি রয়েছে; যদি রিভার্সাল অপর্যাপ্ত হয় তবে সহজেই অ্যাডজাস্টমেন্ট তৈরি হয়, ফলে স্টপ-লস প্রয়োগ করা যায় না।

-

স্টপ-লসের পরিসর অপেক্ষাকৃত বড়, এবং বিরল আটকে পড়ার সুযোগ বড় ক্ষতির কারণ হতে পারে।

এই ঝুঁকিগুলি কমানোর জন্য নিম্নলিখিত দিকগুলি অপ্টিমাইজ করা যেতে পারে:

-

প্যারামিটার অপ্টিমাইজ করা, যাতে গ্যাপ বার এবং কালেক্টিং বার আরও নির্ভুলভাবে চিহ্নিত হয়।

-

ফিল্টার যোগ করা, রিভার্সাল কে-লাইন পুনরায় নিশ্চিত হওয়ার পর পজিশন খোলা।

-

স্টপ-লস অ্যালগরিদম অপ্টিমাইজ করা, যাতে স্টপ-লস দামের কাছাকাছি হয় এবং ক্ষতি আরও নিয়ন্ত্রণযোগ্য হয়।

অপ্টিমাইজেশনের দিকনির্দেশ

এই কৌশলটির আরও কয়েকটি প্রধান অপ্টিমাইজেশনের দিক রয়েছে:

-

যৌগিক ফিল্টার যোগ করা, মিথ্যা ব্রেকআউটের হস্তক্ষেপ এড়ানো। উদাহরণস্বরূপ, ভলিউম ইন্ডিকেটর যোগ করা, শুধুমাত্র ভলিউম বৃদ্ধি পেলে ট্রেড সিগন্যাল বিবেচনা করা।

-

মুভিং এভারেজ ইন্ডিকেটর যুক্ত করা, শুধুমাত্র দাম গুরুত্বপূর্ণ মুভিং এভারেজ (যেমন 20-দিন, 60-দিন) অতিক্রম করলে ট্রেড সিগন্যাল বিবেচনা করা।

-

বহু টাইমফ্রেম যাচাইকরণ, শুধুমাত্র একাধিক সময়কাল একসঙ্গে সিগন্যাল দিলে পজিশন খোলা।

-

টেক-প্রফিট শর্ত অপ্টিমাইজ করা, বাজারের অস্থিরতা এবং ঝুঁকি সহনশীলতা অনুযায়ী লাভ-ক্ষতি অনুপাত গতিশীলভাবে সামঞ্জস্য করা।

-

বাজারের ঊর্ধ্বমুখী/নিম্নমুখী অবস্থা নির্ণয় ব্যবস্থা যুক্ত করা, শুধুমাত্র ট্রেন্ডিং বাজারের পরিবেশে এই কৌশল ব্যবহার করা।

এই অপ্টিমাইজেশনগুলি কৌশলটির স্থিতিশীলতা এবং লাভের সম্ভাবনা আরও বৃদ্ধি করতে পারে।

সারসংক্ষেপ

তিন বা চার কে-লাইন ব্রেকআউট রিভার্সাল কৌশলটি উচ্চ-মানের প্রবণতা সম্ভাব্য অংশ এবং রিভার্সাল সিগন্যাল চিহ্নিত করে ট্রেড করে। অপারেশনের সময়কাল ছোট, ফ্রিকোয়েন্সি বেশি, এবং এটি প্রচুর অতিরিক্ত রিটার্ন অর্জনের সম্ভাবনা রাখে। একইসঙ্গে কিছু ঝুঁকিও রয়েছে, যা কমাতে এবং স্থিতিশীলতা বাড়াতে আরও অপ্টিমাইজেশন প্রয়োজন। সামগ্রিকভাবে, এই কৌশলটি বাজারের গঠনের নিজস্ব বৈশিষ্ট্য ব্যবহার করে প্রবণতা এবং রিভার্সাল পয়েন্ট নির্ধারণ করে, যা আরও গবেষণা এবং প্রয়োগের যোগ্য।

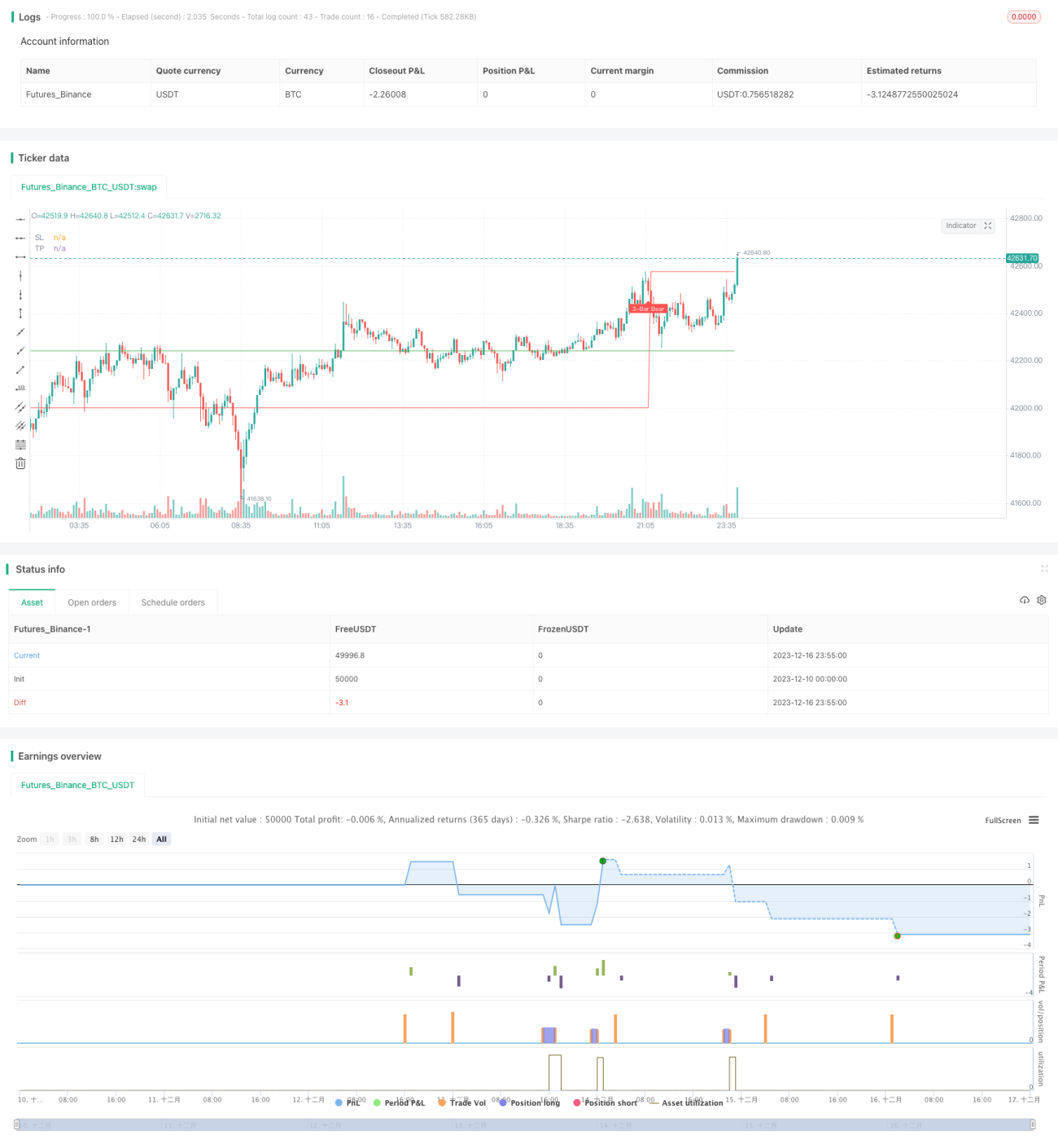

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Three (3)-Bar and Four (4)-Bar Plays Strategy", shorttitle="Three (3)-Bar and Four (4)-Bar Plays Strategy", overlay=true, calc_on_every_tick=true, currency=currency.USD, default_qty_value=1.0,initial_capital=30000.00,default_qty_type=strategy.percent_of_equity)

frommonth = input(defval = 1, minval = 01, maxval = 12, title = "From Month")- 1