গতিবেগ TD বিপরীতমুখী ট্রেডিং কৌশল

সারসংক্ষেপ

মোমেন্টাম টিডি রিভার্সাল ট্রেডিং কৌশলটি একটি পরিমাণগত ট্রেডিং কৌশল যা টিডি সিকোয়েন্সিয়াল সূচক ব্যবহার করে মূল্য বিপরীত সংকেত সনাক্ত করে। এই কৌশলটি মূল্য মোমেন্টাম বিশ্লেষণের উপর ভিত্তি করে তৈরি, এবং মূল্য বিপরীত সংকেত নিশ্চিত হওয়ার পরে লং বা শর্ট পজিশন খোলে।

কৌশল নীতি

এই কৌশলটি টিডি সিকোয়েন্সিয়াল সূচক ব্যবহার করে মূল্যের ওঠানামা বিশ্লেষণ করে এবং পরপর ৯টি ক্যান্ডেলস্টিকের মূল্য বিপরীত প্যাটার্ন সনাক্ত করে। বিশেষভাবে, যখন পরপর ৯টি ক্যান্ডেলস্টিকে মূল্য বৃদ্ধির পর একটি পতনশীল ক্যান্ডেলস্টিক দেখা যায়, তখন কৌশলটি শর্ট করার সুযোগ হিসেবে মূল্যায়ন করে; বিপরীতভাবে, যখন পরপর ৯টি ক্যান্ডেলস্টিকে মূল্য হ্রাসের পর একটি বৃদ্ধিশীল ক্যান্ডেলস্টিক দেখা যায়, তখন কৌশলটি লং করার সুযোগ হিসেবে মূল্যায়ন করে।

টিডি সিকোয়েন্সিয়াল সূচকের সুবিধা ব্যবহার করে, আগেভাগেই মূল্য বিপরীত সংকেত ধরা সম্ভব। এই কৌশলে নির্দিষ্ট সংখ্যক ট্রেন্ড ফলোয়িং (মোমেন্টাম) মেকানিজম যুক্ত থাকায়, বিপরীত সংকেত নিশ্চিত হওয়ার পর দ্রুত লং বা শর্ট পজিশন খোলা যায়, ফলে মূল্য বিপরীতের প্রাথমিক পর্যায়ে ভালো এন্ট্রি পয়েন্ট পাওয়া যায়।

সুবিধা বিশ্লেষণ

- টিডি সিকোয়েন্সিয়াল সূচক ব্যবহার করে আগেভাগেই মূল্য বিপরীতের সুযোগ শনাক্ত করা যায়

- ট্রেন্ড ফলোয়িং মেকানিজম থাকায় আরও সময়োপযোগীভাবে বিপরীত নিশ্চিতকরণ সম্ভব

- বিপরীত গঠনের পর্যায়ে পজিশন খোলার মাধ্যমে ভালো এন্ট্রি পয়েন্ট পাওয়া যায়

ঝুঁকি বিশ্লেষণ

- টিডি সিকোয়েন্সিয়াল সূচকে ভুয়া ব্রেকআউট হতে পারে, তাই অন্যান্য বিষয়ের সাথে সমন্বয় করে নিশ্চিত হতে হবে

- পজিশনের আকার এবং পজিশনের সময় যথাযথভাবে নিয়ন্ত্রণ করা প্রয়োজন, যাতে ঝুঁকি কমানো যায়

উন্নয়নের দিকনির্দেশনা

- বিপরীত সংকেত নিশ্চিত করার জন্য অন্যান্য সূচকের সাথে সমন্বয় করা, যাতে ভুয়া ব্রেকআউটের ঝুঁকি এড়ানো যায়

- একক ট্রেডের ক্ষতি নিয়ন্ত্রণের জন্য স্টপ-লস পদ্ধতি স্থাপন করা

- লাভের পরিমাণ এবং ঝুঁকি নিয়ন্ত্রণের মধ্যে ভারসাম্য বজায় রাখতে পজিশনের আকার এবং ধারণকাল অপ্টিমাইজ করা

সারসংক্ষেপ

মোমেন্টাম টিডি রিভার্সাল ট্রেডিং কৌশলটি টিডি সিকোয়েন্সিয়াল সূচকের মাধ্যমে আগেভাগেই মূল্য বিপরীত সনাক্ত করে এবং বিপরীত নিশ্চিত হওয়ার পর দ্রুত পজিশন খোলে, যা মোমেন্টাম ট্রেডারদের জন্য অত্যন্ত উপযুক্ত একটি কৌশল। এই কৌশলটির বিপরীত সুযোগ শনাক্ত করার সুবিধা রয়েছে, তবে ঝুঁকি নিয়ন্ত্রণের দিকে নজর দিতে হবে, যাতে ভুয়া ব্রেকআউটের কারণে বড় ক্ষতি এড়ানো যায়। আরও অপ্টিমাইজেশনের মাধ্যমে এটি একটি ঝুঁকি-প্রতিফলনে ভারসাম্যপূর্ণ ট্রেডিং কৌশল।

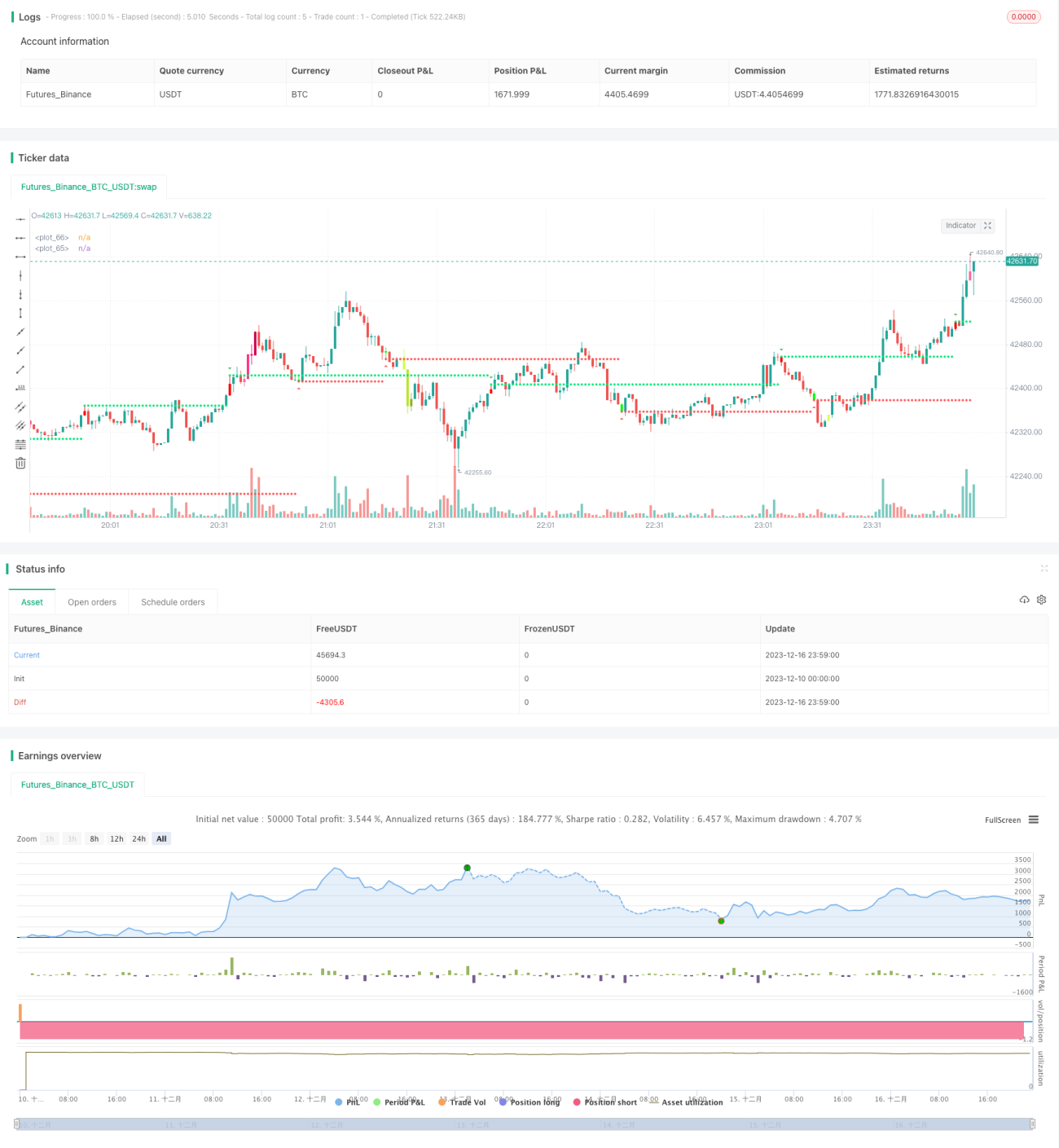

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//This strategy is based on TD sequential study from glaz.

//I made some improvement and modification to comply with pine script version 4.

//Basically, it is a strategy based on proce action, supports and resistance.- 1