দ্বৈত-ফ্যাক্টর পরিমাণগত বিপরীতমুখী ট্র্যাকিং কৌশল

সারসংক্ষেপ

এই কৌশলটি 123 প্যাটার্ন রিভার্সাল এবং সুপার অসিলেটর (Awesome Oscillator) - এই দুটি ফ্যাক্টরকে একত্রিত করে একটি দ্বি-ফ্যাক্টর কোয়ান্টিটেটিভ রিভার্সাল ট্র্যাকিং ট্রেডিং সিস্টেম তৈরি করে। এর মূল ধারণা হল বাজারের বিপরীতমুখী প্রবণতা শনাক্ত করার পাশাপাশি সুপার অসিলেটরের লং/শর্ট সিগন্যাল ব্যবহার করে আরও নির্ভুল এন্ট্রি টাইমিং নির্ধারণ করা।

এই কৌশলটি প্রধানত মিডিয়াম থেকে শর্ট-টার্ম রিভার্সাল ট্রেডিংয়ের জন্য উপযোগী। একাধিক ফ্যাক্টরের নিশ্চিতকরণের মাধ্যমে এটি মিথ্যা রিভার্সাল ফিল্টার করতে এবং সিগন্যালের গুণমান উন্নত করতে সাহায্য করে।

কৌশলের মূলনীতি

-

123 প্যাটার্ন রিভার্সাল

আগের দুই দিনের ক্লোজিং প্রাইস এবং বর্তমান ক্লোজিং প্রাইসের মধ্যে সম্পর্ক বিশ্লেষণ করে "উচ্চ-উচ্চ-নিম্ন" বা "নিম্ন-নিম্ন-উচ্চ" প্যাটার্ন তৈরি হয়, যা রিভার্সাল সিগন্যালের সম্ভাবনা নির্দেশ করে।

একই সাথে, Stochastic ইন্ডিকেটরকে ওভারবট বা ওভারসোল্ড জোনে থাকতে হবে, যা রিভার্সাল সিগন্যালকে আরও নিশ্চিত করে এবং মিথ্যা রিভার্সাল ফিল্টার করে।

-

Awesome Oscillator (সুপার অসিলেটর)

Awesome Oscillator একটি মোমেন্টাম-ভিত্তিক ইন্ডিকেটর যা মিডিয়াম-টার্ম ও শর্ট-টার্ম মুভিং এভারেজের পার্থক্য থেকে তৈরি হয়। যখন ফাস্ট লাইন স্লো লাইনকে উপর থেকে নিচে ক্রস করে, তখন এটি বিক্রির সংকেত; আর নিচ থেকে উপরে ক্রস করলে ক্রয়ের সংকেত।

এই কৌশলে এই ইন্ডিকেটরের লং/শর্ট অবস্থা ব্যবহার করে এন্ট্রি পয়েন্ট নির্ধারণ করা হয়।

-

দ্বি-ফ্যাক্টর নিশ্চিতকরণ

123 প্যাটার্ন রিভার্সাল এবং Awesome Oscillator - এই দুটি ফ্যাক্টরের সম্মিলিত নিশ্চিতকরণের মাধ্যমে মিথ্যা রিভার্সাল কার্যকরভাবে ফিল্টার করা যায় এবং এন্ট্রি টাইমিংয়ের নির্ভুলতা বাড়ে।

কৌশলের সুবিধা

-

রিভার্সাল পয়েন্ট চিহ্নিত করতে দ্বি-ফ্যাক্টর ব্যবহারের ফলে মিথ্যা রিভার্সাল সিগন্যাল কার্যকরভাবে ফিল্টার করা যায়।

-

Awesome Oscillator একটি মোমেন্টাম ইন্ডিকেটর হওয়ায় এটি এন্ট্রি টাইমিংয়ের সঠিকতা উন্নত করে।

-

Stochastic ইন্ডিকেটরের অন্তর্ভুক্তি টপে কিনতে বা বটমে বিক্রি করার ঝুঁকি এড়াতে সাহায্য করে।

-

রিভার্সাল কৌশল সাধারণত উচ্চতর জয়রেট এবং রিস্ক-রিওয়ার্ড অনুপাত প্রদান করে।

কৌশলের ঝুঁকি

-

রিভার্সাল ব্যর্থ হওয়ার ঝুঁকি এখনও বিদ্যমান। দ্বি-ফ্যাক্টর ব্যবহার করলেও এই ঝুঁকি সম্পূর্ণ এড়ানো যায় না, তবে সম্ভাবনা কমানো যায়।

-

অত্যধিক অপ্টিমাইজেশনের ঝুঁকি। ইন্ডিকেটর প্যারামিটার সেটিংস বিভিন্ন বাজারের জন্য পরীক্ষা ও অপ্টিমাইজ করতে হবে, যাতে অত্যধিক অপ্টিমাইজেশন এড়ানো যায়।

-

ট্রেন্ডের বিপরীতে ট্রেড করার ঝুঁকি। শক্তিশালী ট্রেন্ডের সময় রিভার্সাল কৌশল ক্ষতির কারণ হতে পারে। স্টপ লস ব্যবহার করে এই ঝুঁকি নিয়ন্ত্রণ করা যায়।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

ইন্ডিকেটর প্যারামিটার কম্বিনেশন পরীক্ষা ও অপ্টিমাইজ করে প্যারামিটারের রোবাস্টনেস বাড়ানো।

-

স্টপ লস কৌশল যুক্ত করে প্রতি ট্রেডে ক্ষতি সীমিত করা।

-

সেক্টর ও ইন্ডাস্ট্রি নির্বাচনের সঙ্গে সমন্বয় করে স্টক নির্বাচনের ত্রুটি এড়ানো।

-

হোল্ডিং পিরিয়ড অপ্টিমাইজ করে অন্ধ ট্র্যাকিংয়ের সমস্যা সমাধান করা।

-

বিভিন্ন মুভিং এভারেজ সিস্টেম পরীক্ষা করে সহায়ক শর্ত হিসাবে ব্যবহার করা।

সারাংশ

সার্বিকভাবে, এই দ্বি-ফ্যাক্টর কোয়ান্টিটেটিভ রিভার্সাল ট্র্যাকিং কৌশলটি একটি নির্দিষ্ট লাভের সম্ভাবনা ও রিস্ক-রিওয়ার্ড অনুপাত বজায় রেখে Awesome Oscillator-কে এন্ট্রি টাইমিং সহায়ক হিসাবে ব্যবহার করে এবং Stochastic ইন্ডিকেটরের মাধ্যমে টপে কিনতে বা বটমে বিক্রি করার ঝুঁকি এড়িয়ে রিভার্সাল ট্রেডিংয়ের ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করতে পারে। এটি অত্যন্ত ব্যবহারিক।

তবে রিভার্সাল কৌশলের নিজস্ব ঝুঁকি উপেক্ষা করা উচিত নয়। ঝুঁকি নিয়ন্ত্রণের জন্য ইন্ডিকেটর প্যারামিটার অপ্টিমাইজ করা, স্টপ লস শর্ত নির্ধারণ করা ইত্যাদি প্রয়োজন। সঠিকভাবে প্রয়োগ করলে এই কৌশল বিনিয়োগকারীদের জন্য স্থিতিশীল অতিরিক্ত রিটার্ন আনতে পারে।

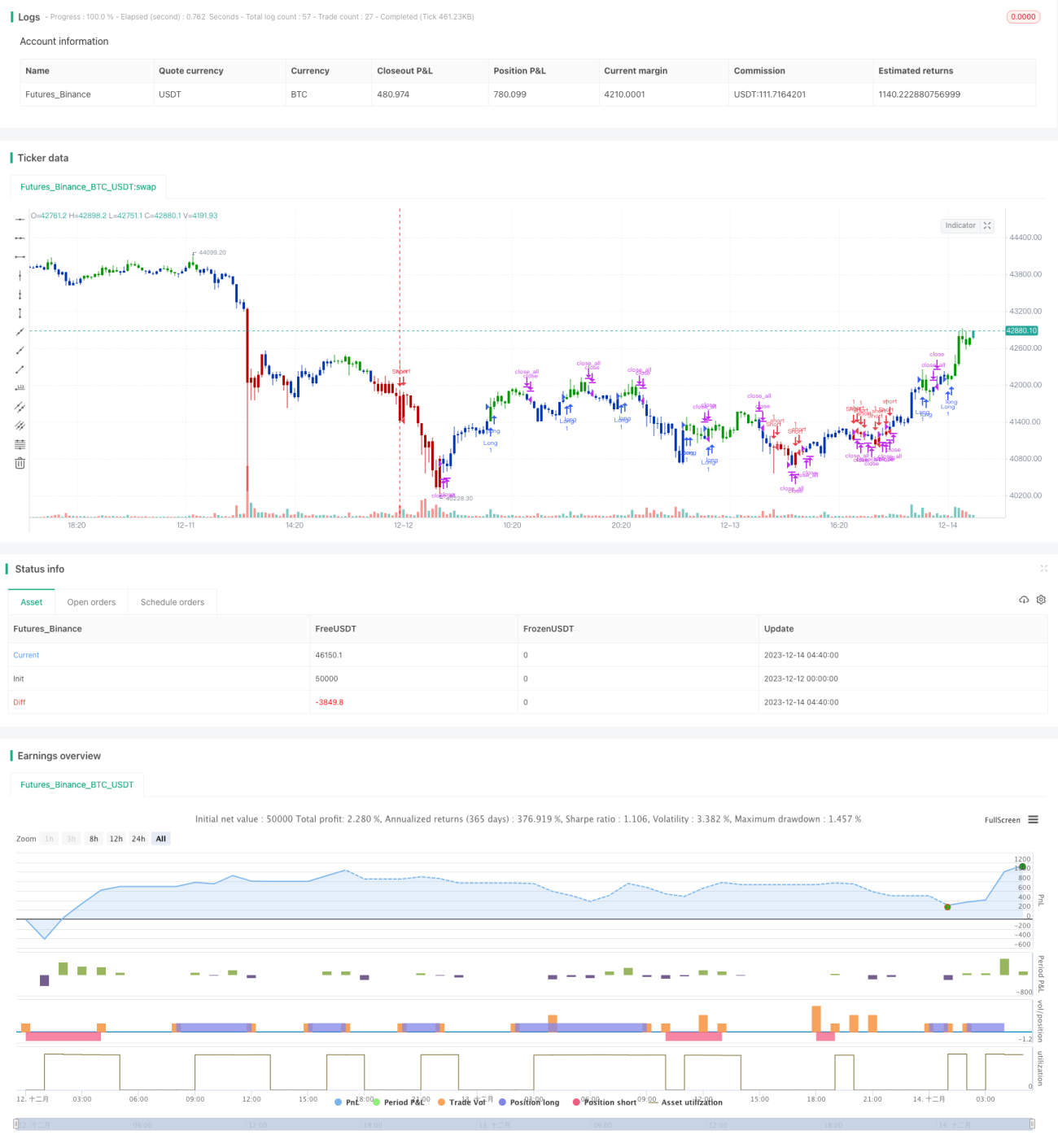

/*backtest

start: 2023-12-12 00:00:00

end: 2023-12-14 05:00:00

period: 20m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/08/2021

// This is combo strategies for get a cumulative signal. - 1