অভ্যন্তরীণ বার এবং মুভিং এভারেজের উপর ভিত্তি করে স্বয়ংক্রিয় পরিমাণগত ট্রেডিং কৌশল

সারসংক্ষেপ

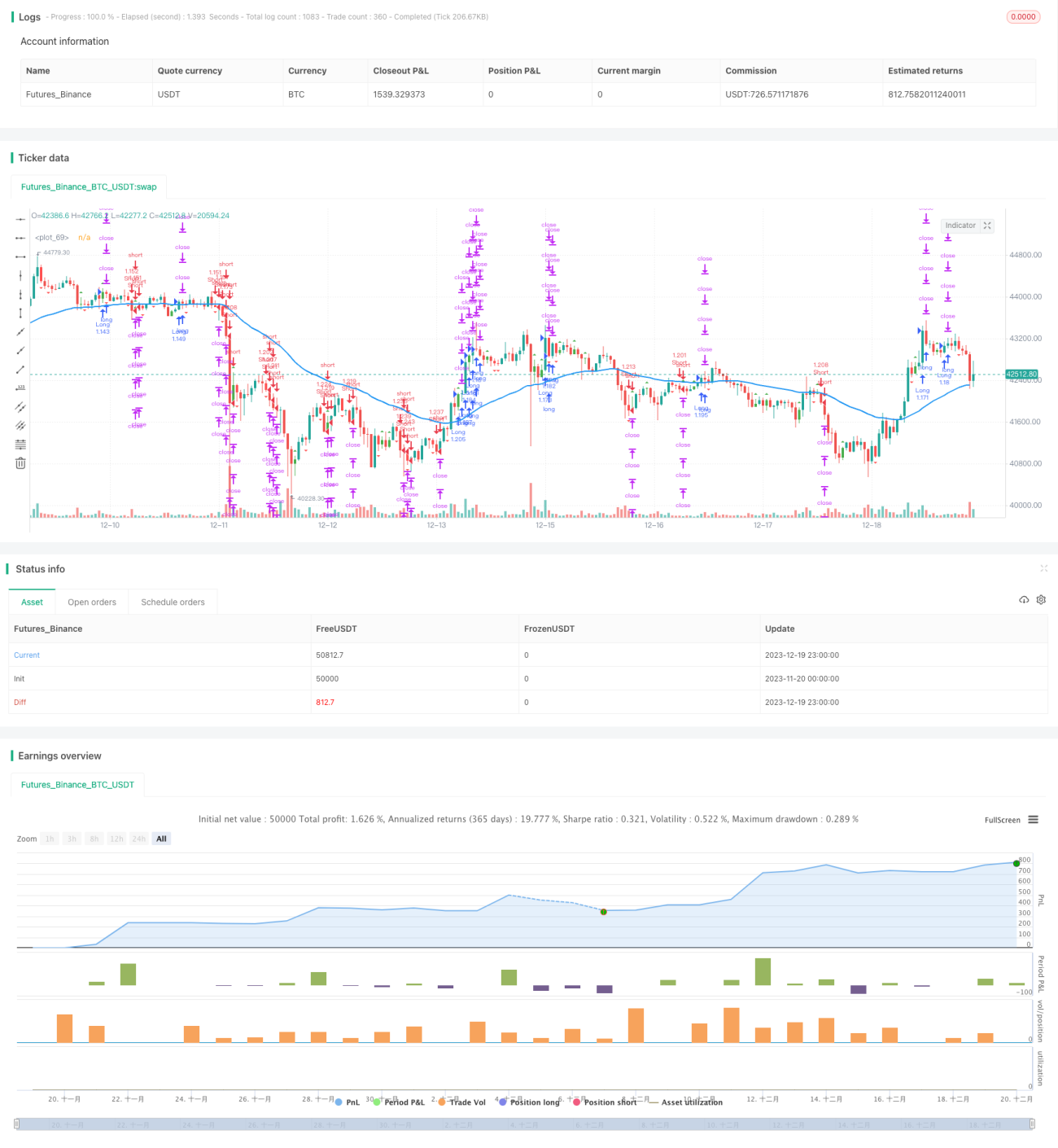

এই কৌশলের মূল ধারণা হলো অভ্যন্তরীণ বার প্যাটার্ন এবং মুভিং এভারেজ ইন্ডিকেটর একত্রিত করে স্বয়ংক্রিয় ট্রেডিং বাস্তবায়ন করা। যখন অভ্যন্তরীণ বার প্যাটার্ন দেখা যায়, এটি নির্দেশ করে যে বর্তমান ট্রেন্ডে পরিবর্তন হতে পারে, তখন আমরা মুভিং এভারেজের অবস্থান ব্যবহার করে চূড়ান্ত ট্রেডিং দিক নির্ধারণ করি।

কৌশলের নীতি

-

অভ্যন্তরীণ বার প্যাটার্ন খোঁজা। অভ্যন্তরীণ বার প্যাটার্ন বলতে বোঝায় যখন কোনো ক্যান্ডেলের সর্বোচ্চ এবং সর্বনিম্ন দাম পূর্ববর্তী ক্যান্ডেলের রিয়েল বডির মধ্যে থাকে। রিয়েল বডির রঙের ভিত্তিতে আমরা নির্ধারণ করতে পারি যে অভ্যন্তরীণ বারটি বুলিশ নাকি বেয়ারিশ।

-

মুভিং এভারেজের অবস্থান নির্ণয় করা। যখন অভ্যন্তরীণ বার প্যাটার্ন পাওয়া যায়, যদি দাম মুভিং এভারেজের উপরে থাকে তবে এটি বুলিশ সিগন্যাল, আর দাম মুভিং এভারেজের নিচে থাকলে এটি বেয়ারিশ সিগন্যাল।

-

অভ্যন্তরীণ বার প্যাটার্ন এবং মুভিং এভারেজের বুলিশ/বেয়ারিশ সিগন্যাল একত্রিত করে চূড়ান্ত ট্রেডিং দিক নির্ধারণ করা। অর্থাৎ, বেয়ারিশ অভ্যন্তরীণ বার যখন মুভিং এভারেজের নিচে ভেঙে যায় তখন শর্ট করা হয়, এবং বুলিশ অভ্যন্তরীণ বার যখন মুভিং এভারেজের উপরে ভেঙে যায় তখন লং করা হয়।

কৌশলের সুবিধা

-

টেকনিক্যাল ইন্ডিকেটর এবং প্রাইস প্যাটার্ন একত্রিত করে ট্রেডিং সিদ্ধান্তের নির্ভুলতা বৃদ্ধি করে।

-

অভ্যন্তরীণ বার প্যাটার্ন নিজেই শক্তিশালী দামের টার্নিং পয়েন্ট সংকেত ধারণ করে, যা ট্রেন্ডের টার্নিং পয়েন্ট আগেভাগে নির্ধারণ করতে সাহায্য করে।

-

মুভিং এভারেজ কিছু শব্দ ফিল্টার করে, যা রেঞ্জ বাউন্ড ট্রেডিংয়ে ফেঁসে যাওয়া এড়ায়।

-

সম্পূর্ণ স্বয়ংক্রিয় ট্রেডিং বাস্তবায়ন করে, যা ম্যানুয়াল ট্রেডিংয়ের সময় ও শ্রম খরচ ব্যাপকভাবে হ্রাস করে।

কৌশলের ঝুঁকি ও সমাধান

-

যখন দাম মুভিং এভারেজের কাছাকাছি ওঠানামা করে, তখন অনেক ভুল সংকেত দেখা দিতে পারে, ফলে অতিরিক্ত ট্রেডিং হতে পারে। মুভিং এভারেজের প্যারামিটার অপ্টিমাইজ করে বা অতিরিক্ত ফিল্টার শর্ত যোগ করে ভুল সংকেত কমানো যেতে পারে।

-

এই কৌশলটি তুলনামূলকভাবে স্পষ্ট ট্রেন্ডযুক্ত বাজারের জন্য বেশি উপযুক্ত; রেঞ্জ বাউন্ড বাজারে এর কার্যকারিতা কমে যেতে পারে। ADX-এর মতো ট্রেন্ড নির্ধারণকারী ইন্ডিকেটর ব্যবহার করে অ্যালগরিদম চালু করার শর্ত নিয়ন্ত্রণ করা যেতে পারে।

-

কিছু সময় ল্যাগ থাকে। প্যারামিটার সংক্ষিপ্ত করে বা মুভিং এভারেজের গণনা পদ্ধতি অপ্টিমাইজ করে ল্যাগ কমানো যেতে পারে।

-

ড্রডাউনের ঝুঁকি বেশি। স্টপ লস ব্যবহার করে ক্ষতির ঝুঁকি নিয়ন্ত্রণ করা যায় এবং উপযুক্ত পজিশন ম্যানেজমেন্টও ড্রডাউন কমাতে সাহায্য করে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

অভ্যন্তরীণ বার নির্ধারণের সময়কালের প্যারামিটার অপ্টিমাইজ করে সর্বোত্তম প্যারামিটার সমন্বয় খোঁজা।

-

বিভিন্ন ধরনের মুভিং এভারেজ যেমন EMA, SMA ইত্যাদি পরীক্ষা করে সবচেয়ে উপযুক্ত মুভিং এভারেজ ইন্ডিকেটর নির্ধারণ করা।

-

MACD, KDJ-এর মতো সহায়ক ইন্ডিকেটর যুক্ত করে বুলিশ/বেয়ারিশ নির্ধারণের ভিত্তি সমৃদ্ধ করা এবং সংকেতের নির্ভুলতা বৃদ্ধি করা।

-

ADX, ATR-এর মতো ফিল্টার ইন্ডিকেটর যোগ করে অ্যালগরিদম চালুর পরিবেশ নিয়ন্ত্রণ করা, যাতে অনুপযুক্ত বাজারে ট্রেডিং এড়ানো যায়।

-

পজিশন ম্যানেজমেন্ট কৌশল অপ্টিমাইজ করা, যেমন রিস্ক-ভিত্তিক পজিশন সাইজিং, লস রিকভারি পজিশন ইত্যাদি, যাতে ঝুঁকি নিয়ন্ত্রণ করা যায় এবং উচ্চতর লাভের লক্ষ্যে পৌঁছানো যায়।

সারসংক্ষেপ

এই কৌশলটি অভ্যন্তরীণ বার সিগন্যাল এবং মুভিং এভারেজ ইন্ডিকেটরের গতিশীল ট্র্যাকিংয়ের মাধ্যমে একটি সম্পূর্ণ স্বয়ংক্রিয় কোয়ান্টিটেটিভ ট্রেডিং সমাধান বাস্তবায়ন করে। কৌশলের সংকেত তৈরি সহজ ও স্পষ্ট, বোঝা এবং অনুসরণ করা সহজ। স্পষ্ট ট্রেন্ডযুক্ত বাজারে এটি বেশ ভালো পারফর্ম করে। প্যারামিটার ও নিয়ম আরও অপ্টিমাইজ করে কৌশলের স্থিতিশীলতা ও লাভজনকতা আরও বাড়ানো যেতে পারে।

- 1