পরিমাণগত সূচকের উপর ভিত্তি করে বিটকয়েন ট্রেডিং কৌশল

সারসংক্ষেপ

এই কৌশলটি বিটকয়েনের ক্রয়-বিক্রয়ের সময় নির্ধারণের জন্য একাধিক কোয়ান্টিটেটিভ সূচক ব্যবহার করে এবং স্বয়ংক্রিয় ট্রেডিং বাস্তবায়ন করে। প্রধানত হাল সূচক (Hull), আপেক্ষিক শক্তি সূচক (RSI), বলিঞ্জার ব্যান্ড (BB) এবং ভলিউম অসিলেটর (VO) অন্তর্ভুক্ত।

কৌশলের নীতি

-

পরিবর্তিত হাল মুভিং এভারেজ ব্যবহার করে বাজারের প্রধান প্রবণতার দিক নির্ধারণ করা হয়, এবং বলিঞ্জার ব্যান্ডের সাহায্যে ব্রেকআউট ক্রয়/বিক্রয় পয়েন্ট নির্ধারণ করা হয়।

-

RSI সূচকটি অভিযোজিত ওঠানামার সীমার সাথে মিলিয়ে ওভারবট/ওভারসল্ড এলাকা নির্ধারণ করে এবং ট্রেডিং সিগন্যাল তৈরি করে। একই সাথে ডুপ্লিকেট সিগন্যাল যাচাইয়ের জন্য দুটি প্যারামিটার সেট করা হয়।

-

ভলিউম অসিলেটর ক্রয়-বিক্রয়ের শক্তি নির্ধারণ করে এবং মিথ্যা ব্রেকআউট এড়ায়।

-

স্টপ-লস/টেক-প্রফিট অনুপাত প্যারামিটারের ভিত্তিতে পূর্বনির্ধারিত স্টপ-লস এবং টেক-প্রফিট লেভেল সেট করে ঝুঁকি ব্যবস্থাপনা বাস্তবায়ন করে।

সুবিধা বিশ্লেষণ

-

হাল কার্ভ দ্রুত প্রবণতা পরিবর্তন ধরতে পারে, এবং বলিঞ্জার ব্যান্ডের সহায়ক মূল্যায়ন মিথ্যা সিগন্যাল কমাতে পারে।

-

RSI সূচকের প্যারামিটার অপ্টিমাইজেশন এবং ডুপ্লিকেট সিগন্যাল যাচাইয়ের কারণে নির্ভরযোগ্যতা বেশি।

-

ভলিউম অসিলেটর প্রবণতা ও সূচক সিগন্যালের সাথে মিলিয়ে ভুল ট্রেডিং এড়ায়।

-

পূর্বনির্ধারিত স্টপ-লস/টেক-প্রফিট পদ্ধতি স্বয়ংক্রিয়ভাবে একক ট্রেডের লাভ-ক্ষতি নিয়ন্ত্রণ করতে পারে এবং সামগ্রিক ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করে।

ঝুঁকি বিশ্লেষণ

-

প্যারামিটার সঠিকভাবে সেট না করলে ট্রেডিং ফ্রিকোয়েন্সি বেশি হতে পারে বা সিগন্যালের কার্যকারিতা কমে যেতে পারে।

-

অপ্রত্যাশিত ঘটনায় বাজারে তীব্র অস্থিরতা দেখা দিলে স্টপ-লস ভেঙে যেতে পারে, ফলে বড় ক্ষতি হতে পারে।

-

অন্য ক্রিপ্টোকারেন্সিতে ট্রেডিং করলে প্যারামিটার পুনরায় পরীক্ষা ও অপ্টিমাইজ করতে হবে।

-

ভলিউম ডেটা অনুপস্থিত থাকলে ভলিউম অসিলেটর অকার্যকর হয়ে যায়।

অপ্টিমাইজেশনের দিকনির্দেশনা

-

RSI প্যারামিটারের আরও বেশি কম্বিনেশন পরীক্ষা করে সর্বোত্তম প্যারামিটার খুঁজে বের করা।

-

MACD, KD ইত্যাদি অন্যান্য সূচকের সাথে RSI যুক্ত করে সিগন্যালের নির্ভুলতা বাড়ানোর চেষ্টা করা।

-

মডেল পূর্বাভাস মডিউল যোগ করে মেশিন লার্নিংয়ের মাধ্যমে বাজারের দিকনির্দেশ নির্ধারণ করা।

-

অন্য ট্রেডিং সম্পদের প্যারামিটার কার্যকারিতা পরীক্ষা করা।

-

স্টপ-লস/টেক-প্রফিট অ্যালগরিদম অপ্টিমাইজ করে সর্বোচ্চ মুনাফা অর্জন করা।

সারসংক্ষেপ

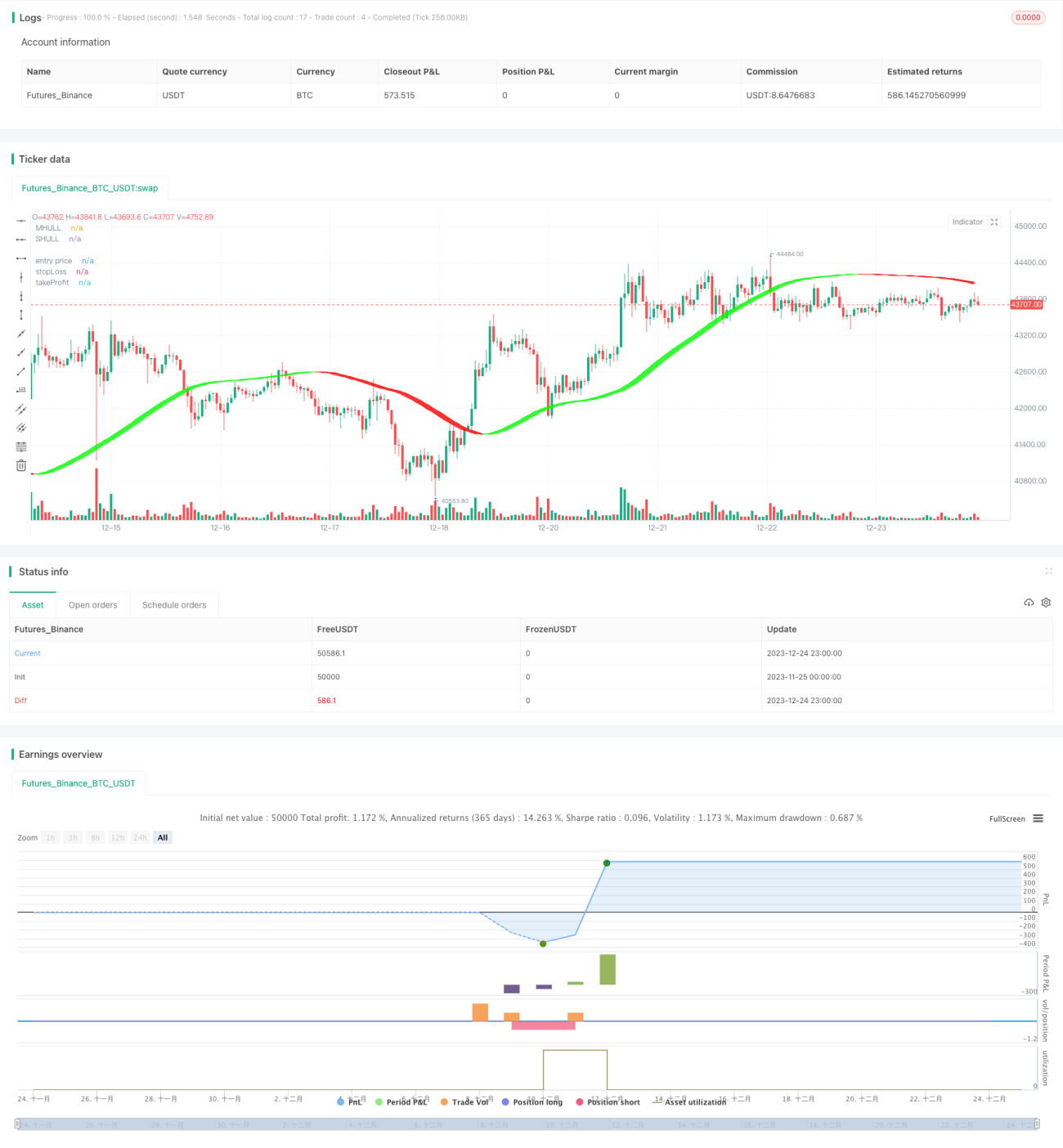

এই কৌশলটি ক্রয়-বিক্রয়ের সময় নির্ধারণের জন্য বিভিন্ন কোয়ান্টিটেটিভ টেকনিক্যাল সূচক সমন্বিতভাবে ব্যবহার করে। প্যারামিটার অপ্টিমাইজেশন, ঝুঁকি নিয়ন্ত্রণ ইত্যাদি পদ্ধতির মাধ্যমে বিটকয়েনের স্বয়ংক্রিয় ট্রেডিং বাস্তবায়িত হয়েছে। ফলাফল ভালো, তবে বাজারের পরিবর্তনের সাথে খাপ খাইয়ে নিতে ক্রমাগত পরীক্ষা ও অপ্টিমাইজেশন প্রয়োজন। এটি বিনিয়োগকারীদের জন্য রেফারেন্স এবং ট্রেডিং সিদ্ধান্তে সহায়তা প্রদান করতে পারে।

- 1