দ্বৈত ট্রেন্ড ফিল্টার চেইনকৃত চলমান গড় অনুপাত কৌশল

সংক্ষিপ্ত বিবরণ

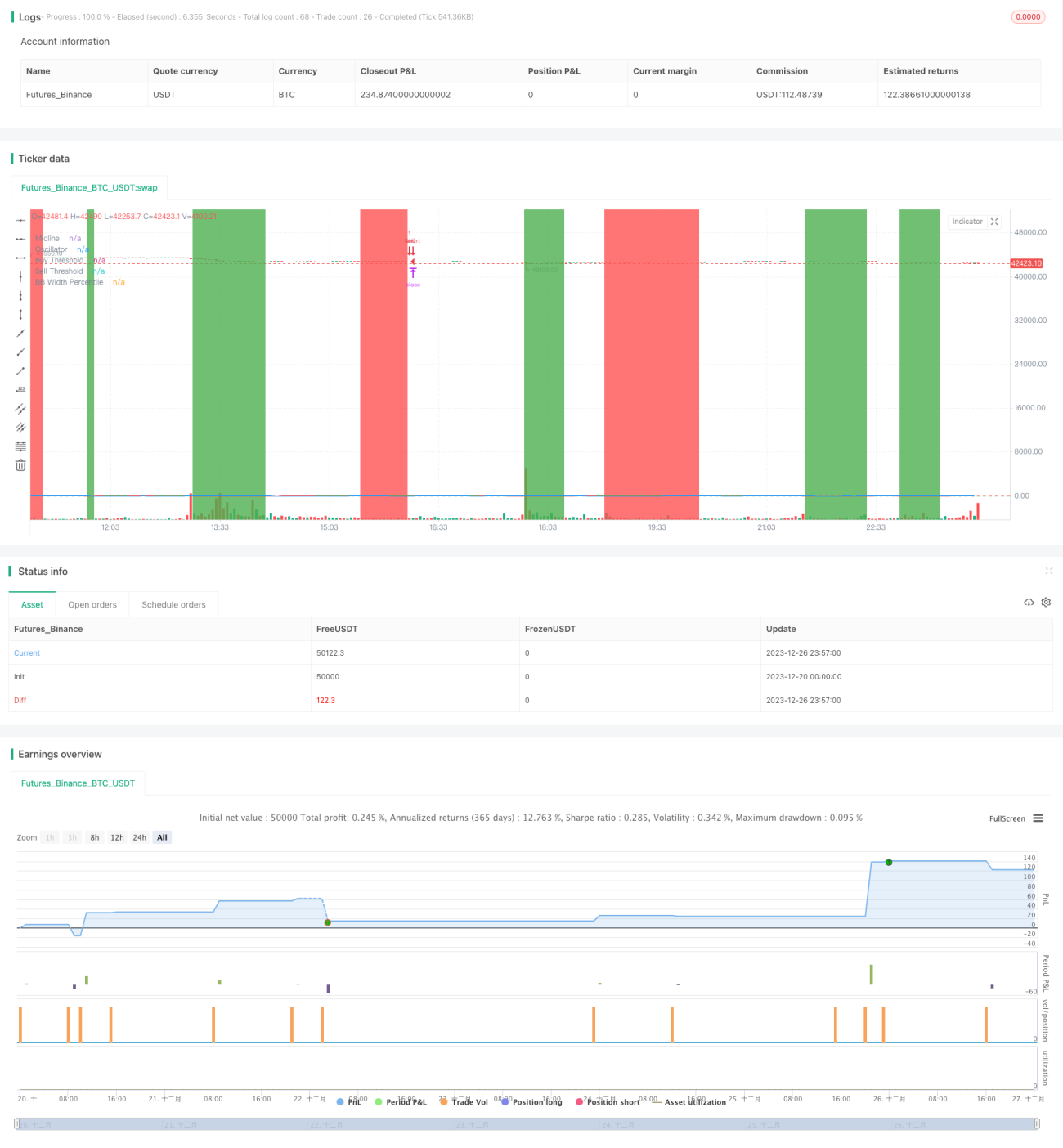

এই কৌশলটি দ্বৈত মুভিং এভারেজ রেশিও ইন্ডিকেটর, বোলিঞ্জার ব্যান্ড ফিল্টার এবং দ্বৈত ট্রেন্ড ফিল্টার ইন্ডিকেটরের উপর ভিত্তি করে তৈরি, যা চেইনড এক্সিট মেকানিজম সহ একটি ট্রেন্ড ফলোয়িং কৌশল। এই কৌশলটির উদ্দেশ্য হল মুভিং এভারেজ রেশিও ইন্ডিকেটর ব্যবহার করে মধ্যম ও দীর্ঘমেয়াদী ট্রেন্ড দিকনির্দেশনা চিহ্নিত করা, এবং যখন ট্রেন্ড দিক স্পষ্ট হয় তখন ভাল এন্ট্রি পয়েন্ট বেছে নেওয়া, এবং লাভ লক করতে এবং ক্ষতি কমাতে টেক প্রফিট ও স্টপ লস এক্সিট মেকানিজম সেট করা।

কৌশল নীতি

১. দ্রুত মুভিং এভারেজ (১০ দিনের) এবং ধীর মুভিং এভারেজ (৫০ দিনের) গণনা করুন এবং তাদের অনুপাত নির্ণয় করুন, যাকে প্রাইস মুভিং এভারেজ রেশিও বলা হয়। এই অনুপাত কার্যকরভাবে মূল্যের মধ্যম ও দীর্ঘমেয়াদী ট্রেন্ড পরিবর্তন শনাক্ত করতে পারে।

২. প্রাইস মুভিং এভারেজ রেশিওকে পার্সেন্টাইলে রূপান্তর করুন, অর্থাৎ নির্দিষ্ট সময়ের মধ্যে বর্তমান অনুপাতের আপেক্ষিক শক্তি। এই পার্সেন্টাইলকে অসিলেটর হিসেবে সংজ্ঞায়িত করা হয়।

৩. যখন অসিলেটর নির্ধারিত ক্রয় থ্রেশহোল্ড (১০) উপরে উঠে যায় তখন ক্রয় সিগন্যাল তৈরি হয়, এবং যখন বিক্রয় থ্রেশহোল্ড (৯০) নিচে ভেঙে যায় তখন বিক্রয় সিগন্যাল তৈরি হয়, ট্রেন্ড ফলো করে।

৪. বোলিঞ্জার ব্যান্ডের প্রস্থ ইন্ডিকেটরের সাথে মিলিয়ে ট্রেডিং সিগন্যাল ফিল্টার করা হয়, বোলিঞ্জার ব্যান্ড সংকুচিত হলে ট্রেড করা হয়।

৫. দ্বৈত ট্রেন্ড ফিল্টার ইন্ডিকেটর ব্যবহার করা হয়, শুধুমাত্র যখন মূল্য ঊর্ধ্বমুখী ট্রেন্ড চ্যানেলে থাকে তখন ক্রয় সিগন্যাল তৈরি হয়, এবং শুধুমাত্র যখন মূল্য নিম্নমুখী চ্যানেলে থাকে তখন বিক্রয় সিগন্যাল তৈরি হয়, যাতে বিপরীত ট্রেন্ডে ট্রেড করা এড়ানো যায়।

৬. চেইনড এক্সিট মেকানিজম সেট করা হয়, যার মধ্যে টেক প্রফিট, স্টপ লস এবং কম্বিনেশন এক্সিট অন্তর্ভুক্ত। একাধিক এক্সিট শর্ত প্রিসেট করা যায়, এবং সর্বোচ্চ লাভ দেয় এমন শর্তকে অগ্রাধিকার দিয়ে এক্সিট করা হয়।

কৌশলের সুবিধা

- দ্বৈত ট্রেন্ড ফিল্টার মেকানিজম নির্ভরযোগ্যভাবে প্রধান ট্রেন্ড দিক নির্ণয় করে, বিপরীত ট্রেন্ডে ট্রেড করা এড়ায়।

- মুভিং এভারেজ রেশিও ইন্ডিকেটর একক মুভিং এভারেজের চেয়ে বেশি কার্যকরভাবে ট্রেন্ড পরিবর্তন শনাক্ত করে।

- বোলিঞ্জার ব্যান্ডের প্রস্থ ইন্ডিকেটর কার্যকরভাবে বাজারের কম ওঠানামার সময় চিহ্নিত করে, যখন ট্রেডিং সিগন্যাল আরও নির্ভরযোগ্য হয়।

- চেইনড এক্সিট মেকানিজম লাভকে আরও স্থিতিশীল করে, মোট লাভ সর্বাধিক করে।

ঝুঁকি ও সমাধান

১. যখন বাজার দোদুল্যমান হয় এবং স্পষ্ট ট্রেন্ড থাকে না, তখন অনেক ভুল সিগন্যাল এবং রিভার্সাল হয়। সমাধান হল বোলিঞ্জার ব্যান্ডের প্রস্থ ফিল্টারের সাথে মিলিয়ে কাজ করা, সংকুচিত হলে ট্রেড করা।

২. যখন স্পষ্ট ট্রেন্ড রিভার্সাল হয়, মুভিং এভারেজ ল্যাগ তৈরি করে এবং প্রথম মুহূর্তে রিভার্সাল সিগন্যাল শনাক্ত করতে পারে না। সমাধান হল মুভিং এভারেজের সময়কাল পরামিতি যথাযথভাবে সংক্ষিপ্ত করা।

৩. যখন বাজারে গ্যাপ তৈরি হয়, স্টপ লস পয়েন্ট তাৎক্ষণিকভাবে আঘাতপ্রাপ্ত হতে পারে, যার ফলে বড় ক্ষতি হয়। সমাধান হল স্টপ লস পয়েন্টের পরামিতি কিছুটা শিথিল করা।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- প্যারামিটার অপ্টিমাইজেশন। মুভিং এভারেজ সময়কাল, অসিলেটর ক্রয়/বিক্রয় পয়েন্ট, বোলিঞ্জার ব্যান্ড প্যারামিটার, ট্রেন্ড ফিল্টার প্যারামিটারগুলির জন্য এক্সহস্টিভ টেস্টিং করা যেতে পারে, সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করতে।

- অন্যান্য ইন্ডিকেটর একীভূত করা। ট্রেন্ড রিভার্সাল শনাক্ত করার জন্য অন্যান্য ইন্ডিকেটর যেমন কেডি (KD) ইন্ডিকেটর, এমএসিডি (MACD) ইন্ডিকেটর ইত্যাদি যুক্ত করার কথা বিবেচনা করা যেতে পারে, যাতে কৌশলের নির্ভুলতা বৃদ্ধি পায়।

- মেশিন লার্নিং। ঐতিহাসিক ডেটা সংগ্রহ করে মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে মডেল প্রশিক্ষণ দেওয়া যেতে পারে, বিভিন্ন প্যারামিটার গতিশীলভাবে অপ্টিমাইজ করতে, প্যারামিটারের অভিযোজিত সমন্বয় অর্জন করতে।

সারসংক্ষেপ

এই কৌশলটি দ্বৈত মুভিং এভারেজ রেশিও ইন্ডিকেটর এবং বোলিঞ্জার ব্যান্ড ইন্ডিকেটর সমন্বিতভাবে ব্যবহার করে মধ্যম ও দীর্ঘমেয়াদী ট্রেন্ড দিক নির্ণয় করে, ট্রেন্ড নিশ্চিত হওয়ার পর সর্বোত্তম এন্ট্রি পয়েন্টে প্রবেশ করে, এবং চেইনড এক্সিট মেকানিজম সেট করে লাভ লক করে, যা উচ্চ নির্ভরযোগ্য এবং কার্যকর। এই কৌশলটি প্যারামিটার অপ্টিমাইজেশন, অন্যান্য সহায়ক নির্ধারণকারী ইন্ডিকেটর যোগ করা এবং মেশিন লার্নিংয়ের মাধ্যমে আরও উন্নত এবং লাভের হার বৃদ্ধি করা যেতে পারে।

- 1