মোমেন্টাম নির্দেশক ক্রসওভার রিভার্সাল ট্রেন্ড ফলোয়িং কৌশল

সারসংক্ষেপ

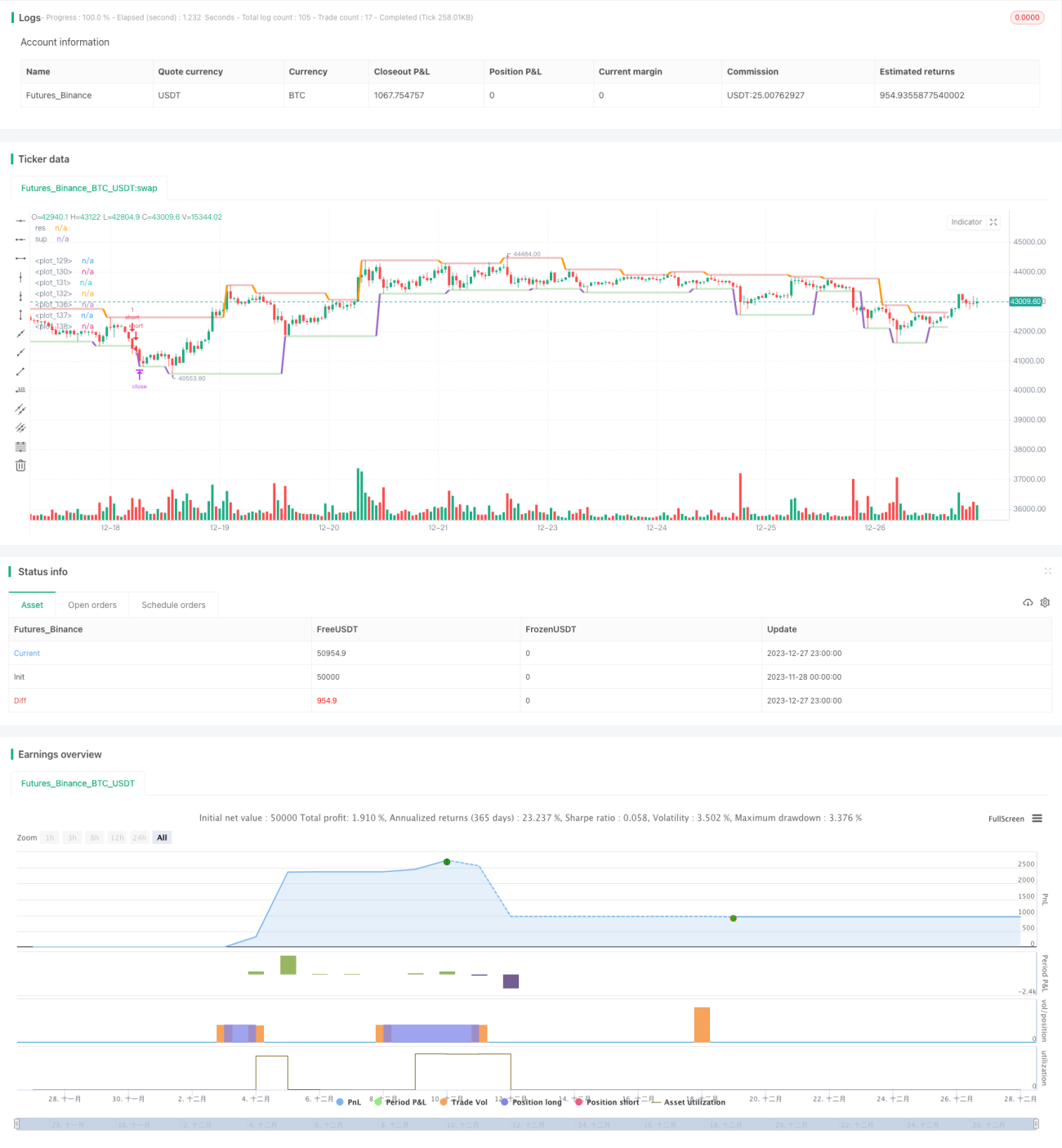

এই কৌশলটি MACD, RSI, ADX সহ একাধিক মুভমেন্ট টেকনিক্যাল ইন্ডিকেটর ব্যবহার করে মূল্য বিপরীত সংকেত সনাক্ত করে এবং বিপরীত কৌশল প্রয়োগ করে, শক্তিশালী ট্রেন্ড উল্টে গেলে বিপরীত দিকে প্রবেশ করে। কৌশলটি একইসাথে স্টপ-লস এবং টেক-প্রফিট নির্ধারণ করে, যাতে লাভ ধরে রাখা ও ঝুঁকি নিয়ন্ত্রণ করা যায়।

কৌশলের মূলনীতি

এই কৌশলটি প্রথমে MACD নির্দেশকের দ্রুত ও ধীর গতির মুভিং এভারেজের ক্রসওভার (গোল্ডেন ক্রস/ডেথ ক্রস) তুলনা করে মূল্য ট্রেন্ড নির্ধারণ করে; তারপর RSI নির্দেশক ব্যবহার করে মিথ্যা ব্রেকআউট ফিল্টার করে, যাতে প্রকৃত মূল্য বিপরীত ঘটার পরই ট্রেডিং সংকেত তৈরি হয়; শেষে ADX নির্দেশক দিয়ে আবার নিশ্চিত করা হয় যে মূল্য ট্রেন্ড অবস্থায় প্রবেশ করেছে কিনা। যখন এই একাধিক শর্ত একসাথে পূরণ হয়, তখনই ক্রয় বা বিক্রয় সংকেত উৎপন্ন হয়।

বিশেষভাবে, যখন MACD দ্রুত রেখা ধীর রেখা উপরে উঠে যায়, RSI 50-এর উপরে এবং ঊর্ধ্বমুখী হয়, এবং ADX 20-এর উপরে থাকে তখন এটি ক্রয় সংকেত; যখন MACD দ্রুত রেখা ধীর রেখা নিচে নামে, RSI 50-এর নিচে এবং নিম্নমুখী হয়, এবং ADX 20-এর উপরে থাকে তখন এটি বিক্রয় সংকেত।

সুবিধা বিশ্লেষণ

এই কৌশলের সবচেয়ে বড় সুবিধা হল একাধিক সূচকের সংমিশ্রণ ব্যবহার করে কার্যকরভাবে সাইডওয়ে মার্কেট এবং ভুল সংকেত ফিল্টার করা, প্রকৃত ট্রেন্ড বিপরীত পয়েন্ট ধরা, ফলে উচ্চ জয়রেট পাওয়া যায়। এছাড়া স্টপ-লস ও টেক-প্রফিট নির্ধারণ করে লাভ ধরে রাখা ও ঝুঁকি নিয়ন্ত্রণ করা যায়, যা অপ্রত্যাশিত ঘটনার প্রভাব প্রতিরোধে সহায়ক।

ঝুঁকি বিশ্লেষণ

এই কৌশলের সবচেয়ে বড় ঝুঁকি হল ট্রেন্ড বিপরীতের ভুল সনাক্তকরণ, যেমন মূল্যের গভীর রিট্রেসমেন্টের কারণে ভুল সিদ্ধান্ত নেওয়া। এছাড়াও, বিপরীতের পর নতুন ট্রেন্ড পর্যাপ্ত লাভের জন্য যথেষ্ট স্থায়ী নাও হতে পারে।

সমাধান হল প্যারামিটারগুলি আরও অপ্টিমাইজ করা, স্টপ-লসের মাত্রা সামঞ্জস্য করা, বা আরও সহায়ক ইন্ডিকেটর যোগ করে সংকেত ফিল্টার করা।

অপ্টিমাইজেশন দিকনির্দেশনা

এই কৌশলটি নিম্নলিখিত দিকগুলিতে আরও অপ্টিমাইজ করা যেতে পারে:

- MACD ও RSI প্যারামিটার সংমিশ্রণ অপ্টিমাইজ করে মূল্য বিপরীত সনাক্তকরণের নির্ভুলতা বাড়ানো

- আরও ইন্ডিকেটর ফিল্টার যোগ করা, যেমন KD, BOLL ইত্যাদি, যাতে ইন্ডিকেটর ঘেরাও প্রভাব তৈরি হয়

- গতিশীলভাবে স্টপ-লস মাত্রা সামঞ্জস্য করা, বিভিন্ন বাজার পরিস্থিতিতে পরিবর্তন করা

- বিপরীতের পর প্রকৃত আন্দোলন অনুসারে রিয়েল-টাইমে টেক-প্রফিট অবস্থান পরিবর্তন করা

উপসংহার

এই কৌশলটি একাধিক মুভমেন্ট ইন্ডিকেটর ব্যবহার করে সম্ভাব্য মূল্য বিপরীত সুযোগ শনাক্ত করে। প্যারামিটার অপ্টিমাইজেশন, আরও সহায়ক ইন্ডিকেটর যোগ করা এবং গতিশীল স্টপ-লস ও টেক-প্রফিট কৌশল ব্যবহারের মাধ্যমে কৌশলের স্থিতিশীলতা ও নির্ভরযোগ্যতা আরও বাড়ানো যেতে পারে, এবং বাজার প্রদত্ত বিভিন্ন ট্রেডিং সুযোগ ক্যাপচার করা যেতে পারে।

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1