স্ব-অভিযোজিত বুয়েঙ্কে নির্দেশক দীর্ঘ-সংক্ষিপ্ত কৌশল

সারসংক্ষেপ (Overview)

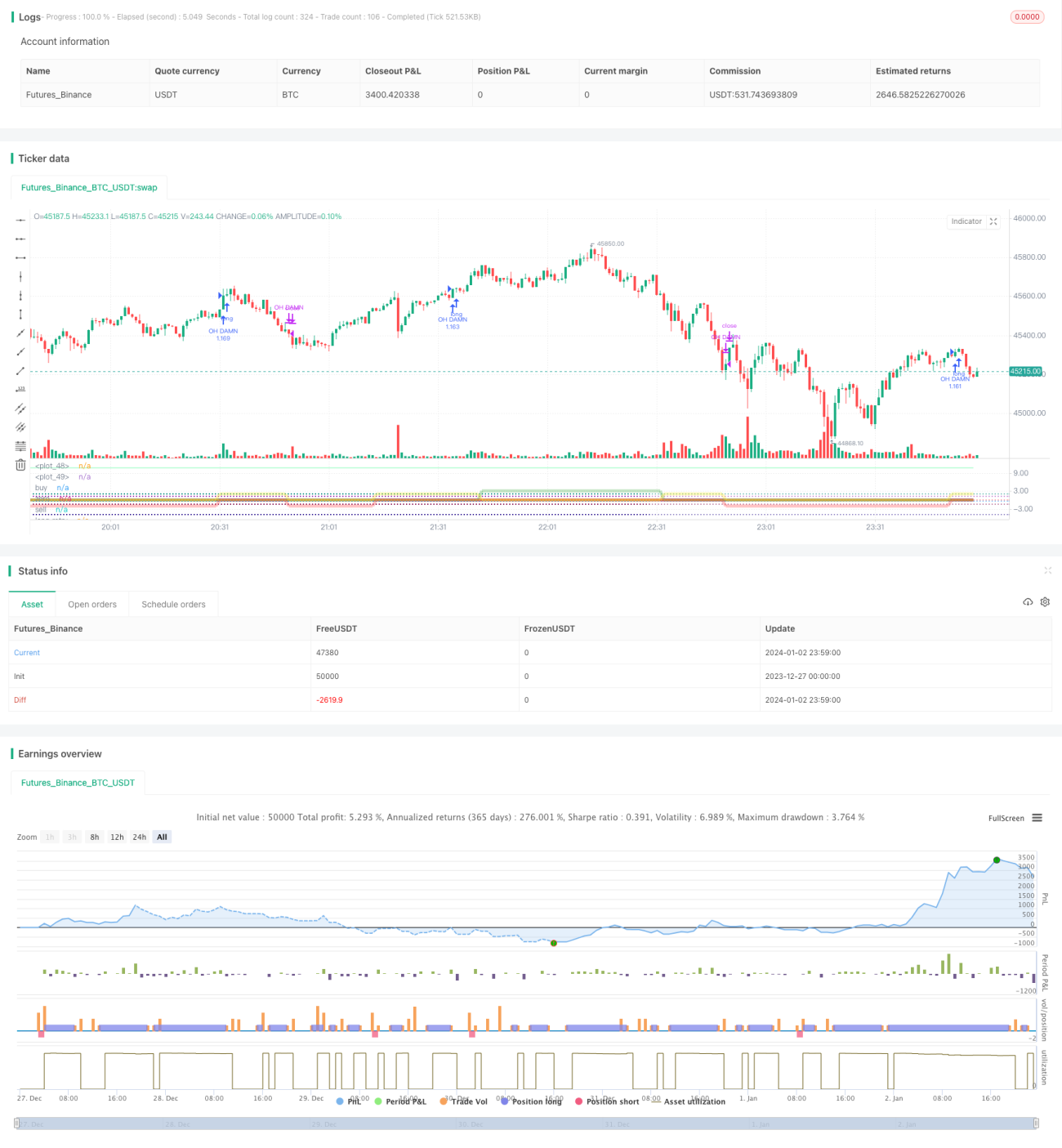

কৌশলটি ব্রুনকো সূচকের উপর ভিত্তি করে স্বয়ংক্রিয়ভাবে বাজারের প্রবণতা শনাক্ত করে এবং লং/শর্ট পজিশন তৈরি করে। এটি ব্রুনকো সূচক, মুভিং এভারেজ এবং অনুভূমিক সাপোর্ট লাইনের মতো প্রযুক্তিগত সূচকগুলিকে একীভূত করে, স্বয়ংক্রিয়ভাবে ব্রেকআউট সংকেত শনাক্ত করে এবং পজিশন খোলে।

কৌশলের মূলনীতি (Strategy Principle)

এই কৌশলের মূল সূচক হল ব্রুনকো সূচক, যা বিভিন্ন ট্রেডিং দিনের ক্লোজিং মূল্যের লগারিদমিক পার্থক্য গণনা করে বাজারের প্রবণতা এবং গুরুত্বপূর্ণ সাপোর্ট/রেজিস্ট্যান্স লেভেল নির্ধারণ করে। যখন সূচকটি একটি নির্দিষ্ট অনুভূমিক রেখা অতিক্রম করে (উপর থেকে নিচে বা নিচ থেকে উপরে), তখন লং বা শর্ট পজিশন নেওয়া হয়।

উপরন্তু, কৌশলটি ২১-দিন এবং ৫৫-দিনের মুভিং এভারেজ সহ একাধিক মুভিং এভারেজ দ্বারা গঠিত "ইএমএ (EMA) সুরক্ষা বেল্ট" একীভূত করে। এই মুভিং এভারেজগুলির ক্রম সম্পর্কের মাধ্যমে বর্তমানে বাজারটি ষাঁড়ের বাজার (বুলিশ), ভালুকের বাজার (বেয়ারিশ) নাকি সাইডওয়েজ (পার্শ্ববর্তী) তা নির্ধারণ করা হয় এবং সেই অনুযায়ী শর্ট বা লং অপারেশন সীমাবদ্ধ করা হয়।

ব্রুনকো সূচকের মাধ্যমে ট্রেডিং সিগন্যাল শনাক্ত এবং মুভিং এভারেজের মাধ্যমে বাজারের পর্যায় নির্ণয় — এই দুটির সমন্বয় ব্যবহার করে অনুপযুক্ত পজিশন খোলা এড়ানো যায়।

সুবিধা বিশ্লেষণ (Advantage Analysis)

এই কৌশলের সবচেয়ে বড় সুবিধা হল এটি স্বয়ংক্রিয়ভাবে বাজারের ষাঁড়/ভালুক (বুলিশ/বেয়ারিশ) প্রবণতা শনাক্ত করতে পারে। ব্রুনকো সূচক দুটি সময়সীমার মূল্যের পার্থক্যের প্রতি অত্যন্ত সংবেদনশীল, তাই এটি দ্রুত মূল সাপোর্ট ও রেজিস্ট্যান্স সনাক্ত করতে পারে; অন্যদিকে মুভিং এভারেজের ক্রম কার্যকরভাবে বর্তমান বাজারের অবস্থা (বুলিশ না বেয়ারিশ) নির্ধারণ করতে পারে।

দ্রুত সূচক ও প্রবণতা সূচকের এই সমন্বয় কৌশলটিকে দ্রুত কেনা/বেচার পয়েন্ট চিহ্নিত করতে এবং একইসাথে অনুপযুক্ত কেনাবেচা প্রতিরোধ করতে সাহায্য করে। এটি এই কৌশলের সবচেয়ে বড় সুবিধা।

ঝুঁকি বিশ্লেষণ (Risk Analysis)

এই কৌশলের ঝুঁকি প্রধানত দুটি দিক থেকে আসে: প্রথমত, ব্রুনকো সূচক নিজেই মূল্য পরিবর্তনের প্রতি অত্যন্ত সংবেদনশীল, যার ফলে অনেক অপ্রয়োজনীয় ট্রেডিং সিগন্যাল তৈরি হতে পারে; দ্বিতীয়ত, সাইডওয়েজ (পার্শ্ববর্তী) বাজারে মুভিং এভারেজের ক্রম বিশৃঙ্খল হয়ে পড়তে পারে, যার ফলে পজিশন খোলার ক্ষেত্রে জটিলতা তৈরি হয়।

প্রথম ঝুঁকি মোকাবেলায় ব্রুনকো সূচকের প্যারামিটারগুলি যথাযথভাবে সামঞ্জস্য করে সূচকের গণনা চক্র বাড়ানো যেতে পারে, যাতে অপ্রয়োজনীয় ট্রেড কমে; দ্বিতীয় ঝুঁকি মোকাবেলায় আরও বেশি মুভিং এভারেজ যুক্ত করা যেতে পারে, যাতে প্রবণতা নির্ণয় আরও নির্ভুল হয়।

অপ্টিমাইজেশন দিকনির্দেশ (Optimization Directions)

এই কৌশলের প্রধান অপ্টিমাইজেশন দিক হল প্যারামিটার সমন্বয় এবং ফিল্টার শর্ত বৃদ্ধি।

ব্রুনকো সূচকের জন্য বিভিন্ন সময়কালের প্যারামিটার পরীক্ষা করে সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করা যেতে পারে; মুভিং এভারেজের জন্য আরও বেশি এভারেজ যুক্ত করে আরও সম্পূর্ণ প্রবণতা নির্ণয় ব্যবস্থা গঠন করা যেতে পারে। এছাড়া ভোলাটিলিটি সূচক, ট্রেডিং ভলিউম সূচক ইত্যাদি ফিল্টার শর্ত যুক্ত করে মিথ্যা সিগন্যাল কমানো যেতে পারে।

প্যারামিটার ও শর্তের সামগ্রিক সমন্বয়ের মাধ্যমে কৌশলের স্থিতিশীলতা ও লাভজনকতা আরও উন্নত করা যেতে পারে।

সারসংক্ষেপ (Summary)

এই অ্যাডাপটিভ ব্রুনকো লং/শর্ট কৌশলটি সফলভাবে দ্রুত সূচক ও প্রবণতা সূচককে একীভূত করেছে, এবং এটি স্বয়ংক্রিয়ভাবে বাজারের মূল পয়েন্টগুলি শনাক্ত করে সঠিক পজিশন তৈরি করতে পারে। এর সুবিধা হল দ্রুত পয়েন্ট শনাক্তকরণ ও অনুপযুক্ত পজিশন খোলা প্রতিরোধ করার ক্ষমতা। পরবর্তী ধাপে প্যারামিটার ও শর্ত অপ্টিমাইজেশনের মাধ্যমে কৌশলের স্থিতিশীলতা ও লাভের মাত্রা আরও উন্নত করা যেতে পারে।

- 1