RSI এবং AI-ভিত্তিক কাস্টম শর্ত ব্যবহার করে ট্রেডিংয়ের জন্য একটি উন্নত কৌশল

সারসংক্ষেপ

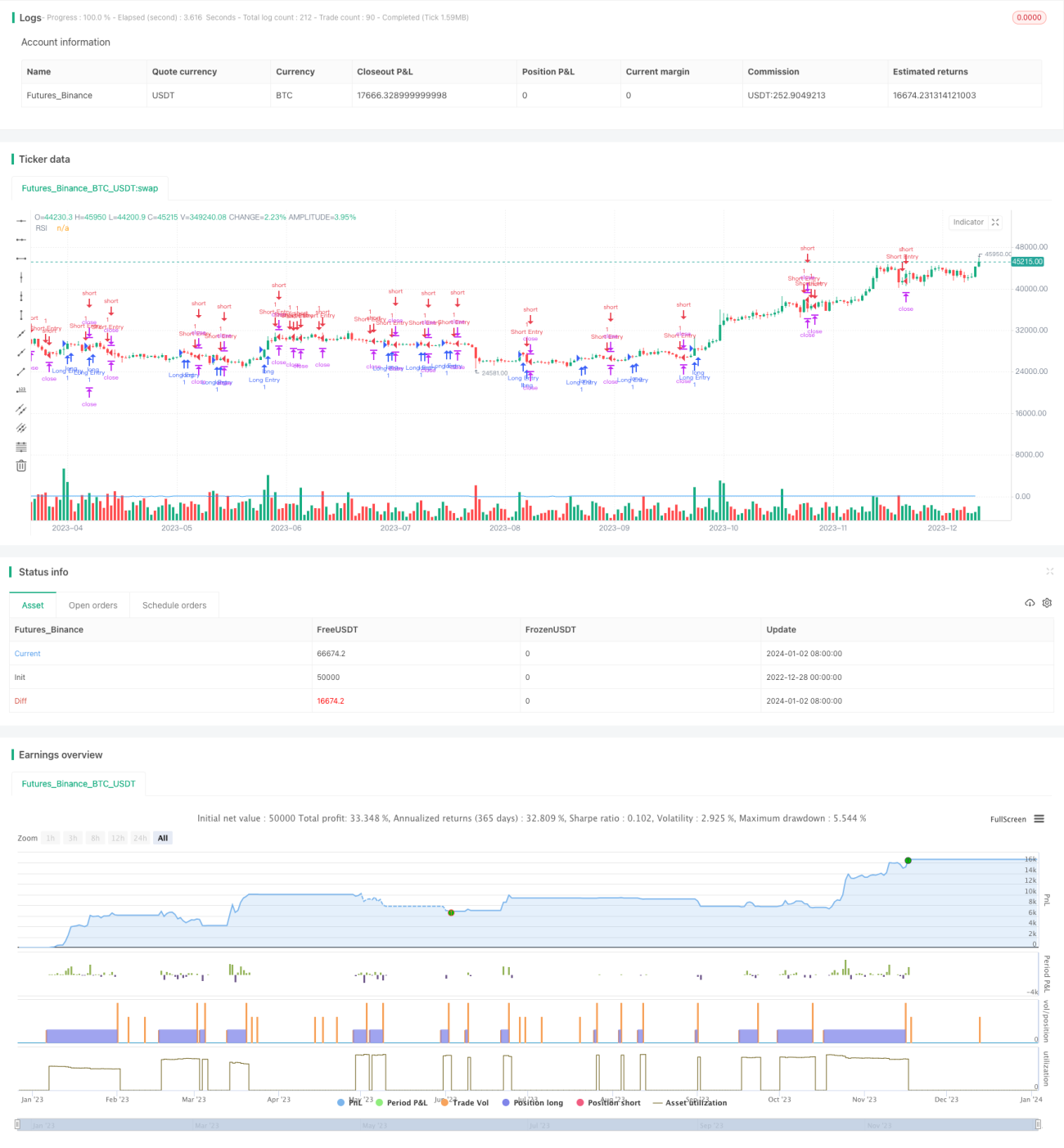

এই কৌশলের মূল ধারণা হল RSI সূচক এবং কাস্টম AI শর্ত ব্যবহার করে ট্রেডিং সুযোগ খুঁজে বের করা। এটি একাধিক শর্ত পূরণ হলে লং বা শর্ট পজিশন খোলে এবং নির্দিষ্ট লাভ ও লোকসানের স্তর ব্যবহার করে।

কৌশলের নীতি

এই কৌশলটি নিম্নলিখিত ধাপগুলির মাধ্যমে বাস্তবায়িত হয়:

- 14 পিরিয়ডের RSI মান গণনা করা

- দুটি কাস্টম AI শর্ত (লং এবং শর্ট) সংজ্ঞায়িত করা

- AI শর্তগুলিকে RSI-এর ওভারবট ও ওভারসোল্ড এলাকার সাথে একত্রিত করে এন্ট্রি সিগন্যাল তৈরি করা

- ঝুঁকির শতাংশ এবং স্টপ লস পয়েন্টের ভিত্তিতে পজিশনের আকার গণনা করা

- টেক প্রফিট এবং স্টপ লস মূল্য গণনা করা

- এন্ট্রি সিগন্যাল পূরণ হলে পজিশন খোলা

- টেক প্রফিট বা স্টপ লস শর্ত পূরণ হলে পজিশন বন্ধ করা

একই সাথে, এই কৌশলটি ট্রেডিং সিগন্যাল তৈরি হলে এলার্ম দেয় এবং চার্টে RSI কার্ভ আঁকে।

কৌশলের সুবিধা বিশ্লেষণ

এই কৌশলটির নিম্নলিখিত সুবিধাগুলি রয়েছে:

- RSI এবং AI শর্তের সংমিশ্রণ ট্রেডিং সুযোগ আরও নির্ভুলভাবে চিহ্নিত করতে সাহায্য করে

- একাধিক শর্তের সংমিশ্রণ ব্যবহার করে মিথ্যা সিগন্যাল কার্যকরভাবে ফিল্টার করা যায়

- ঝুঁকি ব্যবস্থাপনার নীতি অনুযায়ী পজিশনের আকার গণনা করে প্রতিটি ট্রেডের ঝুঁকি নিয়ন্ত্রণ করা যায়

- নির্দিষ্ট টেক প্রফিট ও স্টপ লস পদ্ধতি ব্যবহার করে প্রতিটি ট্রেডের ঝুঁকি ও রিটার্ন পরিষ্কার থাকে

- প্যারামিটার অ্যাডজাস্ট করে কৌশলটি স্বাধীনভাবে কাস্টমাইজ করা যায়

কৌশলের ঝুঁকি বিশ্লেষণ

এই কৌশলটিতে কিছু ঝুঁকি থাকতে পারে:

- RSI প্যারামিটার ঠিকমতো সেট না করলে ট্রেডিং সিগন্যাল ভুল হতে পারে

- কাস্টম AI শর্ত ঠিকমতো ডিজাইন না করলেও ভুল সিগন্যাল তৈরি হতে পারে

- স্টপ লস পয়েন্ট খুব ছোট করলে ঘন ঘন স্টপ লস ট্রিগার হতে পারে

- বাজারে তীব্র ওঠানামার সময় নির্দিষ্ট টেক প্রফিট ও স্টপ লস পদ্ধতির কারণে বেশি লাভ নষ্ট হতে পারে বা ক্ষতি বাড়তে পারে

RSI প্যারামিটার অ্যাডজাস্ট করা, AI শর্ত অপ্টিমাইজ করা, স্টপ লস দূরত্ব একটু শিথিল করে দেওয়ার মাধ্যমে এই ঝুঁকিগুলি কমানো যায়।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

এই কৌশলটি নিম্নলিখিত দিকগুলির মাধ্যমে অপ্টিমাইজ করা যেতে পারে:

- আরও কাস্টম AI শর্ত যোগ করা, ট্রেন্ড বিচারের জন্য আরও ফ্যাক্টর কম্বাইন করা

- RSI প্যারামিটার অপ্টিমাইজ করে সেরা প্যারামিটার কম্বিনেশন খুঁজে বের করা

- বিভিন্ন টেক প্রফিট ও স্টপ লস মেকানিজম পরীক্ষা করা, যেমন ট্রেইলিং স্টপ, মুভিং টেক প্রফিট

- অতিরিক্ত ফিল্টারিং শর্ত যোগ করা, যেমন ভলিউম হঠাৎ বেড়ে যাওয়া, যাতে উচ্চ মানের ট্রেডিং সুযোগ পাওয়া যায়

- মেশিন লার্নিং অ্যালগরিদমের সাথে যুক্ত করে স্বয়ংক্রিয়ভাবে সেরা প্যারামিটার জেনারেট করা

সারসংক্ষেপ

সামগ্রিকভাবে, এটি একটি কাস্টমাইজযোগ্য এবং অপ্টিমাইজেশনের বড় সুযোগ সম্বলিত উন্নত কৌশল, যা RSI সূচক এবং AI কাস্টম শর্তের উপর ভিত্তি করে ট্রেড করে। এটি একাধিক সিগন্যাল সোর্সের কম্বিনেশনের মাধ্যমে ট্রেন্ডের দিক নির্ধারণ করে, ঝুঁকি ব্যবস্থাপনা এবং টেক প্রফিট-স্টপ লস মেকানিজম ব্যবহার করে ট্রেড করে। এই কৌশলটি ব্যবহারকারীদের জন্য ভাল ট্রেডিং ফলাফল দিতে পারে এবং এর সম্প্রসারণ ও অপ্টিমাইজেশনের ব্যাপক সুযোগ রয়েছে।

- 1