সুপারট্রেন্ড অ্যাডভান্সড স্ট্র্যাটেজি

সারসংক্ষেপ

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলটি ক্লাসিক্যাল সুপার ট্রেন্ড ইন্ডিকেটরের উপর ভিত্তি করে অপ্টিমাইজ ও উন্নত একটি কৌশল। এটি মূল্য ক্রিয়া, অস্থিরতা এবং একাধিক টেকনিক্যাল ইন্ডিকেটরকে একত্রিত করে যাতে সিগন্যালের গুণমান বৃদ্ধি পায়, শব্দ কমে যায় এবং বাজারের প্রবণতার পরিবর্তন আরও নির্ভুলভাবে ধরা যায়।

কৌশলের নীতি

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলের মূল হল সুপার ট্রেন্ড লাইন। এটি প্রকৃত পরিসর (True Range) এবং মূল্যের গতিবেগের ভিত্তিতে গণনা করা হয়, যা সম্ভাব্য মূল্য প্রবণতা এবং টার্নিং পয়েন্ট নির্ণয় করতে ব্যবহৃত হয়। যখন দাম সুপার ট্রেন্ড লাইনের উপরে থাকে, তখন তা ঊর্ধ্বমুখী প্রবণতা নির্দেশ করে; অন্যথায় নিম্নমুখী প্রবণতা নির্দেশ করে।

প্রথাগত সুপার ট্রেন্ড ইন্ডিকেটর শুধুমাত্র ক্লোজিং প্রাইস এবং প্রকৃত পরিসর বিবেচনা করে, কিন্তু অ্যাডভান্সড কৌশলটি সিগন্যালের নির্ভরযোগ্যতা যাচাইয়ের জন্য ভলিউম, মোমেন্টাম অসিলেটর এবং মৌলিক ডেটার মতো একাধিক মাত্রাকেও অন্তর্ভুক্ত করে। এই বহু-পরিবর্তনশীল পদ্ধতি নিশ্চিত করে যে উৎপাদিত ট্রেডিং সিগন্যালগুলি আরও নির্ভুল এবং নির্ভরযোগ্য, এবং সহজেই বাজারের শব্দ দ্বারা প্রভাবিত হয় না।

সুবিধা বিশ্লেষণ

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলের প্রধান সুবিধাগুলি হলো:

-

বাজারের গতিপথ আরও নির্ভুলভাবে নির্ণয় করা এবং ভুয়া ব্রেকআউট ফিল্টার করা। এই কৌশলটি একাধিক ফ্যাক্টর এবং ইন্ডিকেটর একমত হওয়ার পরেই ট্রেডিং সিগন্যাল তৈরি করে, যা সঠিকতার হার ব্যাপকভাবে বৃদ্ধি করে।

-

বাজারের শব্দের হস্তক্ষেপ কমানো। ফিল্টার সংমিশ্রণ ব্যবহার করে বিপুল সংখ্যক অপ্রয়োজনীয় বাজার ডেটা বাদ দেওয়া যায়, ফলে বিচার আরও স্পষ্ট হয়।

-

রিস্ক ম্যানেজমেন্ট অপ্টিমাইজ করা। স্পষ্ট ট্রেডিং সিগন্যাল ব্যবসায়ীদের স্টপ লস এবং টেক প্রফিট পয়েন্ট আরও ভালোভাবে পরিকল্পনা করতে সাহায্য করে, যা উন্নত ঝুঁকি নিয়ন্ত্রণ সক্ষমতা প্রদান করে।

-

অভিযোজন ক্ষমতা শক্তিশালী। কৌশলটি শুধু প্রবণতা শনাক্ত করে না, বরং অন্যান্য টেকনিক্যাল টুলের সাথে সংমিশ্রণ করে একটি ব্যাপক ও দক্ষ ট্রেডিং সিস্টেম তৈরি করা যায়।

ঝুঁকি বিশ্লেষণ

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলের নিম্নলিখিত প্রধান ঝুঁকিও রয়েছে:

-

প্যারামিটার সেটিংয়ের ঝুঁকি। ভুল ইন্ডিকেটর প্যারামিটার সমন্বয়ের কারণে কৌশলটি ব্যর্থ হতে পারে বা অত্যধিক ভুল সিগন্যাল তৈরি করতে পারে।

-

প্রবণতা নির্ণয়ে ভুলের ঝুঁকি। কোনো কৌশলই সম্পূর্ণরূপে ভুল নির্ণয়ের ঝুঁকি এড়াতে পারে না, প্রবণতা অপ্রত্যাশিতভাবে পরিবর্তিত হলে ক্ষতি হতে পারে।

-

অত্যধিক অপ্টিমাইজেশনের ঝুঁকি। প্যারামিটারগুলিকে অত্যন্ত নির্ভুল পর্যায়ে সমন্বয় করলে তা ঐতিহাসিক ডেটার উপর অত্যধিক নির্ভরশীল হয়ে পড়ে এবং বাজারের পরিবর্তনের সাথে খাপ খাইয়ে নিতে পারে না।

-

ট্রেডিং খরচের ঝুঁকি। ট্রেডের সংখ্যা বৃদ্ধি পেলে কমিশন ও স্লিপেজের মতো ট্রেডিং খরচও উল্লেখযোগ্যভাবে বৃদ্ধি পায়।

প্রতিকারের পদ্ধতি:

-

প্যারামিটার সেটিং অপ্টিমাইজ করা এবং নিয়মিত ব্যাকটেস্ট করে প্যারামিটারের স্থিতিস্থাপকতা যাচাই করা।

-

স্টপ লস ও টেক প্রফিট নির্ধারণ করে একক ট্রেডের ক্ষতি নিয়ন্ত্রণ করা।

-

অত্যধিক অপ্টিমাইজেশন এড়িয়ে প্যারামিটারের সাধারণীকরণ ক্ষমতা বজায় রাখা।

-

সিগন্যালের ঝুঁকি-প্রত্যাবর্তন অনুপাত গণনা করে ট্রেডিং খরচ নিয়ন্ত্রণ করা।

অপ্টিমাইজেশনের দিকনির্দেশ

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলটি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

-

বিভিন্ন বাজার অনুযায়ী প্যারামিটার সমন্বয় করে সেগুলোকে সেই বাজারের বৈশিষ্ট্যের সাথে আরও সঙ্গতিপূর্ণ করা। যেমন অস্থির বাজারে গণনার সময়কাল সংক্ষিপ্ত করা যেতে পারে।

-

অভিযোজিত ফিল্টারিং মেকানিজম যুক্ত করা। বাজার যখন নির্দিষ্ট অবস্থায় প্রবেশ করে, তখন স্বয়ংক্রিয়ভাবে ইন্ডিকেটর প্যারামিটার সমন্বয় করা বা কিছু ফিল্টার নিষ্ক্রিয় করা।

-

মেশিন লার্নিং পদ্ধতি অন্বেষণ করা, যেমন নিউরাল নেটওয়ার্ক ব্যবহার করে মডেল প্রশিক্ষণের মাধ্যমে গতিশীলভাবে প্যারামিটার অপ্টিমাইজ করা।

-

সেন্টিমেন্ট ইন্ডিকেটর এবং নিউজ ইন্টেলিজেন্স যুক্ত করে আনস্ট্রাকচার্ড ডেটা ব্যবহার করে কার্যকারিতা বৃদ্ধি করা।

-

টার্গেট পজিশন সাইজিং ফাংশন যোগ করা। যখন জয়ের হার খুব বেশি হয়, তখন পজিশন বাড়িয়ে আরও বেশি মুনাফা অর্জন করা যায়।

উপসংহার

সুপার ট্রেন্ড অ্যাডভান্সড কৌশলটি একাধিক ফিল্টার এবং কনফার্মেশন ইন্ডিকেটর প্রবর্তনের মাধ্যমে ক্লাসিক্যাল সুপার ট্রেন্ড ইন্ডিকেটরকে অপ্টিমাইজ ও উন্নত করেছে, যা বাজারের গতিপথ আরও নির্ভুলভাবে নির্ণয় করতে এবং সিগন্যালের গুণমান বৃদ্ধি করতে সক্ষম। একক ইন্ডিকেটরের তুলনায়, এই কৌশলটি আরও স্থিতিশীল, ব্যাপক এবং দক্ষ ট্রেডিং সমাধান প্রদান করে। তবে একইসাথে প্যারামিটার ভুল সমন্বয় এবং নির্ণয় ত্রুটির ঝুঁকি সম্পর্কে সতর্ক থাকতে হবে এবং যথাযথ ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা গ্রহণ করতে হবে। ক্রমাগত অপ্টিমাইজেশন এবং অন্যান্য টুলের সাথে ব্যবহারের মাধ্যমে সুপার ট্রেন্ড অ্যাডভান্সড কৌশলের প্রয়োগের ব্যাপক সম্ভাবনা রয়েছে।

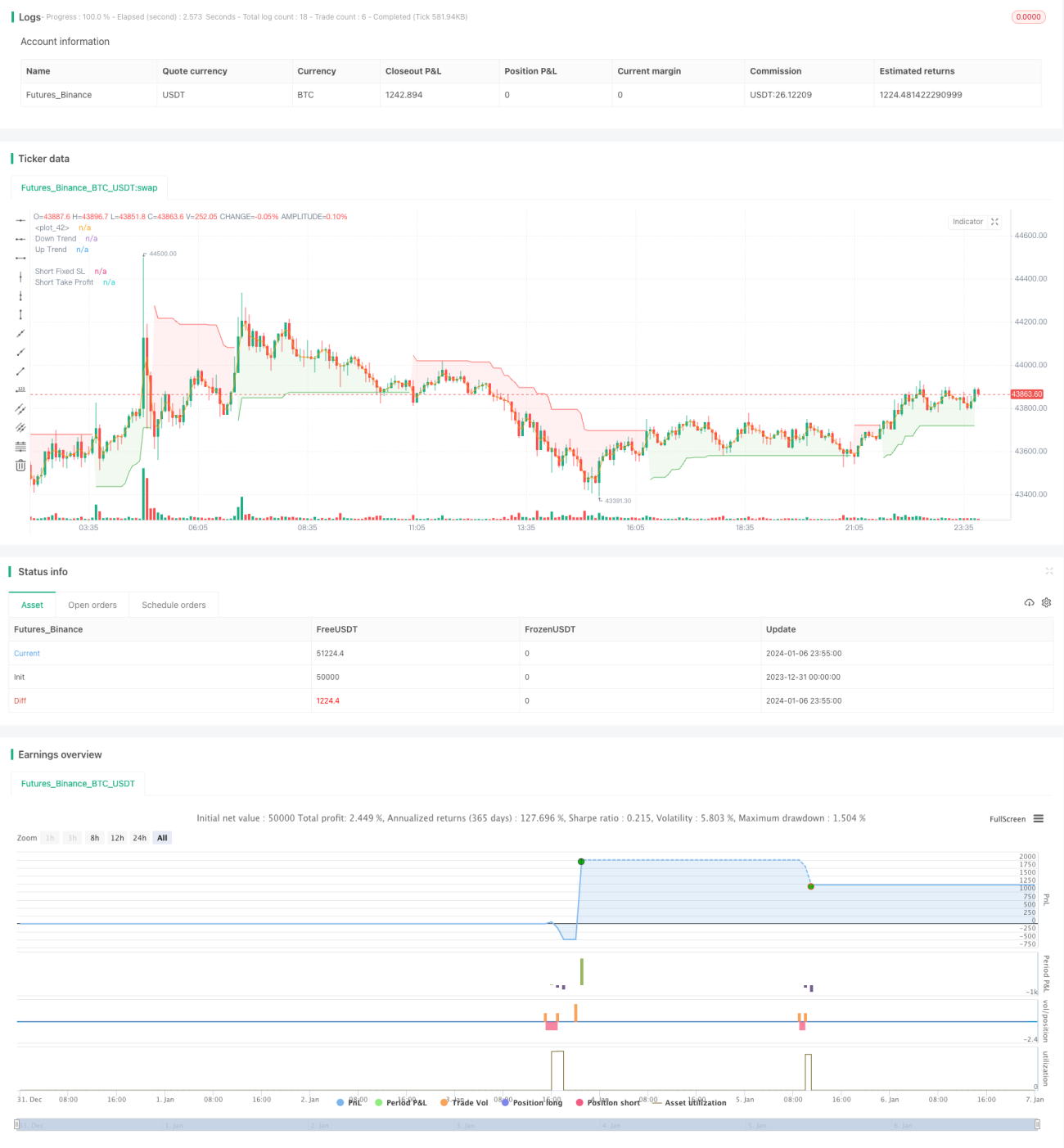

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1