দ্বৈত মুভিং এভারেজ ভিত্তিক অসিলেশন ট্রেডিং কৌশল

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি দ্বৈত মুভিং এভারেজ ভিত্তিক অসিলেশন ট্রেডিং কৌশল। এটি দ্রুত মুভিং এভারেজ ও ধীর মুভিং এভারেজের ক্রসওভারকে ক্রয় ও বিক্রয় সংকেত হিসেবে ব্যবহার করে। যখন দ্রুত মুভিং এভারেজ নিচ থেকে উপরে ধীর মুভিং এভারেজকে অতিক্রম করে, তখন ক্রয় সংকেত তৈরি হয়; আর যখন দ্রুত মুভিং এভারেজ উপরে থেকে নিচে ধীর মুভিং এভারেজকে অতিক্রম করে, তখন বিক্রয় সংকেত তৈরি হয়। কৌশলটি অসিলেটিং বাজারের জন্য উপযোগী এবং স্বল্পমেয়াদী মূল্যের ওঠানামা থেকে লাভ অর্জন করতে পারে।

কৌশলের নীতি

কৌশলটি দ্রুত মুভিং এভারেজ হিসেবে length ৬ এর RMA এবং ধীর মুভিং এভারেজ হিসেবে length ৪ এর HMA ব্যবহার করে। কৌশলটি দ্রুত ও ধীর লাইনের ক্রসওভারের মাধ্যমে মূল্যের প্রবণতা নির্ণয় করে এবং ট্রেডিং সংকেত তৈরি করে।

যখন দ্রুত লাইন নিচ থেকে উপরে ধীর লাইনকে অতিক্রম করে, তখন এটি নির্দেশ করে যে স্বল্পমেয়াদে মূল্য দরপতন থেকে দরবৃদ্ধিতে পরিবর্তিত হয়েছে, যা শেয়ার হস্তান্তরের উপযুক্ত সময়; তাই কৌশলটি এই মুহূর্তে ক্রয় সংকেত তৈরি করে। আর যখন দ্রুত লাইন উপরে থেকে নিচে ধীর লাইনকে অতিক্রম করে, তখন এটি নির্দেশ করে যে স্বল্পমেয়াদে মূল্য দরবৃদ্ধি থেকে দরপতনে পরিবর্তিত হয়েছে, যা শেয়ার হস্তান্তরের উপযুক্ত সময়; তাই কৌশলটি এই মুহূর্তে বিক্রয় সংকেত তৈরি করে।

এছাড়াও, কৌশলটি দীর্ঘমেয়াদী প্রবণতা নির্ণয় করে যাতে বিপরীতমুখী ট্রেডিং এড়ানো যায়। কেবলমাত্র যখন দীর্ঘমেয়াদী প্রবণতাও সেই সংকেতকে সমর্থন করে, তখনই প্রকৃত ক্রয় ও বিক্রয় সংকেত তৈরি হয়।

কৌশলের সুবিধা

কৌশলটির নিম্নলিখিত সুবিধা রয়েছে:

- দ্বৈত মুভিং এভারেজ ক্রসওভার ব্যবহার করে কার্যকরভাবে স্বল্পমেয়াদী মূল্য বিপরীতমুখী পয়েন্ট চিহ্নিত করা যায়।

- দ্রুত ও ধীর লাইনের দৈর্ঘ্যের সমন্বয় সঠিক, যা অপেক্ষাকৃত নির্ভুল ট্রেডিং সংকেত তৈরি করতে পারে।

- দীর্ঘ ও স্বল্পমেয়াদী প্রবণতা নির্ণয়ের সমন্বয় বেশিরভাগ নয়েজ ট্রেডিং সংকেত ফিল্টার করতে পারে।

- লাভ-লোকসান থামানোর লজিক বাস্তবায়িত হয়েছে, যা সক্রিয়ভাবে ঝুঁকি এড়াতে সাহায্য করে।

- বোঝা ও বাস্তবায়ন সহজ, কোয়ান্টিটেটিভ ট্রেডিং শুরুর শিক্ষার্থীদের জন্য উপযোগী।

ঝুঁকি ও সমাধান

কৌশলটির কিছু ঝুঁকিও রয়েছে:

-

দ্বৈত মুভিং এভারেজ কৌশলে প্রায়শই ছোট ছোট লাভ কিন্তু একবার বড় লোকসানের সম্ভাবনা থাকে। সমাধান: যথাযথভাবে লাভ-লোকসান থামানোর স্তর নির্ধারণ করা।

-

অসিলেটিং বাজারে ট্রেডিং সংকেত ঘন ঘন আসতে পারে, যা অতিরিক্ত ট্রেডিংয়ের কারণ হতে পারে। সমাধান: ট্রেডিং শর্ত কিছুটা শিথিল করে ট্রেডের সংখ্যা কমানো।

-

কৌশলের প্যারামিটার সহজেই অত্যধিক অপ্টিমাইজ করা হতে পারে, ফলে বাস্তব ট্রেডিংয়ে কার্যকারিতা কমে যায়। সমাধান: প্যারামিটারের রোবাস্টনেস টেস্ট করা।

-

ট্রেন্ডিং বাজারে কৌশলটি ভালো পারফর্ম করে না। সমাধান: ট্রেন্ড নির্ণয় মডিউল যুক্ত করা অথবা ট্রেন্ড কৌশলের সাথে সমন্বয় করে ব্যবহার করা।

অপ্টিমাইজেশনের দিকনির্দেশনা

কৌশলটি আরও অপ্টিমাইজ করার সম্ভাব্য দিক:

-

মুভিং এভারেজ সূচক আপডেট করে কালমান ফিল্টারের মতো অ্যাডাপটিভ ফিল্টার ব্যবহার করা।

-

মেশিন লার্নিং মডিউল যুক্ত করে কৃত্রিম বুদ্ধিমত্তার মাধ্যমে ক্রয়-বিক্রয় পয়েন্ট প্রশিক্ষণ দেওয়া।

-

ক্যাপিটাল ম্যানেজমেন্ট মডিউল যুক্ত করে ঝুঁকি নিয়ন্ত্রণকে আরও স্বয়ংক্রিয় করা।

-

উচ্চ-ফ্রিকোয়েন্সি ফ্যাক্টরের সাথে সমন্বয় করে শক্তিশালী ট্রেডিং সংকেত খুঁজে বের করা।

-

একাধিক সম্পদ ও ক্রস-মার্কেট আর্বিট্রেজ।

সারসংক্ষেপ

এই দ্বৈত মুভিং এভারেজ অসিলেশন কৌশলটি সামগ্রিকভাবে একটি সাধারণ ও কার্যকরী কোয়ান্টিটেটিভ ট্রেডিং কৌশল। এটির অভিযোজন ক্ষমতা বেশ ভালো, এবং শিক্ষার্থীরা এর মাধ্যমে কৌশল উন্নয়ন সম্পর্কে অনেক কিছু শিখতে পারে। একইসাথে, এতে আরও উন্নতির যথেষ্ট সুযোগ রয়েছে; আরও কোয়ান্টিটেটিভ টেকনিক যুক্ত করে অপ্টিমাইজ করলে আরও ভালো ফলাফল পাওয়া সম্ভব।

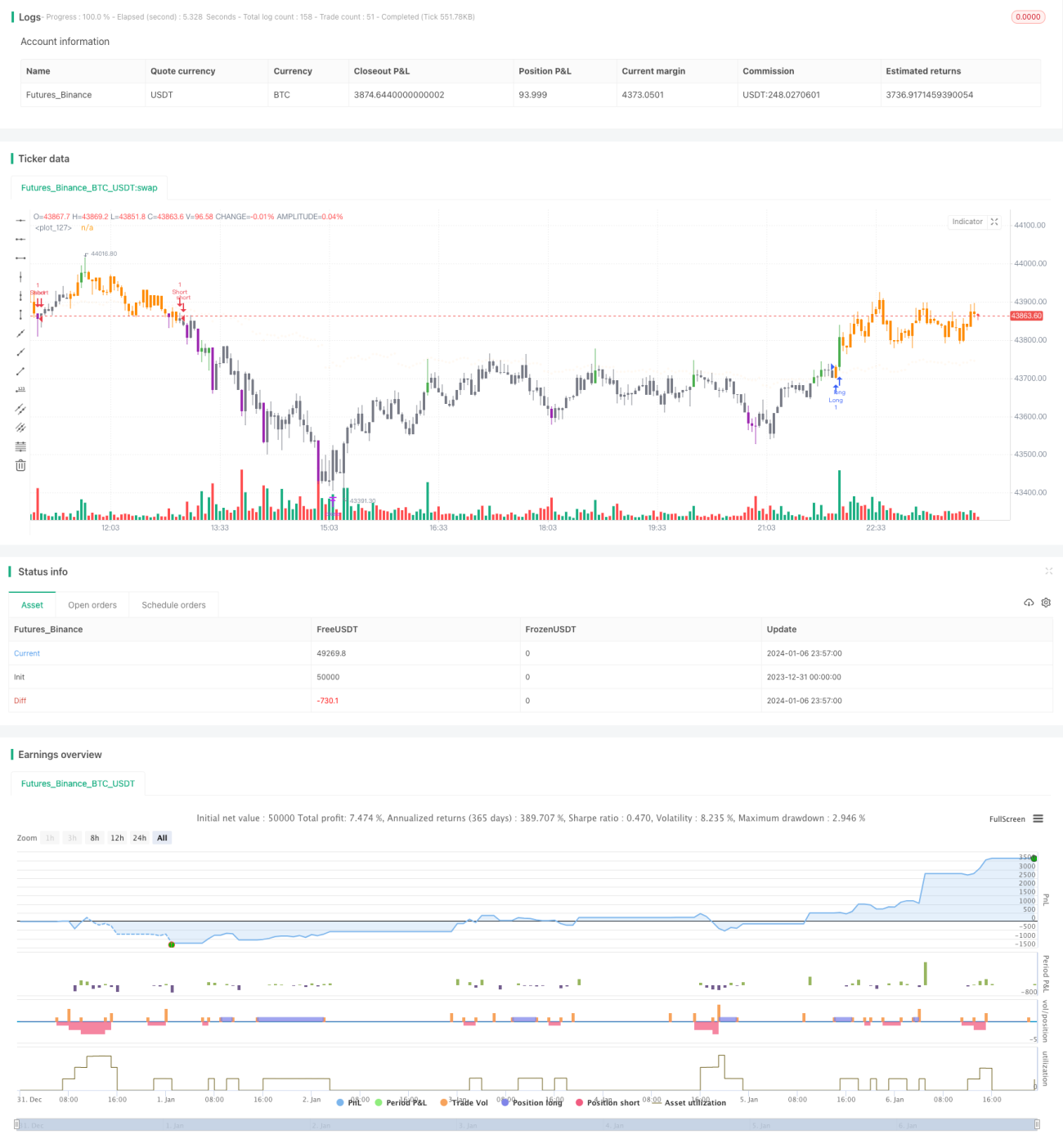

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1