বহু-সময়সীমা প্রবণতা অনুসরণ কৌশল

সারসংক্ষেপ

মাল্টি-টাইমফ্রেম ট্রেন্ড ট্র্যাকিং স্ট্র্যাটেজি একটি ট্রেন্ড ট্র্যাকিং কৌশল যা বিভিন্ন ধরনের মুভিং এভারেজ এবং রিগ্রেশন লাইনকে একীভূত করে। এই কৌশলটি ২০টিরও বেশি ভিন্ন ট্রেন্ড ইন্ডিকেটর থেকে নির্বাচন করে স্বয়ংক্রিয়ভাবে কেনা-বেচা করতে পারে।

কৌশলের নীতি

এই কৌশলের মূল ভিত্তি হল ব্যবহারকারীর নির্বাচিত ট্রেন্ড ইন্ডিকেটরের উপর ভিত্তি করে মূল্য ঊর্ধ্বমুখী না নিম্নমুখী ট্রেন্ডে আছে তা নির্ধারণ করা। কৌশলটি প্রথমে ২০টিরও বেশি মুভিং এভারেজ এবং রিগ্রেশন লাইন গণনা করে। এই ইন্ডিকেটরগুলির মধ্যে সাধারণ মুভিং এভারেজ, ওয়েটেড মুভিং এভারেজ, এক্সপোনেনশিয়াল মুভিং এভারেজ ইত্যাদি পাইন প্রোগ্রামিং ভাষার স্ট্যান্ডার্ড লাইব্রেরির সূচক এবং পাইন কমিউনিটি দ্বারা তৈরি কিছু কাস্টম সূচকও অন্তর্ভুক্ত। তারপর কৌশলটি এই সূচকগুলি থেকে বর্তমান সময়ের মান বের করে এবং পূর্ববর্তী পিরিয়ডের মানের সাথে তুলনা করে। যদি বর্তমান মান আগের মানের চেয়ে বড় হয়, তাহলে ট্রেন্ডটি ঊর্ধ্বমুখী;反之, যদি বর্তমান মান আগের মানের চেয়ে ছোট হয়, তাহলে ট্রেন্ডটি নিম্নমুখী। অবশেষে, কৌশলটি ট্রেন্ডের দিকের উপর ভিত্তি করে সিদ্ধান্ত নেয় যে লং পজিশন খোলা উচিত কিনা। ঊর্ধ্বমুখী ট্রেন্ডে লং পজিশন খোলা হয় এবং নিম্নমুখী ট্রেন্ডে পজিশন বন্ধ করা হয়।

সুবিধা বিশ্লেষণ

এই কৌশলটি ২০টিরও বেশি সূচককে একীভূত করে ট্রেন্ড নির্ধারণ করে, ফলে একক সূচকের ভুল বিচারের সম্ভাবনা হ্রাস পায়। তাছাড়া, এই সূচকগুলি কমিউনিটি ডেভেলপারদের দ্বারা যাচাই করা হয়েছে। বিভিন্ন প্যারামিটার ব্যবহার করে এগুলিকে বিভিন্ন বাজার পরিবেশের সাথে মানিয়ে নেওয়া যায়।

সাধারণ ডাবল মুভিং এভারেজ স্ট্র্যাটেজির তুলনায়, এই কৌশলটি ট্রেন্ডের দিক নির্ধারণের জন্য শুধুমাত্র একটি সূচকের উপর নির্ভর করে, যা ট্রেন্ডকে আরও ভালভাবে প্রকাশ করতে পারে এবং বিপরীতমুখী মিথ্যা সিগন্যাল এড়াতে পারে।

ঝুঁকি বিশ্লেষণ

এই কৌশলটি ট্রেন্ড নির্ধারণের জন্য সূচকের উপর নির্ভর করে, ফলে এটি ট্রেন্ডের মোড় পরিবর্তন চিহ্নিত করতে পারে না। এতে কিছুটা ল্যাগ তৈরি হয়, যা লোকসান বা সুযোগ হাতছাড়া করার কারণ হতে পারে। সূচকের প্যারামিটার সামঞ্জস্য করে এই সমস্যা কমানো যেতে পারে।

অপ্রত্যাশিত ঘটনার পরে, সমস্ত ট্রেন্ড ফলোয়িং স্ট্র্যাটেজি বড় লোকসানের সম্মুখীন হয়। ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস সেট করা প্রয়োজন।

উন্নতির দিকনির্দেশ

ট্রেন্ড মোড়ের পূর্বাভাস দিতে অন্য সূচকের সাথে মিলিয়ে বিচার করার কথা বিবেচনা করা যেতে পারে, যাতে ল্যাগের সমস্যা হ্রাস পায়। উদাহরণস্বরূপ, বোলিঞ্জার ব্যান্ডের সাথে মিলিয়ে মূল্য অতিরিক্ত প্রসারিত হয়েছে কিনা তা বিচার করা।

অপ্রত্যাশিত ঘটনার জন্য জরুরি স্টপ-লস ব্যবস্থা ডিজাইন করা যেতে পারে। যেমন, একদিনে ৫% এর বেশি ক্ষতি হলে বাধ্যতামূলক স্টপ-লস সক্রিয় করা।

সারসংক্ষেপ

মাল্টি-টাইমফ্রেম ট্রেন্ড ট্র্যাকিং স্ট্র্যাটেজি ২০টিরও বেশি সূচককে একীভূত করে ট্রেন্ড নির্ধারণ করে, যা বাজারের ট্রেন্ডকে পূর্ণরূপে প্রকাশ করতে পারে এবং মিথ্যা সিগন্যাল এড়াতে পারে। একই সাথে এটি উচ্চ কাস্টমাইজেশন ক্ষমতা ধরে রাখে, যা ভিন্ন ভিন্ন বাজার পরিবেশের জন্য উপযোগী করে তোলে। এটি একটি অত্যন্ত কার্যকর ট্রেন্ড ট্র্যাকিং কৌশল। যথাযথ স্টপ-লস নির্ধারণ এবং সূচকের প্যারামিটার অপটিমাইজেশনের মাধ্যমে ঝুঁকি নিয়ন্ত্রণ করে ভাল রিটার্ন অর্জন করা সম্ভব।

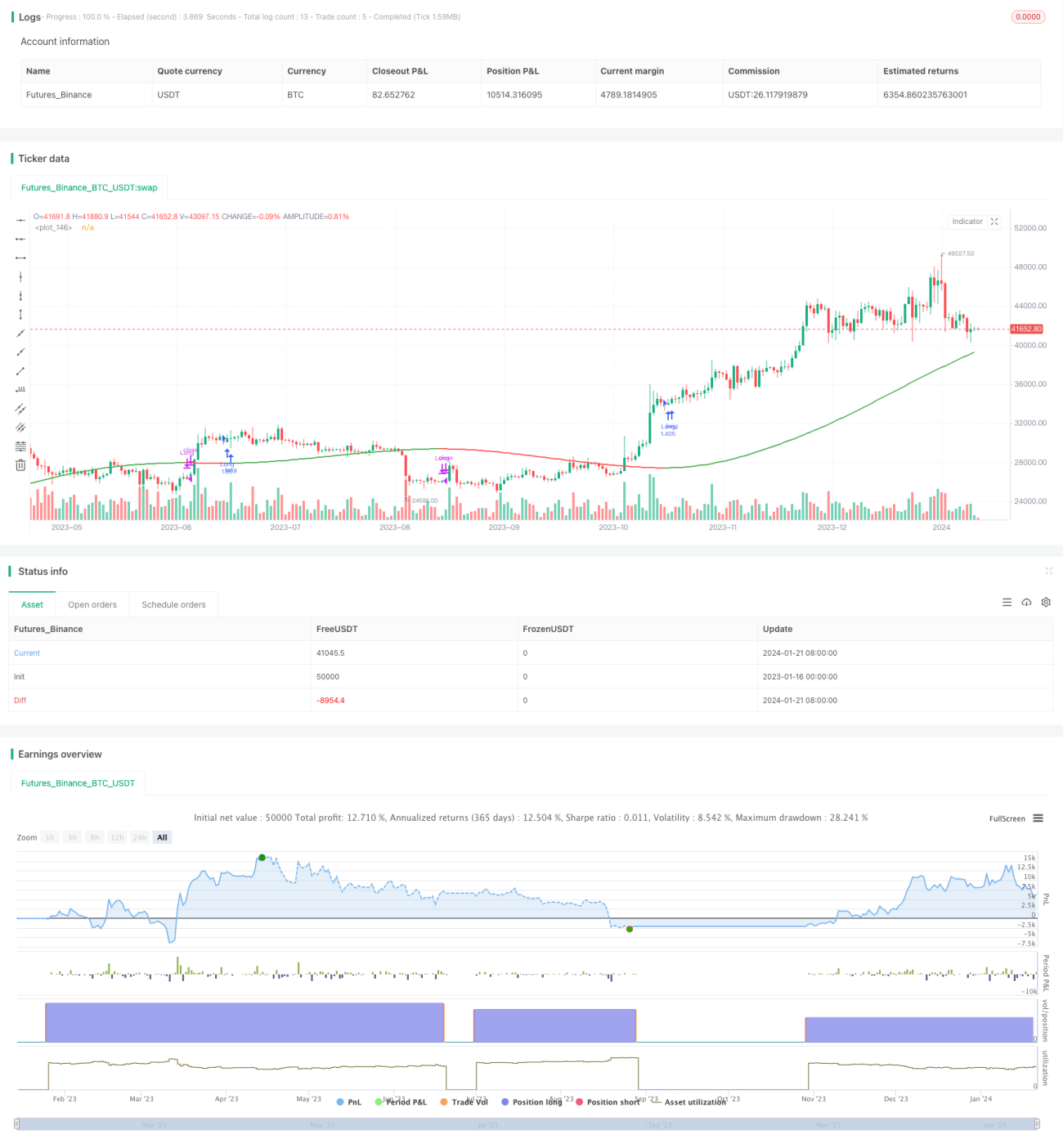

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1