দ্বিমুখী অভিযোজিত পরিসর ফিল্টার মোমেন্টাম ট্র্যাকিং কৌশল

সংক্ষিপ্ত বিবরণ

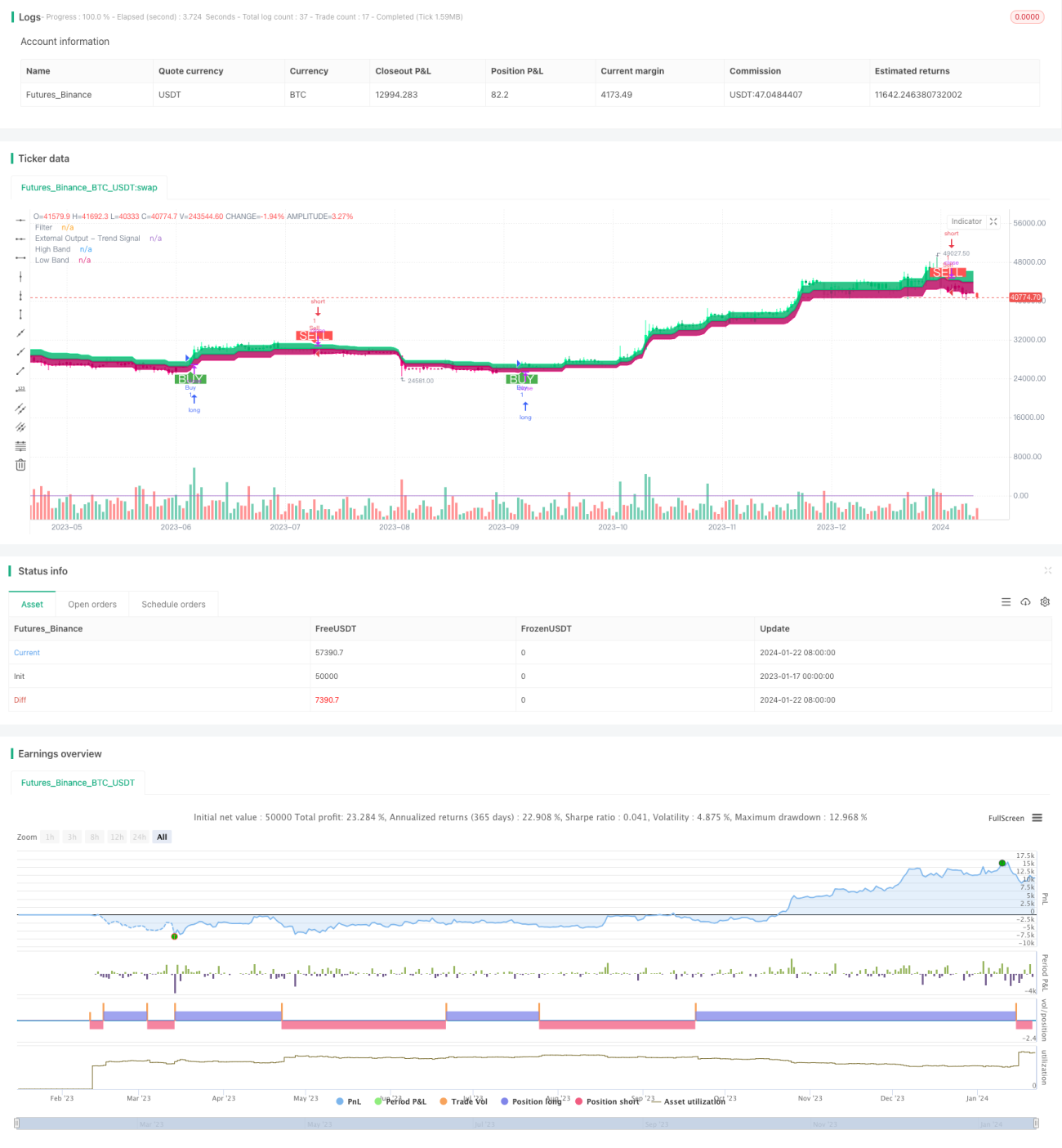

কৌশলটি একটি দ্বিমুখী অভিযোজিত রেঞ্জ ফিল্টার মোমেন্টাম ট্র্যাকিং কৌশল। এটি দামের ওঠানামা ট্র্যাক করতে অভিযোজিত রেঞ্জ ফিল্টার ব্যবহার করে এবং ভলিউম/এনার্জি ইন্ডিকেটরের সাথে মিলিয়ে মানের দিক নির্ধারণ করে, ফলে কমে কিনে বেশি দামে বিক্রি করা সম্ভব হয়।

কৌশলের নীতি

১. দামের ওঠানামা ট্র্যাক করতে অভিযোজিত রেঞ্জ ফিল্টার ব্যবহার করা হয়। ফিল্টারের আকার ব্যবহারকারীর নির্ধারিত রেঞ্জ পিরিয়ড, সংখ্যা ও স্কেল অনুযায়ী স্বয়ংক্রিয়ভাবে সামঞ্জস্য হয়।

২. ফিল্টার দুটি প্রকারে বিভক্ত: টাইপ ১ (স্ট্যান্ডার্ড রেঞ্জ ট্র্যাকিং) এবং টাইপ ২ (স্টেপ রাউন্ডিং)।

৩. ফিল্টার ও ক্লোজিং প্রাইসের আপেক্ষিক অবস্থানের ভিত্তিতে দামের ওঠানামার দিক নির্ধারণ করা হয়। উপরের ব্যান্ডের উপরে থাকলে বুলিশ, নিচের ব্যান্ডের নিচে থাকলে বিয়ারিশ।

৪. পূর্ববর্তী দিনের তুলনায় ক্লোজিং প্রাইসের পরিবর্তনের সাথে মিলিয়ে মানের দিক নির্ধারণ করা হয়। মান বাড়লে লং, কমলে শর্ট।

৫. যখন দাম উপরের ব্যান্ড ভেঙে উপরে যায় এবং মান বৃদ্ধি পায়, তখন বাই সিগন্যাল জেনারেট হয়; আর যখন দাম নিচের ব্যান্ড ভেঙে নিচে যায় এবং মান হ্রাস পায়, তখন সেল সিগন্যাল জেনারেট হয়।

সুবিধা বিশ্লেষণ

১. অভিযোজিত রেঞ্জ ফিল্টার বাজারের ওঠানামা নির্ভুলভাবে ধরতে পারে।

২. দুটি প্রকারের ফিল্টার বিভিন্ন ট্রেডিং পছন্দের জন্য উপযোগী।

৩. ভলিউম/এনার্জি ইন্ডিকেটর ব্যবহার করে মানের দিক কার্যকরভাবে শনাক্ত করা যায়।

৪. কৌশলটি নমনীয়, বাজার অনুযায়ী প্যারামিটার সামঞ্জস্য করা যায়।

৫. উপযুক্ত ট্রেডিং কন্ডিশন লজিক নির্বাচন করে কাস্টমাইজ করা সম্ভব।

ঝুঁকি বিশ্লেষণ

১. প্যারামিটার সেটিং ঠিক না হলে অতিরিক্ত ট্রেডিং বা মিসড অর্ডার হতে পারে।

২. ব্রেকআউট সিগন্যাল কিছুটা ল্যাগ নিয়ে আসে।

৩. ভলিউম/এনার্জি ইন্ডিকেটরের কিছুটা জামিং ঝুঁকি থাকে।

৪. রেঞ্জ ব্রেকআউটে ফাঁদে পড়ার সম্ভাবনা থাকে।

ঝুঁকি প্রতিরোধ:

১. উপযুক্ত প্যারামিটার কম্বিনেশন নির্বাচন করে সময়মতো সামঞ্জস্য করুন।

২. ট্রেন্ড শনাক্ত করতে অন্যান্য ইন্ডিকেটর ব্যবহার করুন।

৩. গুরুত্বপূর্ণ লেভেলের কাছে ও ট্রেন্ড রিভার্সালের সময় সতর্কতার সাথে ট্রেড করুন।

অপ্টিমাইজেশন দিকনির্দেশনা

১. বিভিন্ন রেঞ্জ সাইজ ও স্মুথিং পিরিয়ড কম্বিনেশন পরীক্ষা করে সর্বোত্তম কম্বিনেশন খুঁজুন।

২. বিভিন্ন ফিল্টার টাইপ চেষ্টা করে ব্যক্তিগত পছন্দের টাইপ নির্বাচন করুন।

৩. অন্যান্য ভলিউম/এনার্জি ইন্ডিকেটর বা সহায়ক টেকনিক্যাল ইন্ডিকেটর ব্যবহার করে দেখুন।

৪. অযৌক্তিক ট্রেডিং কমাতে ট্রেডিং কন্ডিশন লজিক অপ্টিমাইজ ও সামঞ্জস্য করুন।

৫. বাজারের প্যাটার্ন তত্ত্বের সাথে মিলিয়ে স্বয়ংক্রিয়ভাবে পজিশন সাইজিং নির্ধারণ করুন।

- 1