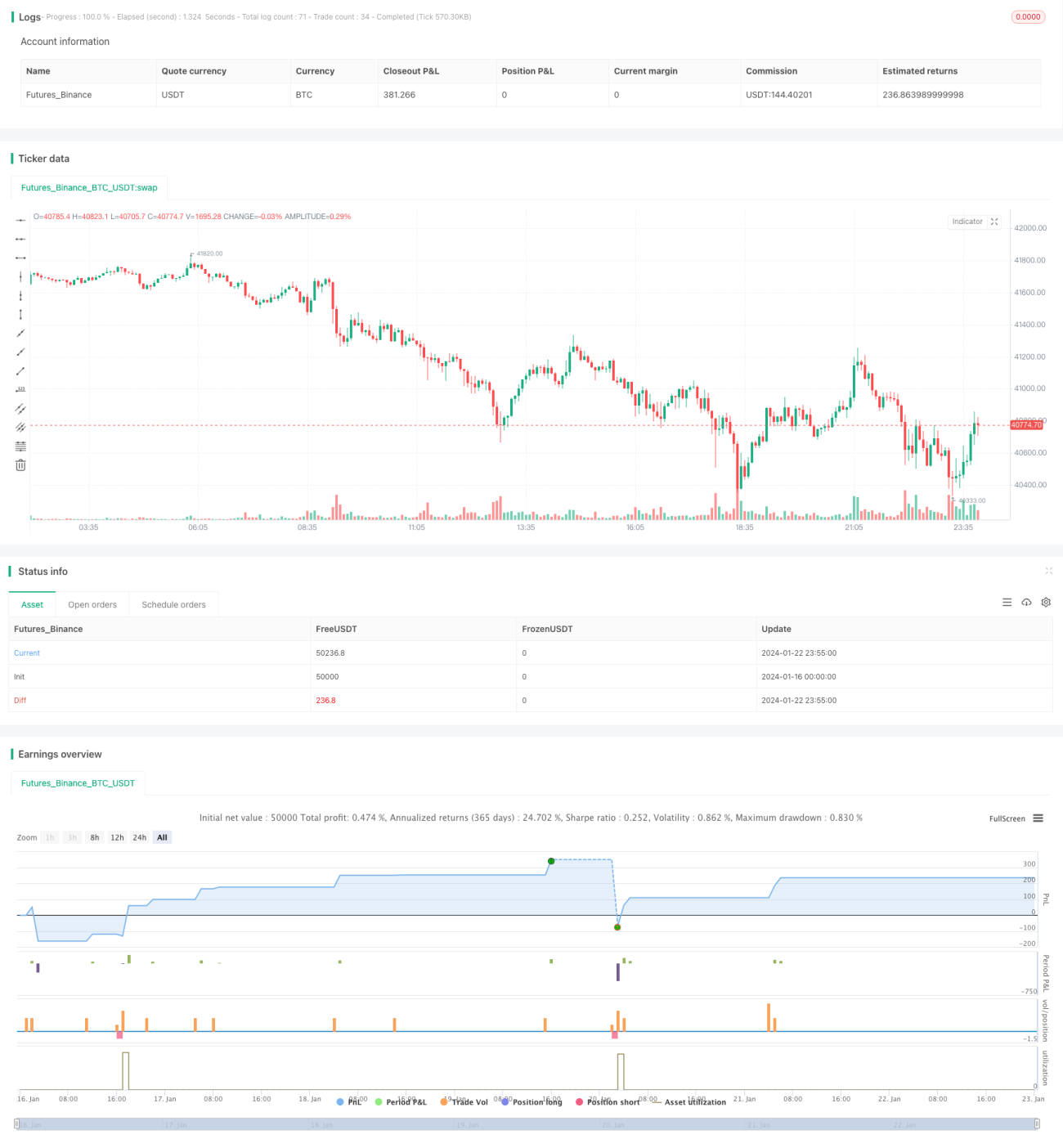

RSI সূচক এবং গড় মান সূচক ব্যবহার করে একটি পরিমাণগত কৌশল

সারসংক্ষেপ

ডাবল RSI মুভিং এভারেজ ব্রেকআউট কৌশলটি একটি কোয়ান্টিটেটিভ ট্রেডিং কৌশল যা একই সাথে RSI সূচক এবং মুভিং এভারেজ সূচক ব্যবহার করে ট্রেডিংয়ের সময় নির্ধারণ করে। এই কৌশলের মূল ধারণা হলো, যখন RSI সূচক ওভারবট বা ওভারসোল্ড অঞ্চলে পৌঁছায়, তখন মুভিং এভারেজের দিক ব্যবহার করে সংকেত ফিল্টার করা এবং ভালো ব্রেকআউট পয়েন্ট খুঁজে পজিশন খোলা।

কৌশলের নীতি

- ব্যবহারকারীর নির্ধারিত প্যারামিটার অনুযায়ী, যথাক্রমে RSI সূচক এবং সরল মুভিং এভারেজ (SMA) গণনা করা হয়।

- যখন RSI নির্ধারিত ওভারসোল্ড লাইন (ডিফল্ট 30) উপরে উঠে যায়, তখন যদি দাম LONG এক্সিট মুভিং এভারেজের নিচে থাকে, তবে লং সিগন্যাল তৈরি হয়।

- যখন RSI নির্ধারিত ওভারবট লাইন (ডিফল্ট 70) নিচে নামে, তখন যদি দাম SHORT এক্সিট মুভিং এভারেজের উপরে থাকে, তবে শর্ট সিগন্যাল তৈরি হয়।

- ব্যবহারকারী একটি ফিল্টার মুভিং এভারেজ নির্বাচন করতে পারেন; দাম যখন ফিল্টার মুভিং এভারেজের উপরে থাকবে, তখনই সিগন্যাল তৈরি হবে।

- পজিশন থেকে বের হওয়ার সিদ্ধান্ত LONG এক্সিট মুভিং এভারেজ এবং SHORT এক্সিট মুভিং এভারেজের ভিত্তিতে নেওয়া হয়।

সুবিধা বিশ্লেষণ

- দ্বৈত সূচক নকশা, বাজারের দুটি গুরুত্বপূর্ণ বিষয় একসঙ্গে বিবেচনা করে সিদ্ধান্তের নির্ভুলতা বাড়ায়।

- RSI সূচকের রিভার্সাল বৈশিষ্ট্যের যথাযথ ব্যবহার করে রিভার্সালের সময় খুঁজে পাওয়া যায়।

- মুভিং এভারেজ ফিল্টারিং সিদ্ধান্তের কঠোরতা বাড়ায়, উচ্চ মূল্যে কেনা এবং নিম্ন মূল্যে বিক্রি এড়ায়।

- কাস্টমাইজযোগ্য প্যারামিটার, বিভিন্ন পণ্য এবং সময়কালের জন্য অপ্টিমাইজ করা যায়।

- সরল লজিক ডিজাইন, সহজে বোঝা এবং পরিবর্তন করা যায়।

ঝুঁকি বিশ্লেষণ

- RSI সূচকে প্রায়ই ভার্টিকাল নেক লাইন তৈরি হয়, Density সূচক এই সমস্যা কমাতে পারে।

- বড় সময়কালে RSI প্রায়ই অকার্যকর হয়, প্যারামিটার অপ্টিমাইজেশন বা অন্যান্য সূচক সাহায্য নেওয়া যেতে পারে।

- মুভিং এভারেজে পিছিয়ে থাকার সমস্যা আছে, মুভিং এভারেজের দৈর্ঘ্য কমিয়ে বা MACD-এর মতো সূচক ব্যবহার করে সমাধান করা যায়।

- সরল শর্তাবলী, আরও সূচক যুক্ত করে ট্রেডিং সিগন্যালের কার্যকারিতা নিশ্চিত করা যেতে পারে।

অপ্টিমাইজেশন দিকনির্দেশনা

- RSI প্যারামিটার অপ্টিমাইজ করা বা Density সূচক প্রবর্তন করে মিথ্যা সিগন্যালের সম্ভাবনা কমানো।

- DMI, BOLL-এর মতো ট্রেন্ড এবং ভোলাটিলিটি সূচকের সাথে একত্রিত করে ট্রেন্ড এবং সাপোর্ট লেভেল নির্ধারণ করা।

- মুভিং এভারেজের পরিবর্তে বা সহায়ক হিসেবে MACD-এর মতো সূচক যুক্ত করা।

- পজিশন খোলার শর্ত লজিক বাড়ানো, অবাঞ্ছিত ব্রেকআউট সিগন্যাল প্রতিরোধ করা।

সারসংক্ষেপ

ডাবল RSI মুভিং এভারেজ ব্রেকআউট কৌশলটি RSI সূচক ব্যবহার করে ওভারবট/ওভারসোল্ড শনাক্তকরণ এবং মুভিং এভারেজ ব্যবহার করে ট্রেন্ড নির্ধারণের পদ্ধতিকে একত্রিত করে, যা তাত্ত্বিকভাবে রিভার্সাল সুযোগ কার্যকরভাবে ধরতে পারে। এই কৌশলটি নমনীয় এবং সরল, সহজে বোঝা যায় এবং বিভিন্ন পণ্যের জন্য অপ্টিমাইজ করা যায়, যা একটি প্রস্তাবিত কোয়ান্টিটেটিভ ট্রেডিংয়ের প্রাথমিক কৌশল। আরও সূচক যুক্ত করে সিদ্ধান্তকে সমর্থন করলে এই কৌশল আরও উন্নত হতে পারে এবং লাভের সম্ভাবনা বাড়াতে পারে।

- 1