আরএসআই সূচকের সাকশন কাপ ট্রেডিং কৌশল

সারসংক্ষেপ

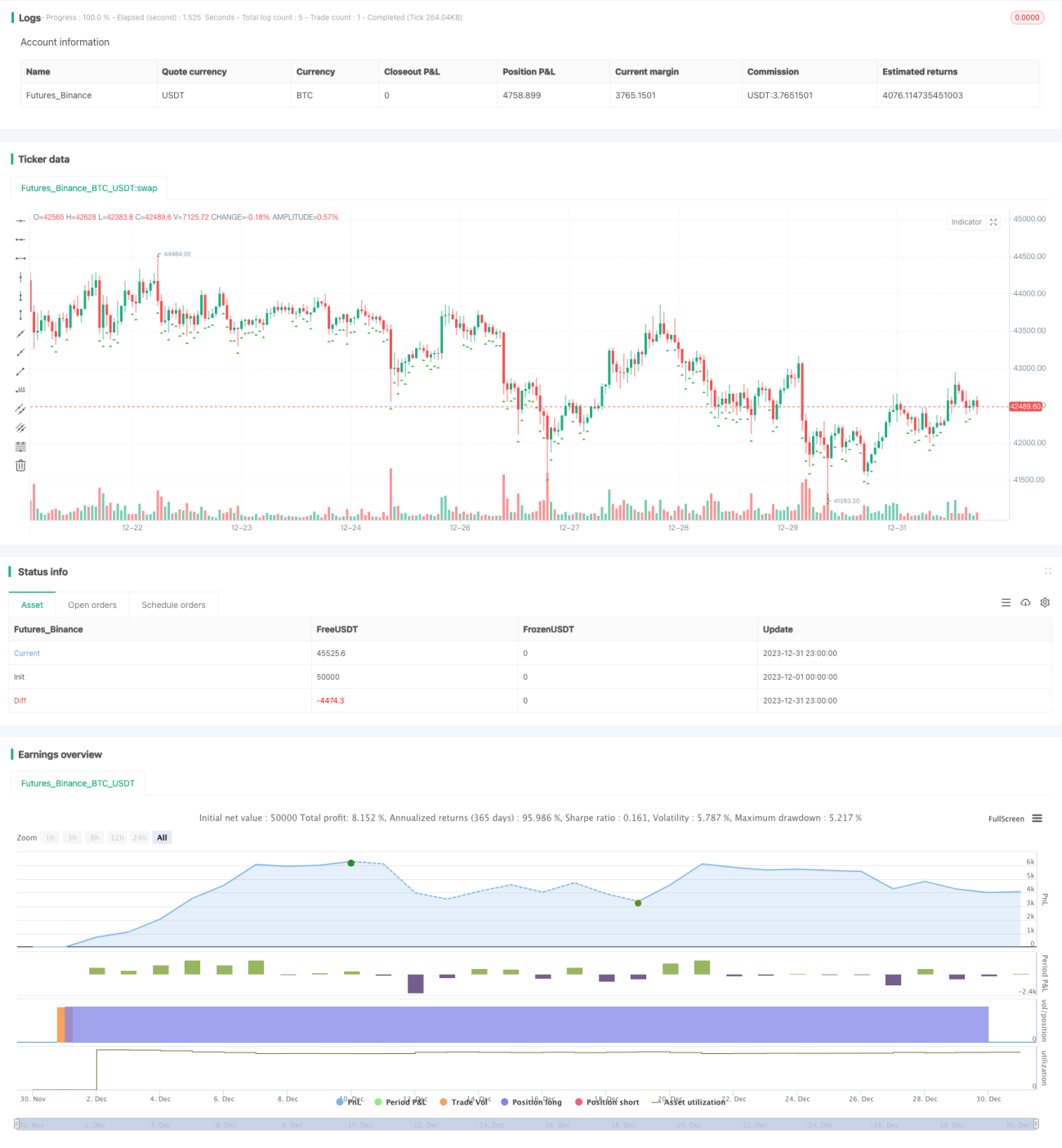

RSI সূচক সাকশন ট্রেডিং কৌশল হল একটি নির্দিষ্ট গ্রিড ট্রেডিং পদ্ধতি যা RSI এবং CCI প্রযুক্তিগত সূচকগুলিকে একীভূত করে। এই কৌশলটি RSI এবং CCI সূচকের মান অনুসারে প্রবেশের সময় নির্ণয় করে, নির্দিষ্ট লাভের অনুপাত এবং নির্দিষ্ট গ্রিড সংখ্যা ব্যবহার করে টেক প্রফিট অর্ডার এবং অ্যাড পজিশন অর্ডার সেট করে। একই সাথে, কৌশলটিতে বিরতিমূলক মূল্য পরিবর্তনের জন্য হেজিং প্রক্রিয়াও একীভূত করা হয়েছে।

কৌশল নীতি

প্রবেশের শর্ত

যখন 5 মিনিট এবং 30 মিনিটের RSI সূচক উভয়ই নির্ধারিত থ্রেশহোল্ডের নিচে থাকে, এবং 1 ঘন্টার CCI সূচকও নির্ধারিত মানের নিচে থাকে, তখন লং সিগন্যাল তৈরি হয়। এই সময়ে বর্তমান ক্লোজ মূল্যকে প্রবেশ মূল্য হিসেবে রেকর্ড করা হয় এবং অ্যাকাউন্ট ইকুইটি ও গ্রিড সংখ্যার ভিত্তিতে প্রথম পজিশনের পরিমাণ গণনা করা হয়।

লাভ বন্ধের শর্ত

প্রবেশ মূল্যকে ভিত্তি ধরে, নির্ধারিত লক্ষ্য লাভের অনুপাত অনুসারে লাভের মূল্য গণনা করা হয় এবং সেই মূল্য স্তরে টেক প্রফিট অর্ডার সেট করা হয়।

পজিশন যোগ করার শর্ত

প্রথম পজিশন ছাড়াও, বাকি নির্দিষ্ট পজিশনের অ্যাড অর্ডারগুলি প্রবেশ সিগন্যালের পরে একে একে প্রকাশ করা হয়, যতক্ষণ না নির্ধারিত গ্রিড সংখ্যায় পৌঁছায়।

হেজিং প্রক্রিয়া

যদি মূল্য প্রবেশ মূল্যের তুলনায় নির্ধারিত হেজ থ্রেশহোল্ড শতাংশের বেশি বেড়ে যায়, তাহলে সমস্ত পজিশন হেজ করে বন্ধ করা হয়।

বিপরীতমুখী প্রক্রিয়া

যদি মূল্য প্রবেশ মূল্যের তুলনায় নির্ধারিত বিপরীতমুখী থ্রেশহোল্ড শতাংশের বেশি কমে যায়, তাহলে সমস্ত অপূর্ণ অর্ডার বাতিল করা হয় এবং নতুন প্রবেশের সুযোগের জন্য অপেক্ষা করা হয়।

সুবিধা বিশ্লেষণ

- RSI এবং CCI উভয় সূচককে একত্রিত করে লাভের সম্ভাবনা বৃদ্ধি করা

- নির্দিষ্ট গ্রিড ব্যবহার করে লক্ষ্য লাভ নির্ধারণ করা, যা লাভের নিশ্চয়তা বাড়ায়

- হেজিং প্রক্রিয়া একীভূত করা, যা দামের তীব্র ওঠানামার ঝুঁকি কার্যকরভাবে প্রতিরোধ করে

- বিপরীতমুখী প্রক্রিয়া সংযোজন, যা ক্ষতি কমাতে সাহায্য করে

ঝুঁকি বিশ্লেষণ

- সূচকগুলি ভুল সংকেত তৈরি করার সম্ভাবনা

- দামের তীব্র ওঠানামা হেজ থ্রেশহোল্ড ভেঙে ফেলা

- বিপরীতমুখী হওয়ার পর আবার ঘুরে ফিরে প্রবেশ করতে না পারা

সূচক প্যারামিটার সমন্বয়, হেজের পরিসর বাড়ানো এবং বিপরীতমুখী পরিসর কমানোর মাধ্যমে এই ঝুঁকিগুলি কমানো যেতে পারে।

অপ্টিমাইজেশন দিকনির্দেশনা

- আরো বিভিন্ন ধরনের সূচক কম্বিনেশন পরীক্ষা করা যেতে পারে

- অভিযোজিত টেক প্রফিট প্রক্রিয়া নিয়ে গবেষণা করা যেতে পারে

- পজিশন যোগ করার লজিক অপ্টিমাইজ করা যেতে পারে

সারাংশ

RSI সূচক সাকশন ট্রেডিং কৌশল সূচকের মাধ্যমে প্রবেশের সময় নির্ণয় করে এবং নির্দিষ্ট গ্রিডের মাধ্যমে টেক প্রফিট ও পজিশন যোগ করে স্থিতিশীল লাভ লক করে। একই সাথে, কৌশলটিতে বড় ওঠানামার বিরুদ্ধে হেজিং এবং বিপরীতমুখী হওয়ার পরে পুনরায় প্রবেশের প্রক্রিয়া রয়েছে। এই বহু-প্রক্রিয়া সমন্বিত কৌশলটি ট্রেডিং ঝুঁকি কমাতে এবং লাভের হার বাড়াতে ব্যবহার করা যেতে পারে। সূচক ও প্যারামিটার সেটিংস আরও অপ্টিমাইজ করে, আরও ভালো বাস্তব ট্রেডিং ফলাফল পাওয়া যেতে পারে।

- 1