ক্যান্ডেলস্টিকের ওপর ভিত্তি করে দ্বিমুখী ব্রেকআউট ট্রেডিং কৌশল

ওভারভিউ

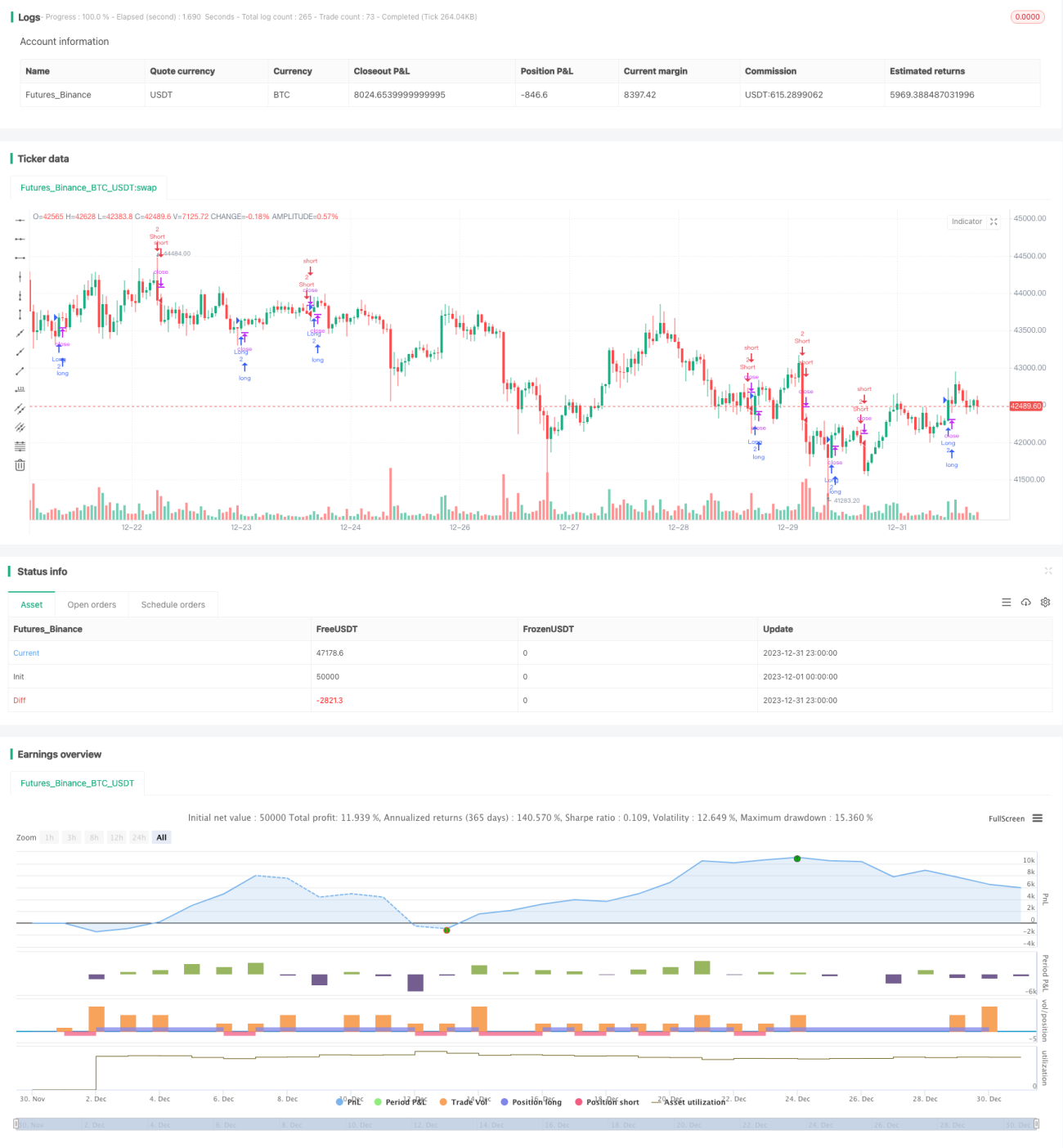

এটি একটি ক্যান্ডেলস্টিক-ভিত্তিক দ্বি-মুখী ব্রেকআউট ট্রেডিং কৌশল। এটি তখন ট্রেডিং সিগন্যাল তৈরি করে যখন বর্তমান ক্যান্ডেলের ক্লোজিং প্রাইস আগের দুটি ক্যান্ডেলের সর্বোচ্চ এবং সর্বনিম্ন মূল্য উভয়কেই ভেঙ্গে যায়।

কৌশলের নীতি

কৌশলটির মৌলিক যুক্তি হল:

-

বুল সিগন্যাল সংজ্ঞায়িত করা:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]। অর্থাৎ, বর্তমান ক্যান্ডেলের ক্লোজিং প্রাইস ওপেন প্রাইসের চেয়ে বেশি এবং আগের দুটি ক্যান্ডেলের সর্বোচ্চ মূল্যের চেয়ে বেশি, এবং বর্তমান ক্যান্ডেলের সর্বনিম্ন মূল্য আগের ক্যান্ডেলের সর্বনিম্ন মূল্যের চেয়ে কম। -

বিয়ার সিগন্যাল সংজ্ঞায়িত করা:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]। অর্থাৎ, বর্তমান ক্যান্ডেলের ক্লোজিং প্রাইস ওপেন প্রাইসের চেয়ে কম এবং আগের দুটি ক্যান্ডেলের সর্বনিম্ন মূল্যের চেয়ে কম, এবং বর্তমান ক্যান্ডেলের সর্বোচ্চ মূল্য আগের ক্যান্ডেলের সর্বোচ্চ মূল্যের চেয়ে বেশি। -

বুল সিগন্যাল ট্রিগার হলে লং পজিশন নিন; বিয়ার সিগন্যাল ট্রিগার হলে শর্ট পজিশন নিন।

-

স্টপ লস এবং টেক প্রফিট লেভেল সেট করা যায়।

কৌশলটি দ্বি-মুখী ব্রেকআউটের বৈশিষ্ট্য ব্যবহার করে, মূল্য নির্ধারিত জোন ভেঙে ট্রেন্ড পরিবর্তন বুঝতে এবং ট্রেডিং সিগন্যাল তৈরি করতে।

সুবিধা বিশ্লেষণ

এটি একটি অপেক্ষাকৃত সহজ এবং স্বজ্ঞাত ব্রেকআউট কৌশল, যার নিচের সুবিধাগুলি রয়েছে:

-

যুক্তি পরিষ্কার, বুঝতে ও বাস্তবায়ন করা সহজ, প্রবেশের বাধা কম।

-

ব্রেকআউট একটি সাধারণ ট্রেডিং সিগন্যাল, যা ট্রেন্ড গঠনে সহায়তা করে।

-

একই সাথে লং এবং শর্ট করতে পারে, দ্বি-মুখী ট্রেডিংয়ের সুযোগ দেয়, যা লাভের সম্ভাবনা বাড়ায়।

-

স্টপ লস ও টেক প্রফিট নমনীয়ভাবে সেট করে ঝুঁকি নিয়ন্ত্রণ করা যায়।

ঝুঁকি বিশ্লেষণ

কৌশলটির কিছু ঝুঁকি রয়েছে:

-

দ্বি-মুখী ট্রেডিংয়ে ঝুঁকি বেশি, তাই ঘনিষ্ঠভাবে পর্যবেক্ষণ করা প্রয়োজন।

-

ব্রেকআউট মিথ্যা সিগন্যাল তৈরি করতে পারে এবং ফাঁদে ফেলতে পারে।

-

প্যারামিটার ঠিকমতো না সেট করলে অতিরিক্ত ট্রেডিং হতে পারে।

-

স্টপ লস ও টেক প্রফিট ঠিকমতো না সেট করলে লাভের জায়গাও প্রভাবিত হতে পারে।

প্যারামিটার অপ্টিমাইজ করে এবং উপযুক্ত পণ্যগুলি বেছে নিয়ে ঝুঁকি কমানো যেতে পারে।

অপ্টিমাইজেশন দিক

কৌশলটি নিচের দিক থেকে অপ্টিমাইজ করা যেতে পারে:

-

প্যারামিটার অপ্টিমাইজেশন, যেমন ব্রেকআউট পিরিয়ড প্যারামিটার, স্টপ লস ও টেক প্রফিটের মাত্রা ইত্যাদি।

-

ফিল্টারিং শর্ত যুক্ত করা, যেমন আর্বিট্রেজ, রেঞ্জবাউন্ড মার্কেটে ভুল সিগন্যাল এড়ানো।

-

ট্রেন্ড ইন্ডিকেটর যুক্ত করে কনসলিডেশন জোন এড়ানো।

-

মানি ম্যানেজমেন্ট অপ্টিমাইজ করা এবং পজিশন সাইজিং অ্যালগরিদম উন্নত করা।

-

বিভিন্ন পণ্যের জন্য ভিন্ন প্যারামিটার থাকতে পারে, তাই আলাদাভাবে টেস্ট ও অপ্টিমাইজ করা উচিত।

সারসংক্ষেপ

এটি একটি দ্বি-মুখী ব্রেকআউট ধারণার উপর ভিত্তি করে সরল কৌশল। এর যুক্তি পরিষ্কার এবং বাস্তবায়ন সহজ, তবে পর্যবেক্ষণ ঝুঁকিও বিদ্যমান। প্যারামিটার এবং শর্ত অপ্টিমাইজ করে কৌশলটি থেকে ভাল ফলাফল আশা করা যেতে পারে।

- 1