ধৈর্য সহকারে কে-লাইন থেকে মূল্যবান তথ্য বের করার ট্রিপল মুভিং এভারেজ সুইং স্ট্র্যাটেজি

ওভারভিউ

ট্রিপল মুভিং এভারেজ সুইং কৌশলটি একাধিক মুভিং এভারেজ ইন্ডিকেটর ব্যবহার করে এবং ক্যান্ডেলস্টিকের গভীর বিশ্লেষণের মাধ্যমে দামের ওঠানামার মধ্যে লুকিয়ে থাকা নিয়মাবলী উন্মোচন করে, যা কম-ঝুঁকিপূর্ণ আর্বিট্রেজ ট্রেডিং সক্ষম করে।

কৌশলের নীতি

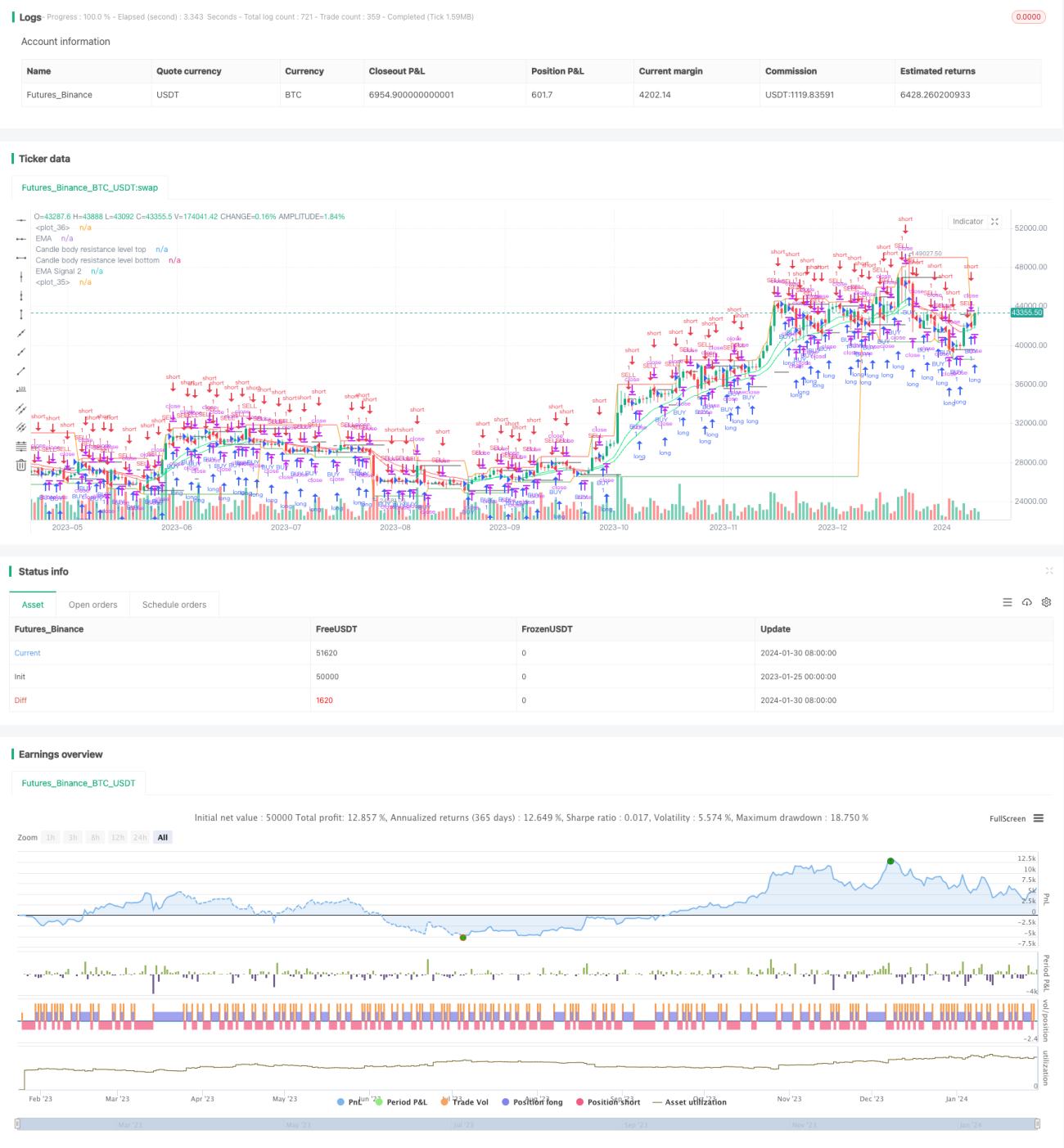

এই কৌশলটি বোলিঙ্গার ব্যান্ডের উপর ভিত্তি করে একাধিক EMA নির্দেশক যোগ করে একটি মূল্য চ্যানেল তৈরি করে এবং দামের ওঠানামার ধরণ খুঁজে বের করে। নির্দিষ্টভাবে:

- ক্যান্ডেলস্টিকের দেহের রেজিস্ট্যান্স লেভেল আঁকার জন্য BodyResistanceChannel নির্দেশক ব্যবহার করা হয়।

- বহুদিনের সাপোর্ট ও রেজিস্ট্যান্স লেভেল আঁকার জন্য Support/Resistance নির্দেশক ব্যবহার করা হয়।

- দ্বৈত EMA সিস্টেমের মাধ্যমে দামের ট্রেন্ডের দিক নির্ধারণ করা হয়।

- মূল্য বক্ররেখা মসৃণ করার জন্য Hull মুভিং এভারেজ নির্দেশক ব্যবহার করা হয়।

এই ভিত্তিতে প্যাটার্ন রিকগনিশনের সাথে মিলিয়ে রিভার্সাল সুযোগ চিহ্নিত করে আর্বিট্রেজ ট্রেডিং কৌশল তৈরি করা হয়।

সুবিধা বিশ্লেষণ

এই কৌশলের নিম্নলিখিত সুবিধাগুলি রয়েছে:

- একাধিক EMA দিয়ে মূল্য চ্যানেল তৈরি করায় দামের ওঠানামার দিক স্পষ্টভাবে নির্ধারণ করা যায়।

- Hull মুভিং এভারেজ নির্দেশক ব্যবহার করে মূল্য ব্রেকআউটের সিদ্ধান্ত কার্যকরভাবে মসৃণ করা যায়।

- রিভার্সাল প্যাটার্ন ও চ্যানেল নির্দেশক সমন্বয়ের মাধ্যমে উচ্চ সম্ভাবনা ও কম ঝুঁকির ট্রেডিং সম্ভব।

- বহুস্তরীয় নির্দেশক ব্যবস্থা তৈরি হওয়ায় ট্রেডিং সিগন্যাল স্থিতিশীল ও নির্ভরযোগ্য।

ঝুঁকি বিশ্লেষণ

এই কৌশলের নিম্নলিখিত ঝুঁকিও রয়েছে:

- মূল্য চ্যানেল ভেঙে গেলে ব্যাপক ক্ষতির ঝুঁকি। এর সমাধান হিসেবে মুভিং স্টপ-লস ব্যবহার করে একক ট্রেডের ক্ষতি কমানো যায়।

- রিভার্সাল প্যাটার্ন ভুল চিহ্নিত করলে ভুল সিগন্যালের ঝুঁকি। এর সমাধান হিসেবে প্যারামিটার অপ্টিমাইজ করে প্যাটার্ন চিহ্নিতকরণের নির্ভুলতা বাড়ানো যায়।

- নির্দেশক প্যারামিটারের অমিলের কারণে ট্রেডিং সিগন্যালের মান কমে যাওয়ার ঝুঁকি। এর সমাধান হিসেবে একাধিক প্যারামিটার সমন্বয় অপ্টিমাইজেশন পরীক্ষা করা যায়।

অপ্টিমাইজেশনের দিকনির্দেশনা

এই কৌশলের প্রধান অপ্টিমাইজযোগ্য দিকগুলি হলো:

- EMA পিরিয়ড প্যারামিটার সমন্বয় অপ্টিমাইজ করে নির্দেশককে বাজারের বৈশিষ্ট্যের সাথে আরও মানানসই করা।

- লাভ নিশ্চিত করার পাশাপাশি একক ট্রেডের ক্ষতির ঝুঁকি সর্বনিম্ন করতে স্টপ-লসের অবস্থান সমন্বয় করা।

- অস্থিরতার ভিত্তিতে গতিশীল পজিশন সাইজিং মডিউল যুক্ত করে কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করা।

- আরও বেশি দামের ধরণ উন্মোচন করতে এবং সিগন্যালের মান উন্নত করতে ডিপ লার্নিং প্রযুক্তি ব্যবহার করা।

সারসংক্ষেপ

ট্রিপল মুভিং এভারেজ সুইং কৌশল দামের ওঠানামার ধরণ গভীরভাবে বিশ্লেষণ করে এবং স্থিতিশীল ও দক্ষ, যা দীর্ঘমেয়াদি প্রয়োগ ও ধারাবাহিক অপ্টিমাইজেশনের উপযুক্ত। বিনিয়োগের জন্য যুক্তি ও ধৈর্য প্রয়োজন, ধাপে ধাপে ট্রেড করাই সাফল্যের চাবিকাঠি।

- 1