দ্বিমুখী গ্রিড K-লাইন ট্র্যাকিং ট্রেডিং কৌশল

ওভারভিউ

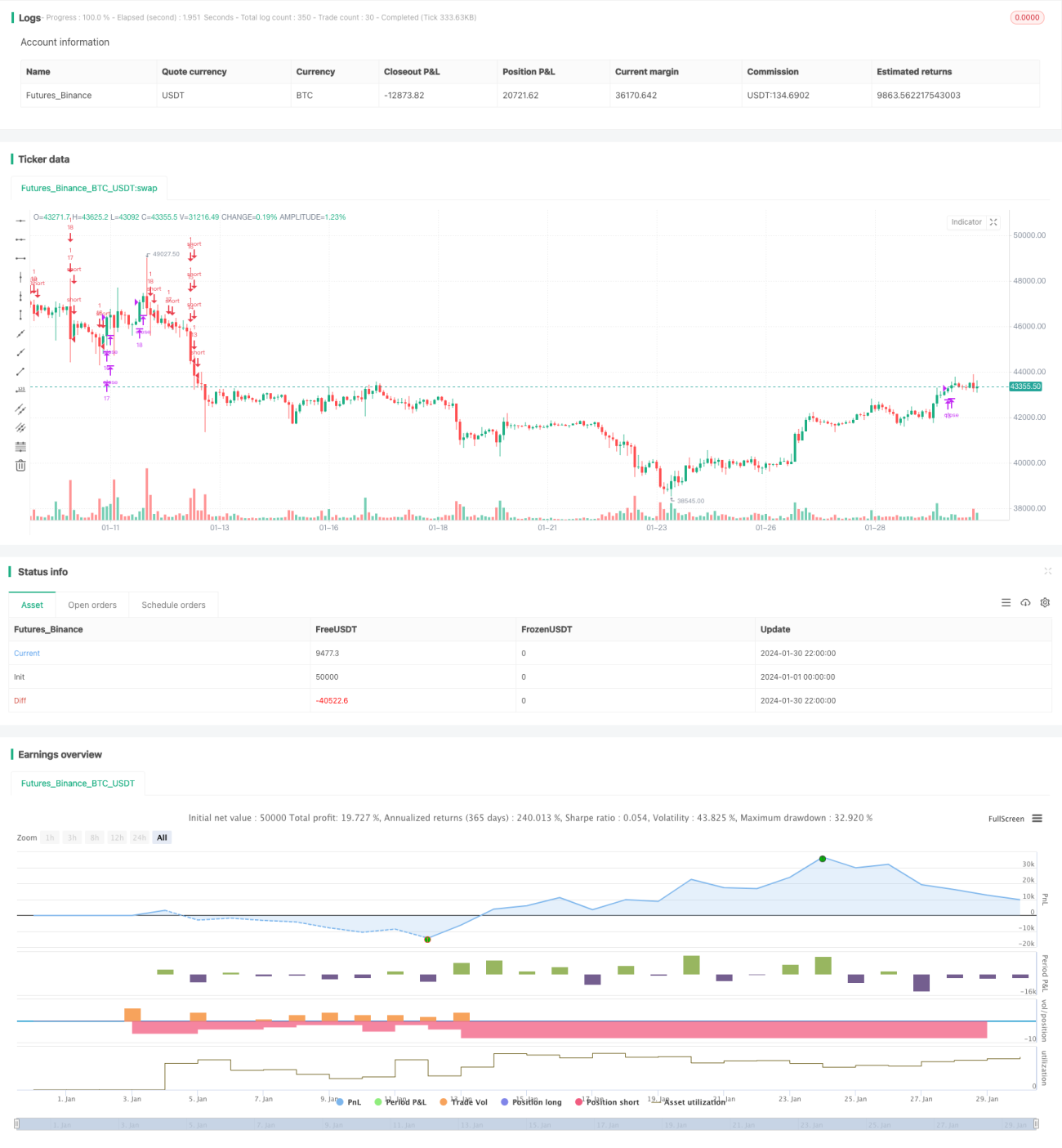

এই কৌশলটি K-লাইন রিয়েল-টাইম পরিবর্তনের ভিত্তিতে একটি দ্বি-দিকনির্দেশক ট্র্যাকিং গ্রিড ট্রেডিং কৌশল। এটি বুলিশ এবং বিয়ারিশ বাজার উভয় ক্ষেত্রেই স্থিতিশীল মুনাফা অর্জন করতে পারে।

কৌশলের নীতি

-

ব্যবহারকারীর সেট করা গ্রিড সংখ্যা অনুযায়ী, স্বয়ংক্রিয়ভাবে মূল্য গ্রিডের পরিসর এবং প্রতিটি গ্রিডের মূল্য গণনা করে।

-

যখন মূল্য গ্রিডের মূল্য ভেদ করে, তখন নির্দিষ্ট পরিমাণে লং পজিশন খোলে; যখন মূল্য গ্রিডের মূল্যের নিচে নামে, তখন লং পজিশন বন্ধ করে এবং শর্ট পজিশন খোলে।

-

এইভাবে, মূল্য যখন গ্রিডের পরিসরে ওঠানামা করে, তখন মূল্য পরিবর্তন ট্র্যাক করে মুনাফা অর্জন করা যায়।

সুবিধা বিশ্লেষণ

-

স্বয়ংক্রিয়ভাবে যুক্তিসঙ্গত গ্রিড পরিসর গণনা করে, কৃত্রিমভাবে সমর্থন ও প্রতিরোধ নির্ধারণের প্রয়োজন নেই।

-

দ্বি-দিকনির্দেশক ট্রেডিং, পরিবর্তনশীল বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে পারে।

-

নির্দিষ্ট পরিমাণে পজিশন খোলা, ঝুঁকি নিয়ন্ত্রণে সহায়ক।

-

কোডটি সহজবোধ্য ও সংক্ষিপ্ত, বোঝা এবং পরিবর্তন করা সহজ।

ঝুঁকি বিশ্লেষণ

-

বাজারের তীব্র ওঠানামা ক্ষতি বাড়িয়ে দিতে পারে।

-

ট্রেডিং ফি-এর জমানো চূড়ান্ত মুনাফাকেও প্রভাবিত করে।

-

গ্রিডের সংখ্যা যুক্তিসঙ্গতভাবে নির্ধারণ করতে হবে; অনেক বেশি গ্রিড থাকলে ট্রেডের সংখ্যা বাড়ে কিন্তু প্রতিটি লাভ সীমিত।

অপ্টিমাইজেশন দিকনির্দেশনা

-

স্টপ-লস কৌশল যোগ করা, ক্ষতি বাড়তে বাধা দেওয়া।

-

গ্রিড সংখ্যার গতিশীল সমন্বয় ফিচার যোগ করা।

-

লিভারেজ যোগ করার বিবেচনা, ট্রেডিং ভলিউম বাড়ানো।

সারসংক্ষেপ

এই কৌশলের সামগ্রিক ধারণা স্পষ্ট ও সরল, দ্বি-দিকনির্দেশক ট্র্যাকিং গ্রিড ট্রেডিংয়ের মাধ্যমে স্থিতিশীল আয় অর্জন করা যায়, তবে কিছু ট্রেডিং ঝুঁকিও রয়েছে। ক্রমাগত অপ্টিমাইজেশনের মাধ্যমে আরও ভাল ফলাফল আশা করা যায়।

- 1