দুই-মুভিং এভারেজ কোয়ান্টিটেটিভ ট্রেডিং কৌশল

সারসংক্ষেপ

এই কৌশলটি দ্রুত চলমান গড় এবং ধীর চলমান গড় গণনা করে এবং প্যারাবোলিক সূচকের সাথে মিলিয়ে ক্রয়/বিক্রয়ের সিদ্ধান্ত নেয়। এটি একটি ট্রেন্ড অনুসরণকারী (ট্রেন্ড ট্র্যাকিং) ধরনের কৌশল। যখন দ্রুত চলমান গড় ধীর চলমান গড়কে উপরে অতিক্রম করে, তখন লং (ক্রয়) পজিশন নেওয়া হয়; যখন দ্রুত চলমান গড় ধীর চলমান গড়কে নিচে অতিক্রম করে, তখন শর্ট (বিক্রয়) পজিশন নেওয়া হয়। একইসাথে প্যারাবোলিক সূচক ব্যবহার করে মিথ্যা ব্রেকআউট ফিল্টার করা হয়।

কৌশলের মূলনীতি

- দ্রুত চলমান গড় এবং ধীর চলমান গড় গণনা করা হয়। চলমান গড়ের প্যারামিটার কাস্টমাইজ করা যায়।

- দুটি চলমান গড় তুলনা করে বাজারের দিকনির্দেশ নির্ধারণ করা হয়। যখন দ্রুত চলমান গড় ধীর চলমান গড়কে উপরে অতিক্রম করে, তখন বাজারকে বুলিশ (ঊর্ধ্বমুখী) ধরা হয়; যখন দ্রুত চলমান গড় ধীর চলমান গড়কে নিচে অতিক্রম করে, তখন বাজারকে বিয়ারিশ (নিম্নমুখী) ধরা হয়।

- আরও নিশ্চিতকরণের জন্য ক্লোজিং প্রাইস এবং চলমান গড়ের সম্পর্ক ব্যবহার করা হয়। শুধুমাত্র যখন দ্রুত লাইন ধীর লাইনকে উপরে অতিক্রম করে এবং ক্লোজিং প্রাইস দ্রুত লাইনের উপরে থাকে, তখনই ক্রয় সংকেত তৈরি হয়; শুধুমাত্র যখন দ্রুত লাইন ধীর লাইনকে নিচে অতিক্রম করে এবং ক্লোজিং প্রাইস দ্রুত লাইনের নিচে থাকে, তখনই বিক্রয় সংকেত তৈরি হয়।

- প্যারাবোলিক সূচক ব্যবহার করে মিথ্যা ব্রেকআউট ফিল্টার করা হয়। শুধুমাত্র যখন দ্রুত লাইন ধীর লাইনকে উপরে অতিক্রম করে, ক্লোজিং প্রাইস দ্রুত লাইনের উপরে থাকে এবং শেয়ারের দাম প্যারাবোলিকের উপরে থাকে, তখনই চূড়ান্ত ক্রয় সংকেত তৈরি হয়; বিপরীত ক্ষেত্রেও একই নিয়ম প্রযোজ্য।

- সর্বোচ্চ সহনীয় ক্ষতির ভিত্তিতে স্টপ লস নির্ধারণ করা হয়। ATR সূচকের সাথে মিলিয়ে নির্দিষ্ট স্টপ লস মূল্য গণনা করা হয়।

কৌশলের সুবিধা

- চলমান গড় ব্যবহার করে বাজারের দিকনির্দেশ নির্ধারণ করা হয়, যা দিকহীন রেঞ্জবাউন্ড বাজারে অপ্রয়োজনীয় ট্রেডিং এড়াতে সাহায্য করে।

- দ্বৈত ফিল্টারিং শর্ত সাধারণ মিথ্যা ব্রেকআউট সমস্যা কার্যকরভাবে এড়াতে সহায়তা করে।

- স্টপ লস কৌশল ব্যবহার করে প্রতিটি ট্রেডের ক্ষতি নিয়ন্ত্রণ করা যায়।

কৌশলের ঝুঁকি

- সূচকভিত্তিক কৌশলগুলি সহজেই মিথ্যা সংকেত তৈরি করতে পারে।

- মুদ্রার ঝুঁকি বিবেচনায় নেওয়া হয়নি।

- সম্ভাব্য প্রাথমিক বিপরীত দিকের মুভমেন্ট মিস হতে পারে।

উপরোক্ত সমস্যাগুলি সমাধানের জন্য নিম্নলিখিত দিকগুলি থেকে অপ্টিমাইজেশন করা যেতে পারে:

- চলমান গড়ের প্যারামিটার অপ্টিমাইজ করে নির্দিষ্ট সম্পদের সাথে আরও উপযোগী করা।

- অন্যান্য সূচক বা মডেলের সাথে একত্রিত করে সংকেত ফিল্টার করা।

- রিয়েল-টাইম হেজিং বা স্বয়ংক্রিয়ভাবে ব্রোকার অ্যাকাউন্টের মুদ্রা রূপান্তরের ব্যবস্থা করা।

অপ্টিমাইজেশনের দিকনির্দেশনা

- চলমান গড়ের প্যারামিটার অপ্টিমাইজ করে ট্রেন্ড আরও ভালোভাবে ক্যাপচার করা।

- মডেল কম্বিনেশন বাড়িয়ে সংকেতের নির্ভুলতা উন্নত করা।

- একাধিক টাইমফ্রেমে যাচাই করে ফাঁদে পড়া এড়ানো।

- স্টপ লস কৌশল অপ্টিমাইজ করে কৌশলের স্থায়িত্ব বৃদ্ধি করা।

সারসংক্ষেপ

এই কৌশলটি একটি সাধারণ ডাবল মুভিং এভারেজ এবং সূচক কম্বিনেশন ট্রেন্ড ট্র্যাকিং কৌশল। দ্রুত ও ধীর দুটি চলমান গড়ের দিক তুলনা করে বাজারের ট্রেন্ড নির্ধারণ করা হয় এবং একাধিক ফিল্টারিং সূচক ব্যবহার করে মিথ্যা সংকেত এড়িয়ে ট্রেডিং সিগন্যাল তৈরি করা হয়। একইসাথে, প্রতিটি ট্রেডের ক্ষতি নিয়ন্ত্রণের জন্য কৌশলে স্টপ লস ফাংশন রয়েছে। সুবিধা হলো কৌশলের যুক্তি সহজ ও স্পষ্ট, বোঝা এবং বাস্তবায়ন করা সহজ, এবং প্রয়োজন অনুযায়ী নমনীয়ভাবে অপ্টিমাইজ করা যায়। অসুবিধা হলো এটি একটি মোটামুটি ট্রেন্ড নির্ধারণের টুল হিসেবে সংকেতের নির্ভুলতা উন্নত করার প্রয়োজন রয়েছে, যা মেশিন লার্নিংয়ের মতো উন্নত মডেল প্রবর্তনের মাধ্যমে অপ্টিমাইজ করা যেতে পারে।

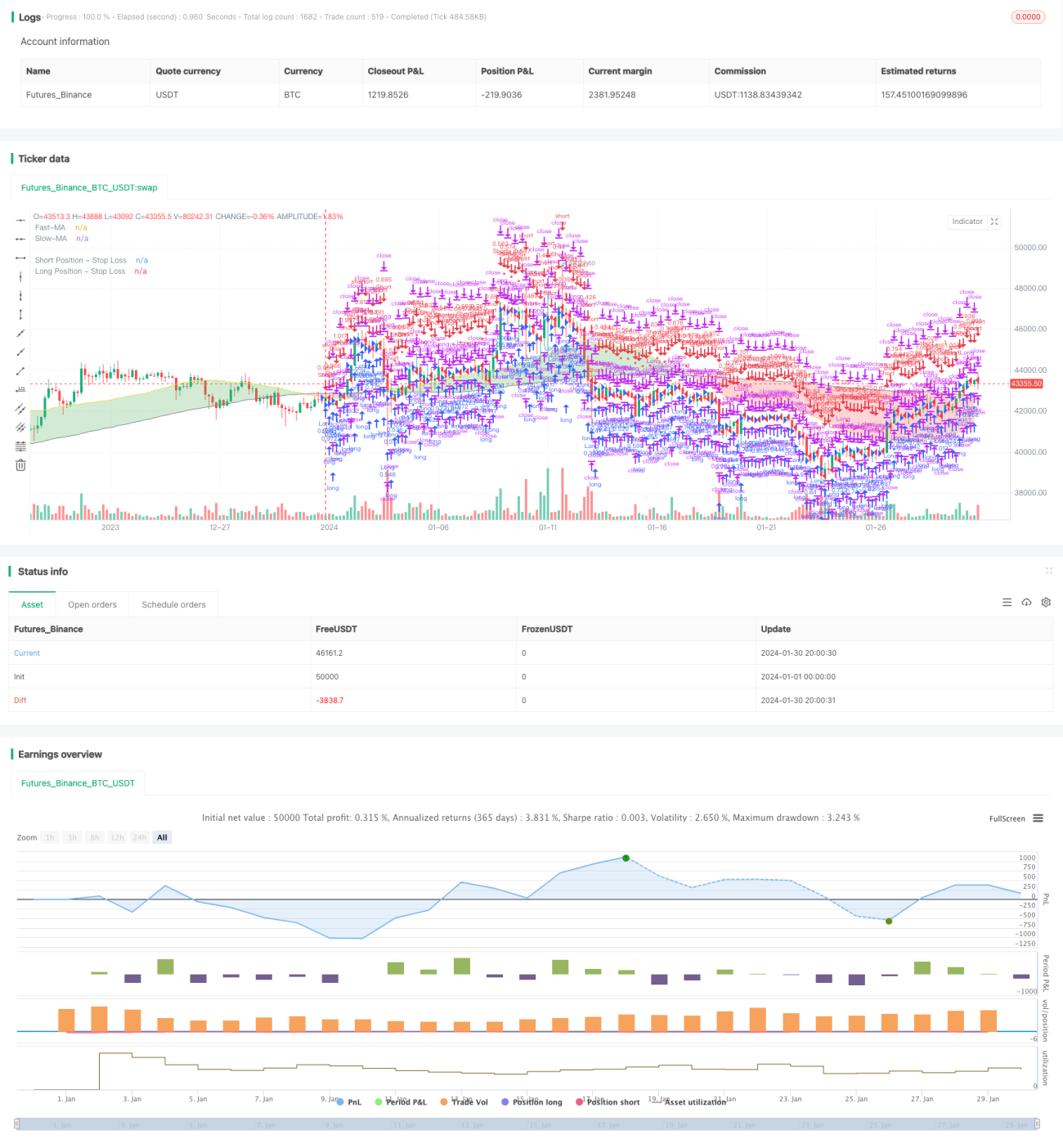

- 1