অলস ভালুক গতিবেগ স্কুইজ কৌশল

সারসংক্ষেপ

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজি হলো একটি কোয়ান্টিটেটিভ ট্রেডিং স্ট্র্যাটেজি যা বোলিঞ্জার ব্যান্ড, কেল্টনার চ্যানেল এবং মোমেন্টাম ইন্ডিকেটরকে একত্রিত করে। এটি বোলিঞ্জার ব্যান্ড এবং কেল্টনার চ্যানেল ব্যবহার করে বর্তমান বাজার স্কুইজ অবস্থায় আছে কিনা তা নির্ধারণ করে, তারপর মোমেন্টাম ইন্ডিকেটরের সাথে মিলিয়ে ট্রেডিং সিগন্যাল তৈরি করে।

এই স্ট্র্যাটেজির প্রধান সুবিধা হলো এটি স্বয়ংক্রিয়ভাবে ট্রেন্ডিং মার্কেটের সূচনা শনাক্ত করতে পারে এবং মোমেন্টাম ইন্ডিকেটরের মাধ্যমে প্রবেশের সময় নির্ধারণ করতে পারে। তবে এর কিছু ঝুঁকিও রয়েছে এবং বিভিন্ন প্রোডাক্টের জন্য প্যারামিটার অপ্টিমাইজেশন প্রয়োজন।

স্ট্র্যাটেজির মূলনীতি

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজি নিম্নলিখিত তিনটি ইন্ডিকেটরের উপর ভিত্তি করে কাজ করে:

- বোলিঞ্জার ব্যান্ড (Bollinger Bands): মিডল ব্যান্ড, আপার ব্যান্ড এবং লোয়ার ব্যান্ড নিয়ে গঠিত

- কেল্টনার চ্যানেল (Keltner Channels): মিডল ব্যান্ড, আপার ব্যান্ড এবং লোয়ার ব্যান্ড নিয়ে গঠিত

- মোমেন্টাম ইন্ডিকেটর (Momentum Indicator): বর্তমান মূল্য এবং n দিন আগের মূল্যের মধ্যে পার্থক্য

যখন বোলিঞ্জার ব্যান্ডের আপার ব্যান্ড কেল্টনার চ্যানেলের আপার ব্যান্ডের নিচে থাকে, এবং বোলিঞ্জার ব্যান্ডের লোয়ার ব্যান্ড কেল্টনার চ্যানেলের লোয়ার ব্যান্ডের উপরে থাকে, তখন আমরা ধরি যে বাজার স্কুইজ অবস্থায় আছে। এটি সাধারণত ইঙ্গিত দেয় যে বর্তমান ট্রেন্ডিং মুভমেন্ট শুরু হতে চলেছে।

প্রবেশের সময় নির্ধারণের জন্য আমরা মোমেন্টাম ইন্ডিকেটর ব্যবহার করে মূল্য পরিবর্তনের গতি নির্ণয় করি। যখন মোমেন্টাম তার গড় মান উপরের দিকে ভেঙে যায়, তখন বাই সিগন্যাল তৈরি হয়; যখন মোমেন্টাম তার গড় মান নিচের দিকে ভেঙে যায়, তখন সেল সিগন্যাল তৈরি হয়।

স্ট্র্যাটেজির সুবিধা বিশ্লেষণ

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজির প্রধান সুবিধাগুলো হলো:

- স্বয়ংক্রিয়ভাবে ট্রেন্ড শুরুর সময় চিহ্নিত করতে পারে এবং দ্রুত প্রবেশ করতে পারে

- একাধিক ইন্ডিকেটর ব্যবহার করে মিথ্যা সংকেত এড়ায়

- ট্রেন্ড এবং রিভারসাল উভয় ধরনের ট্রেডিং পদ্ধতিকে সামঞ্জস্য রাখে

- কাস্টমাইজযোগ্য প্যারামিটার, বিভিন্ন প্রোডাক্টের জন্য অপ্টিমাইজ করা যায়

ঝুঁকি বিশ্লেষণ

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজির কিছু ঝুঁকিও রয়েছে:

- বোলিঞ্জার ব্যান্ড এবং কেল্টনার চ্যানেলের মিথ্যা সংকেত দেওয়ার সম্ভাবনা বেশি

- মোমেন্টাম ইন্ডিকেটর অস্থির হতে পারে এবং সেরা প্রবেশ পয়েন্ট মিস করতে পারে

- প্যারামিটার অপ্টিমাইজেশন প্রয়োজন, অন্যথায় ফলাফল দুর্বল হয়

- ফলাফল ট্রেডিং প্রোডাক্টের সাথে উচ্চ সম্পর্কযুক্ত

ঝুঁকি কমানোর জন্য, বোলিঞ্জার ব্যান্ড এবং কেল্টনার চ্যানেলের দৈর্ঘ্য প্যারামিটার অপ্টিমাইজ করার, স্টপ লস পয়েন্ট সমন্বয় করার, তরলতা ভালো এমন ট্রেডিং প্রোডাক্ট বেছে নেওয়ার এবং অন্যান্য ইন্ডিকেটরের সাথে যাচাই করার পরামর্শ দেওয়া হয়।

স্ট্র্যাটেজি অপ্টিমাইজেশনের দিকনির্দেশনা

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজির কার্যকারিতা আরও বাড়ানোর জন্য প্রধান অপ্টিমাইজেশনের দিকগুলো হলো:

- বিভিন্ন প্রোডাক্ট এবং টাইমফ্রেমের জন্য প্যারামিটার কম্বিনেশন পরীক্ষা করা

- বোলিঞ্জার ব্যান্ড এবং কেল্টনার চ্যানেলের দৈর্ঘ্য অপ্টিমাইজ করা

- মোমেন্টাম ইন্ডিকেটরের দৈর্ঘ্য অপ্টিমাইজ করা

- লং এবং শর্ট পজিশনের জন্য আলাদা স্টপ লস ও টেক প্রফিট কৌশল তৈরি করা

- সিগন্যাল যাচাইয়ের জন্য অন্যান্য ইন্ডিকেটর যুক্ত করা

বহুমুখী পরীক্ষা ও অপ্টিমাইজেশনের মাধ্যমে এই স্ট্র্যাটেজির জয় রেট এবং লাভজনকতা ব্যাপকভাবে উন্নত করা সম্ভব।

উপসংহার

লেজি বিয়ার মোমেন্টাম স্কুইজ স্ট্র্যাটেজি একাধিক ইন্ডিকেটরকে একীভূত করে শক্তিশালী বিচারক্ষমতা প্রদান করে এবং ট্রেন্ড শুরুর সময় কার্যকরভাবে চিহ্নিত করতে পারে। তবে এর কিছু ঝুঁকিও রয়েছে এবং বিভিন্ন ট্রেডিং প্রোডাক্টের জন্য প্যারামিটার অপ্টিমাইজেশন প্রয়োজন। ক্রমাগত পরীক্ষা ও অপ্টিমাইজেশনের মাধ্যমে এই স্ট্র্যাটেজি একটি দক্ষ অ্যালগরিদমিক ট্রেডিং সিস্টেমে পরিণত হতে পারে।

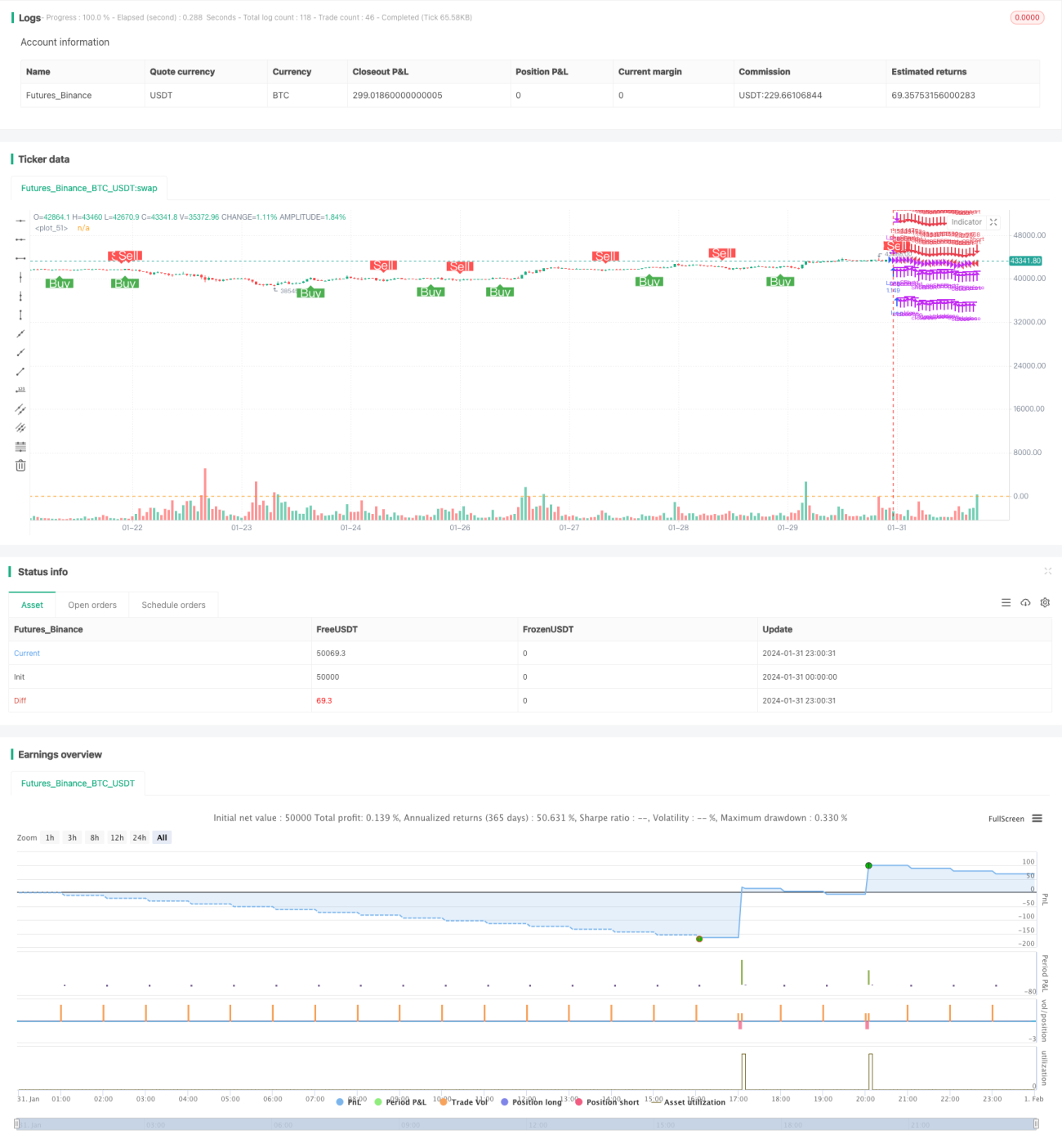

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1