বলিঞ্জার ব্যান্ড ও VWAP ভিত্তিক লং ব্রেকআউট কৌশল

সারসংক্ষেপ

এই কৌশলটি VWAP ট্র্যাক করার জন্য বলিঞ্জার ব্যান্ড ব্যবহার করে। যখন VWAP বলিঞ্জার ব্যান্ডের মাঝের রেখা ভেদ করে উপরে উঠে, তখন তা বুলিশ ব্রেকআউট হিসেবে চিহ্নিত করা হয় এবং লং পজিশন নেওয়া হয়। অন্যদিকে, যখন VWAP বলিঞ্জার ব্যান্ডের নিচের রেখা ভেদ করে নিচে নামে, তখন তা বিয়ারিশ নিশ্চিতকরণ হিসেবে বিবেচিত হয় এবং পজিশন বন্ধ করা হয়। একই সঙ্গে, কৌশলটি প্রধান সমর্থন স্তর পিভট পয়েন্টকেও এন্ট্রি সিগন্যালের সহায়ক শর্ত হিসেবে ব্যবহার করে, যা মিথ্যা ব্রেকআউট ফিল্টার করতে সাহায্য করে।

কৌশলের নীতি

- VWAP মান গণনা করা।

- VWAP-এর বলিঞ্জার ব্যান্ড গণনা করা, যার মধ্যে উপরের রেখা, মাঝের রেখা এবং নিচের রেখা অন্তর্ভুক্ত।

- নির্ণয় করা যে VWAP বলিঞ্জার ব্যান্ডের মাঝের রেখা ভেদ করে উপরে উঠেছে কিনা। যদি তা হয় এবং দাম প্রধান সমর্থন স্তর পিভট পয়েন্টের উপরে থাকে, তাহলে লং পজিশন নেওয়া হয়।

- স্টপ লস নির্ধারণ করা হয় ৫%।

- যদি VWAP বলিঞ্জার ব্যান্ডের নিচের রেখা ভেদ করে নিচে নামে, তাহলে বিয়ারিশ নিশ্চিত বলে গণ্য করে পজিশন বন্ধ করা হয়; যদি স্টপ লস ট্রিগার হয়, তাহলেও পজিশন বন্ধ করা হয়।

সুবিধা বিশ্লেষণ

- VWAP-এর শক্তিশালী ট্রেন্ড অনুসরণের ক্ষমতা আছে; বলিঞ্জার ব্যান্ডের সাথে মিলিয়ে এটি ট্রেন্ডের শুরু সঠিকভাবে চিহ্নিত করতে পারে।

- পিভট পয়েন্টকে সহায়ক শর্ত হিসেবে যুক্ত করায় অনেক মিথ্যা ব্রেকআউট ফিল্টার হয়, অপ্রয়োজনীয় লোকসান এড়ানো যায়।

- আংশিক পজিশন বন্ধ করার কৌশল ব্যবহার করায় কিছু মুনাফা লক করা যায় এবং ঝুঁকি নিয়ন্ত্রণ করা যায়।

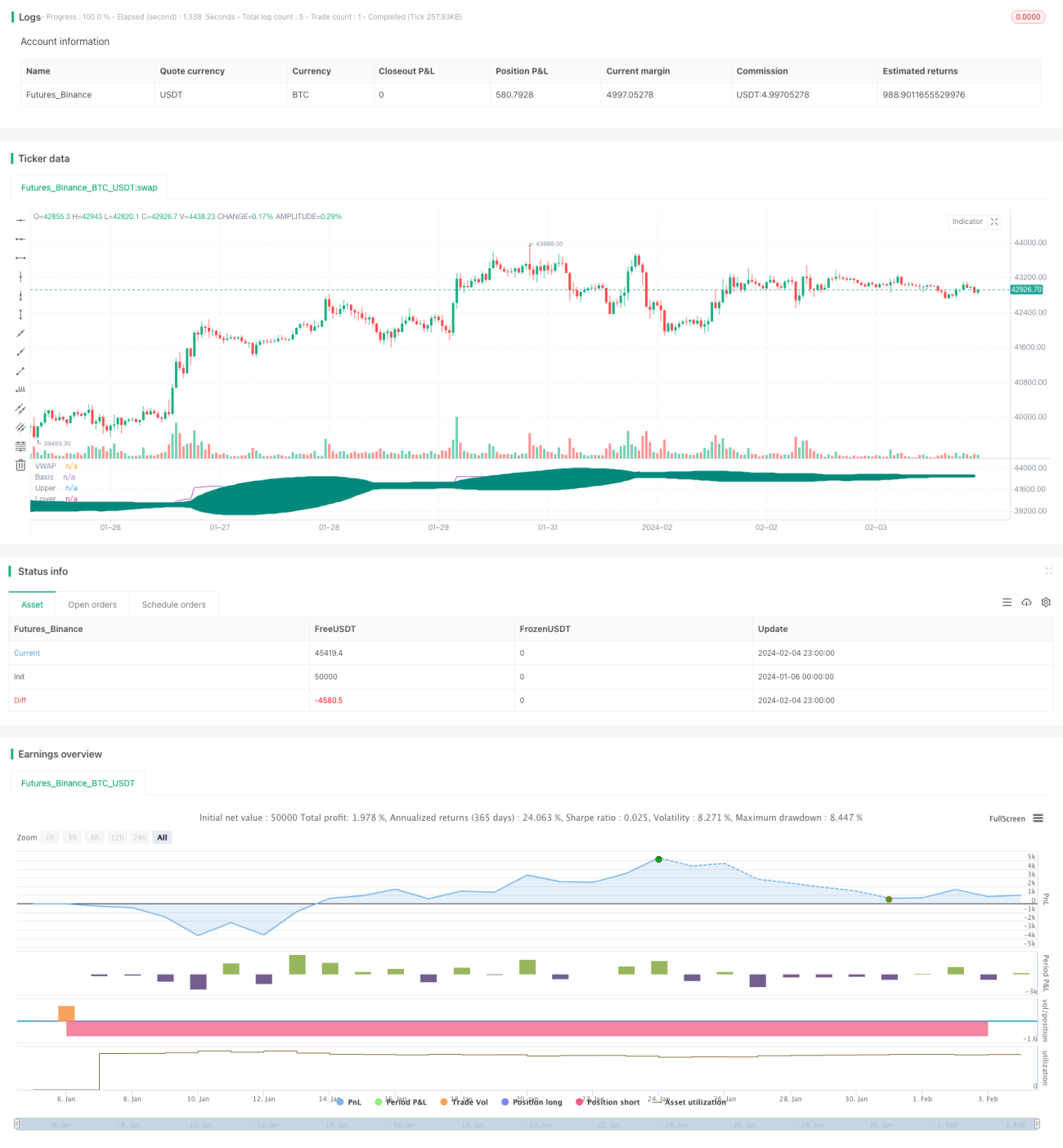

- ব্যাকটেস্ট ফলাফলে দেখা যায়, এই কৌশলটি বুল মার্কেটে চমৎকার কর্মক্ষমতা দেখায় এবং উচ্চ স্থিতিশীলতা বজায় রাখে।

ঝুঁকি বিশ্লেষণ

- সাইডওয়েজ/রেঞ্জ মার্কেটে মিথ্যা ব্রেকআউটের কারণে লোকসান হওয়ার সম্ভাবনা থাকে।

- পিভট পয়েন্ট সম্পূর্ণভাবে মিথ্যা ব্রেকআউট এড়াতে পারে না; আরও ইন্ডিকেটর দিয়ে সিগন্যাল ফিল্টার করা প্রয়োজন।

- আংশিক পজিশন বন্ধ করায় অপারেশন ফ্রিকোয়েন্সি বাড়ে, ফলে ট্রেডিং খরচও বাড়ে।

- বিয়ার মার্কেটে এই কৌশল তেমন কার্যকর নয়; ঝুঁকি নিয়ন্ত্রণে রাখা জরুরি।

অপ্টিমাইজেশনের দিকনির্দেশনা

- MACD, KDJ-এর মতো অন্যান্য ইন্ডিকেটর যুক্ত করে এন্ট্রি ও এক্সিট সিগন্যাল আরও ফিল্টার করা যেতে পারে।

- বলিঞ্জার ব্যান্ডের দৈর্ঘ্য এবং স্ট্যান্ডার্ড ডেভিয়েশন অপ্টিমাইজ করে সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করা যেতে পারে।

- মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে বলিঞ্জার ব্যান্ডের প্যারামিটার ডায়নামিক অপ্টিমাইজ করা যেতে পারে।

- বিভিন্ন স্টপ লস লেভেল পরীক্ষা করে সর্বোত্তম স্টপ লস পয়েন্ট নির্ধারণ করা যেতে পারে।

- অ্যাডাপটিভ এক্সিট মেকানিজম যুক্ত করা যেতে পারে, যা বাজারের ওঠানামার মাত্রা অনুযায়ী লক্ষ্য মুনাফা সমন্বয় করবে।

সারসংক্ষেপ

সামগ্রিকভাবে এই কৌশলটি একটি স্থিতিশীল ব্রেকআউট সিস্টেম। এর প্রমিত অপারেশন পদ্ধতি এবং প্যারামিটার অপ্টিমাইজেশনের যথেষ্ট জায়গা থাকায় এটি কোয়ান্টিটেটিভ ট্রেডিংয়ের জন্য উপযোগী। তবে ঝুঁকি নিয়ন্ত্রণ এবং অস্বাভাবিক বাজার পরিস্থিতির কারণে লোকসান এড়ানোর দিকেও নজর রাখা প্রয়োজন। সার্বিকভাবে, এটি আরও গভীরভাবে গবেষণা ও ক্রমাগত অপ্টিমাইজেশনের যোগ্য একটি ব্রেকআউট-ভিত্তিক কৌশল।

- 1