মুভিং এভারেজ ক্রসওভার রিভার্সাল স্ট্র্যাটেজি

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি সরল চলমান গড়ের উপর ভিত্তি করে ক্রস-গড় রিভার্সাল কৌশল। এটি দৈর্ঘ্য ১ এবং দৈর্ঘ্য ৫ এর সরল চলমান গড় ব্যবহার করে। যখন স্বল্পমেয়াদী চলমান গড় দীর্ঘমেয়াদী চলমান গড়কে নিচ থেকে উপরে অতিক্রম করে, তখন লং পজিশন নেওয়া হয়; যখন উপর থেকে নিচে অতিক্রম করে, তখন শর্ট পজিশন নেওয়া হয়। এটি একটি সাধারণ ট্রেন্ড ফলোয়িং কৌশল।

কৌশলের নীতি

এই কৌশলটি ক্লোজ প্রাইসের ১ দিনের সরল চলমান গড় sma1 এবং ৫ দিনের সরল চলমান গড় sma5 গণনা করে। যখন sma1 sma5 কে নিচ থেকে উপরে অতিক্রম করে, তখন লং এ প্রবেশ করা হয়; যখন sma1 sma5 কে উপর থেকে নিচে অতিক্রম করে, তখন শর্ট এ প্রবেশ করা হয়। লং নেওয়ার পর স্টপ লস নির্ধারণ করা হয় প্রবেশ মূল্যের ৫ ডলার নিচে, এবং টেক প্রফিট নির্ধারণ করা হয় প্রবেশ মূল্যের ১৫০ ডলার উপরে। শর্ট নেওয়ার পর স্টপ লস নির্ধারণ করা হয় প্রবেশ মূল্যের ৫ ডলার উপরে, এবং টেক প্রফিট নির্ধারণ করা হয় প্রবেশ মূল্যের ১৫০ ডলার নিচে।

সুবিধা বিশ্লেষণ

- দ্বৈত চলমান গড় ব্যবহার করে বাজারের ট্রেন্ডের দিক নির্ণয় করা হয়, যা স্টপ লস হওয়ার পরপরই বিপরীত দিকে প্রবেশ এড়াতে সাহায্য করে।

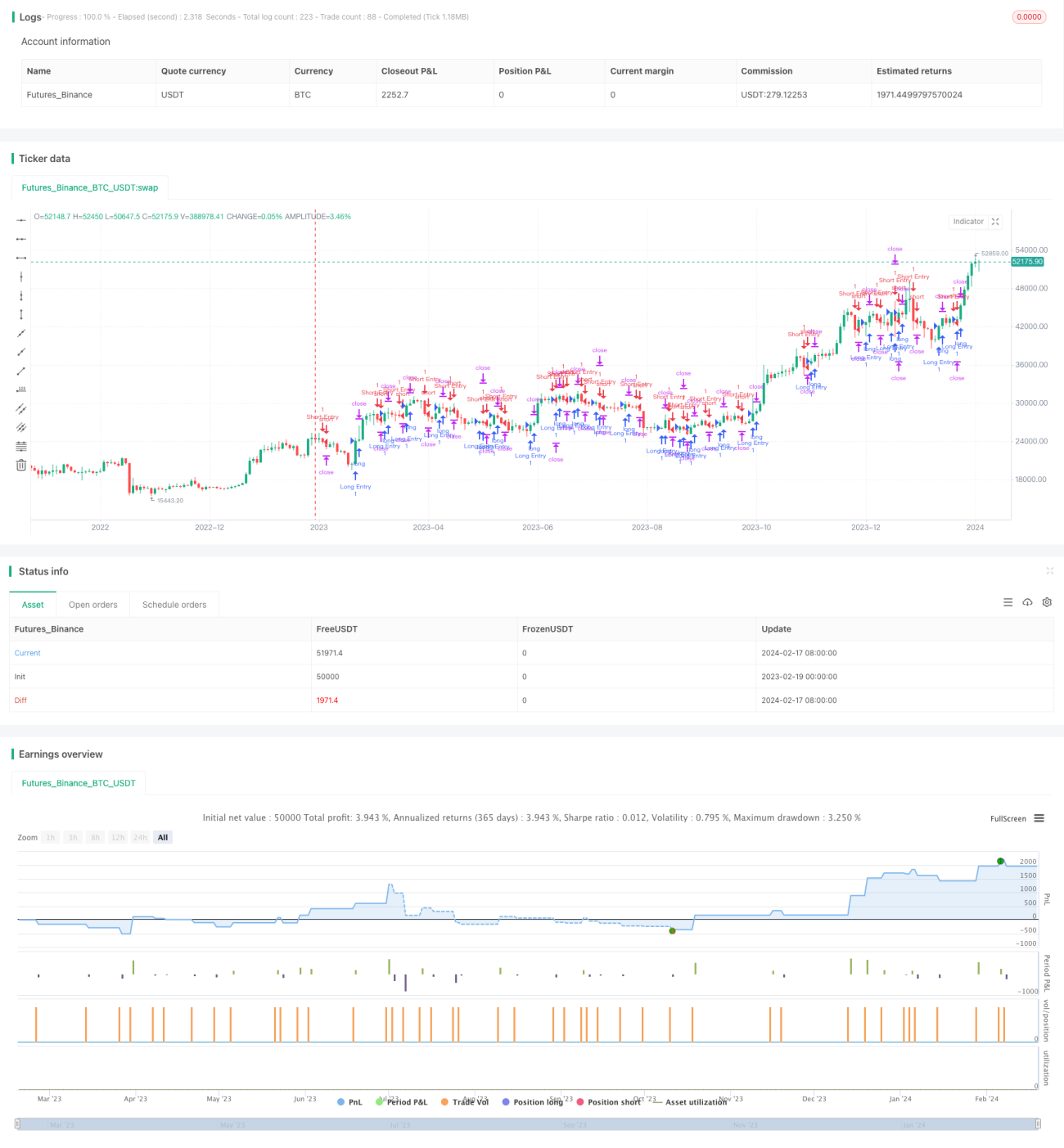

- চলমান গড়ের প্যারামিটারগুলি সহজ ও যুক্তিসঙ্গত, এবং ব্যাকটেস্টের ফলাফল ভালো।

- স্টপ লসের পরিমাণ ছোট, যা কিছুটা দামের ওঠানামা সহ্য করতে পারে।

- টেক প্রফিটের পরিমাণ বড়, যা পর্যাপ্ত মুনাফা অর্জন করতে পারে।

ঝুঁকি বিশ্লেষণ

- দ্বৈত চলমান গড় কৌশলটি সহজেই ফাঁদে পড়ে, দামের ওঠানামার সময় স্টপ লস হওয়ার সম্ভাবনা বেশি।

- ট্রেন্ডিং বাজার কার্যকরভাবে অনুসরণ করতে পারে না, দীর্ঘমেয়াদী মুনাফা অর্জনের ক্ষমতা সীমিত।

- প্যারামিটার অপ্টিমাইজেশনের সুযোগ সীমিত, এবং সহজেই ওভার-অপ্টিমাইজেশনের শিকার হতে পারে।

- নির্দিষ্ট ট্রেডিং যন্ত্রের জন্য প্যারামিটার সমন্বয় প্রয়োজন, বিভিন্ন যন্ত্রের জন্য আলাদা প্যারামিটার প্রয়োজন।

অপ্টিমাইজেশনের দিকনির্দেশনা:

- ভুল সংকেত এড়াতে অন্যান্য সূচক যুক্ত করা।

- স্টপ লস এবং টেক প্রফিটের পরিমাণ গতিশীলভাবে সমন্বয় করা।

- চলমান গড়ের প্যারামিটার অপ্টিমাইজ করা।

- অস্থিরতা সূচকের সাথে যুক্ত করে পজিশনের আকার নিয়ন্ত্রণ করা।

সারসংক্ষেপ

এই কৌশলটি একটি সরল দ্বৈত চলমান গড় কৌশল, যা সহজে বাস্তবায়নযোগ্য এবং কৌশল ধারণাগুলি দ্রুত পরীক্ষা করতে সাহায্য করে। তবে এর ধারণক্ষমতা এবং মুনাফার সম্ভাবনা সীমিত, তাই বিভিন্ন বাজার পরিবেশের সাথে খাপ খাওয়ানোর জন্য প্যারামিটার এবং ফিল্টার শর্তগুলি অপ্টিমাইজ করা প্রয়োজন। নতুনদের জন্য প্রথম কোয়ান্ট কৌশল হিসেবে, এতে মৌলিক উপাদান রয়েছে এবং এটি একটি সহজ কাঠামো হিসেবে পুনরাবৃত্তিমূলক উন্নতির জন্য ব্যবহার করা যেতে পারে।

- 1