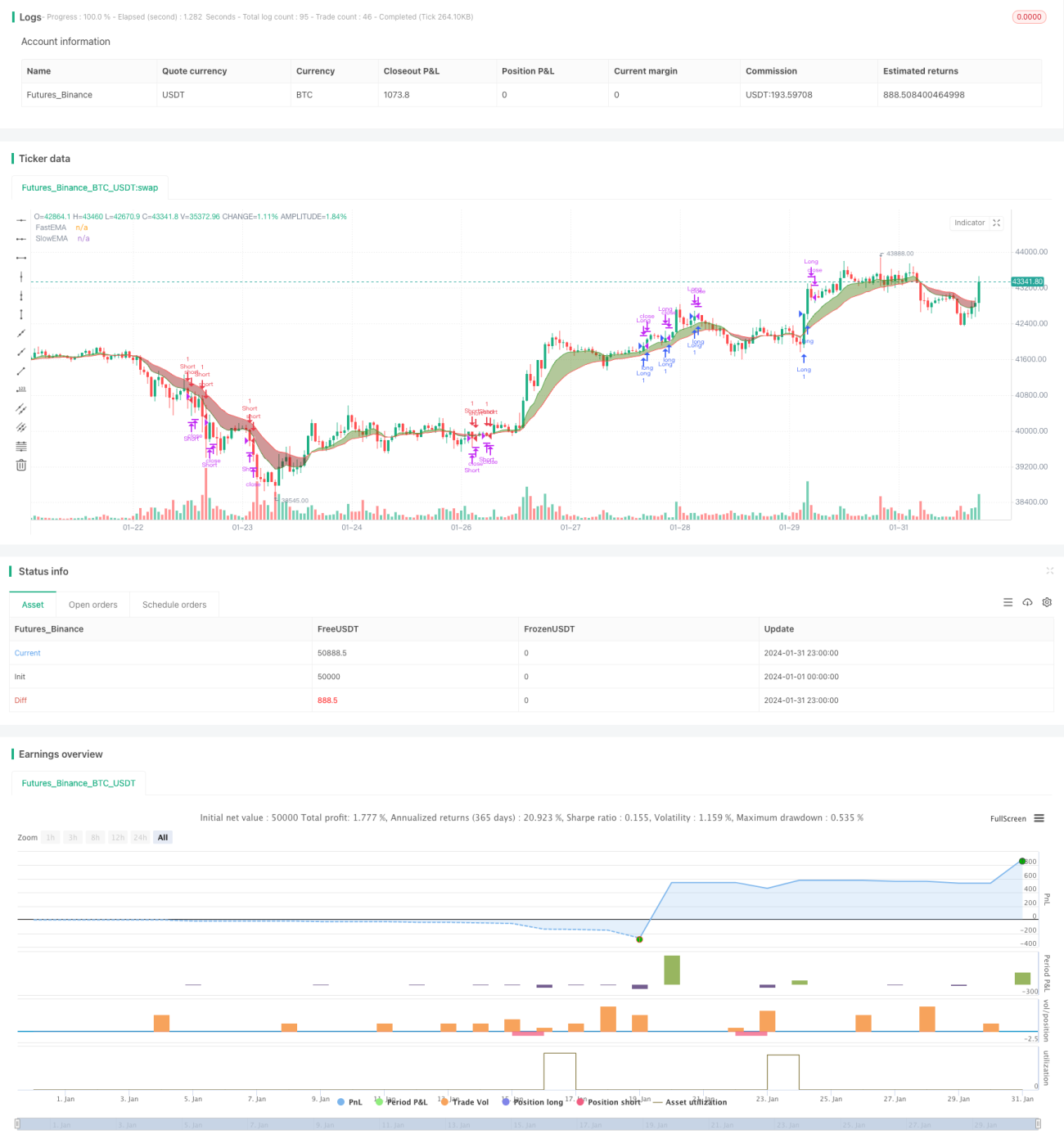

দ্বৈত পরিমাণগত বাণিজ্য ব্যবস্থার ভিত্তিতে

এই কৌশলটি একটি সংমিশ্রণ ট্রেডিং সিস্টেম যা CCI সূচক, RSI সূচক এবং দুটি মুভিং এভারেজের সমন্বয়ে গঠিত। এই সিস্টেমটি সাধারণ ট্রেন্ড ধরা এবং একই সাথে RSI সূচকের ক্রসওভারকে এন্ট্রি টাইমিংয়ের জন্য নিশ্চিতকরণ হিসেবে ব্যবহার করে কিছু নয়েজ ফিল্টার করতে পারে।

কৌশলের নীতি

এই কৌশলটি মূলত CCI সূচকের ভিত্তিতে ট্রেন্ডের দিক নির্ণয় করে। CCI সূচকের মান ১০০ এর উপরে থাকলে বুলিশ মার্কেট এবং -১০০ এর নিচে থাকলে বিয়ারিশ মার্কেট হিসেবে ধরা হয়। সিস্টেমটি দুটি মুভিং এভারেজের ক্রসওভার ব্যবহার করে ট্রেন্ডের দিক নিশ্চিত করতে সহায়তা করে। যখন দ্রুত মুভিং এভারেজ ধীর মুভিং এভারেজকে উপরে ক্রস করে, তখন এটি ক্রয় সংকেত, এবং বিপরীত ক্ষেত্রে বিক্রয় সংকেত।

ট্রেন্ডের দিক নির্ধারণের পর, সিস্টেমটি দুটি ভিন্ন প্যারামিটার দৈর্ঘ্যের RSI সূচকের ক্রসওভারকে এন্ট্রি নিশ্চিতকরণ হিসেবে ব্যবহার করে। উদাহরণস্বরূপ, বুলিশ মার্কেটে, যদি স্বল্প-মেয়াদী RSI সূচক দীর্ঘ-মেয়াদী RSI সূচককে উপরে ক্রস করে, তবে এটি চূড়ান্ত ক্রয় সংকেত। এই নকশাটি মূলত নয়েজ ফিল্টার করার জন্য, যাতে ট্রেন্ডের মধ্যে স্বল্পমেয়াদী সংশোধন ভুল ট্রেডের কারণ না হয়।

এই কৌশলটি শুধুমাত্র নির্ধারিত ট্রেডিং সেশনে পজিশন খোলে এবং বাজার বন্ধের ১৫ মিনিট আগে সমস্ত পজিশন সক্রিয়ভাবে ক্লোজ করে, রাতারাতি ঝুঁকি এড়াতে। পজিশন খোলার পরে মোবাইল স্টপ-লস ব্যবহার করে লাভ লক করা হয়।

সুবিধা বিশ্লেষণ

- ট্রেন্ড নির্ধারণ এবং সূচক ক্রসওভারের সমন্বয় কার্যকরভাবে ট্রেন্ড শনাক্ত করতে পারে এবং নয়েজ ফিল্টার করে, এন্ট্রি নির্ভুল করে।

- মোবাইল স্টপ-লস ব্যবহার করে সক্রিয়ভাবে ঝুঁকি নিয়ন্ত্রণ করে, স্টপ-লসের শিকার হওয়ার পরিস্থিতি এড়ায়।

- শুধুমাত্র নির্ধারিত ট্রেডিং সেশনে পজিশন খোলে, রাতারাতি গ্যাপ রিস্ক এড়ায়।

- RSI সূচকের প্যারামিটার সমন্বয়যোগ্য, যা বিভিন্ন বাজার পরিবেশের সাথে নমনীয়ভাবে মানিয়ে নিতে পারে।

ঝুঁকি বিশ্লেষণ

- CCI সূচক অস্বাভাবিক অস্থির বাজারে খারাপ পারফর্ম করে।

- ডুয়াল RSI ক্রসওভার শর্ত অনেক সীমাবদ্ধ, কিছু সুযোগ হারাতে পারে।

- মোবাইল স্টপ-লস অত্যধিক সাবজেক্টিভ হতে পারে; প্যারামিটার অপ্টিমাইজেশন প্রয়োজন।

- নির্ধারিত ট্রেডিং সেশন রাতারাতি গুরুত্বপূর্ণ খবরের কারণে গ্যাপ মিস করতে পারে।

অপ্টিমাইজেশন পরামর্শ

- বিভিন্ন প্যারামিটারের CCI সূচক পরীক্ষা করে সেরা প্যারামিটার সমন্বয় খুঁজে বের করা যেতে পারে।

- RSI ক্রসওভার শর্ত বাতিল করে সরাসরি CCI সূচকের ভিত্তিতে এন্ট্রি করা যায় কিনা তা পরীক্ষা করা যেতে পারে।

- মোবাইল স্টপ-লস প্যারামিটার ব্যাকটেস্ট অপ্টিমাইজ করে সেরা প্যারামিটার খুঁজে বের করা যেতে পারে।

- ফোর্সড লিকুইডেশন লজিক বাতিল করে পজিশন হোল্ডিং পিরিয়ডে শুধু মোবাইল স্টপ-লস ট্র্যাকিং করে লাভ সর্বাধিক করা যেতে পারে।

সারসংক্ষেপ

এই কৌশলটি ট্রেন্ড নির্ধারণ এবং সূচক ক্রসওভার নিশ্চিতকরণকে সমন্বয় করে, ঝুঁকি নিয়ন্ত্রণের পাশাপাশি ট্রেডিং সিগন্যালের কার্যকারিতাও নিশ্চিত করে। প্যারামিটার অপ্টিমাইজেশন এবং লজিক সংশোধনের মাধ্যমে, এই কৌশলটি লাভের সুযোগ আরও বাড়াতে পারে এবং মিস হওয়া সুযোগ কমাতে পারে। এটি একটি অত্যন্ত সম্ভাবনাময় ট্রেডিং আইডিয়া।

- 1