কম্প্রেশন ইন্ডিকেটর ভিত্তিক মাল্টি-টাইমফ্রেম ট্রেডিং স্ট্র্যাটেজি

সারসংক্ষেপ

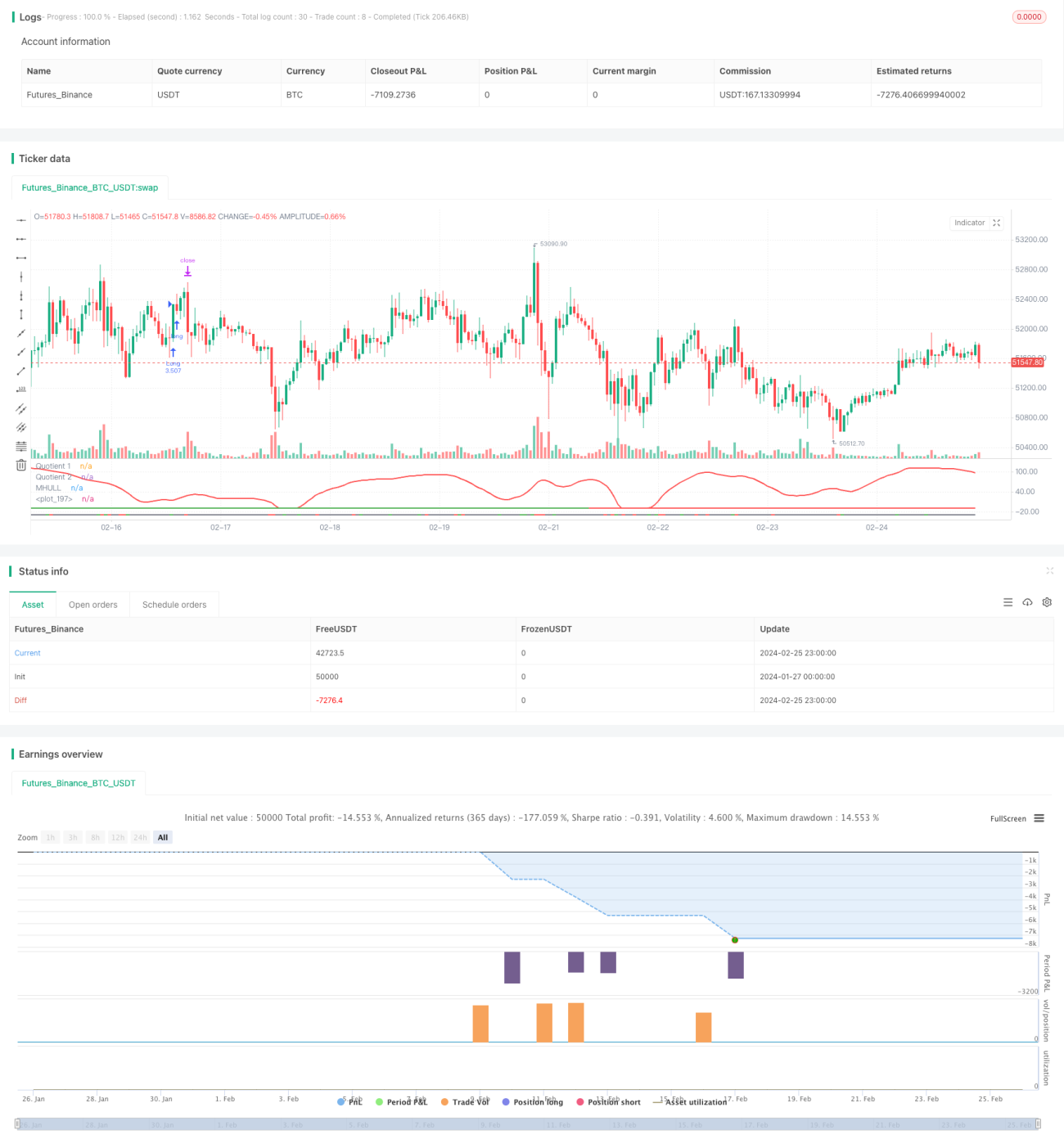

এই কৌশলটি বুম হান্টার, হাল স্যুট এবং ভোলাটিলিটি অসিলেটর – এই তিনটি সূচককে একত্রিত করে বহু-সময়সীমার মধ্যে ট্রেন্ড ট্র্যাকিং এবং ব্রেকআউট ট্রেডিংয়ের জন্য একটি পরিমাণগত কৌশল বাস্তবায়ন করে। এই কৌশলটি বিটকয়েনের মতো উচ্চ অস্থিরতা এবং আকস্মিক মূল্য আন্দোলনযুক্ত ডিজিটাল সম্পদের জন্য উপযুক্ত।

নীতি

কৌশলটির মূল যুক্তি নিম্নলিখিত তিনটি সূচকের উপর ভিত্তি করে তৈরি:

-

বুম হান্টার: একটি সূচক যা ইন্ডিকেটর কম্প্রেশন প্রযুক্তি ব্যবহার করে তৈরি একটি অসিলেটর। এটি দুটি সূচকের (কোশেন্ট১ এবং কোশেন্ট২) ক্রসওভারের মাধ্যমে ক্রয় ও বিক্রয়ের সংকেত নির্ধারণ করে।

-

হাল স্যুট: একগুচ্ছ মসৃণ মুভিং এভারেজ সূচক, যা মিডল ব্যান্ড এবং আপার/লোয়ার ব্যান্ডের সম্পর্কের মাধ্যমে ট্রেন্ডের দিক নির্ধারণ করে।

-

ভোলাটিলিটি অসিলেটর: একটি অসিলেটর সূচক যা মূল্যের অস্থিরতা সম্পর্কিত তথ্য পরিমাপ করে।

এই কৌশলের এন্ট্রি লজিক হলো: বুম হান্টারের দুটি কোশেন্ট সূচক যখন উপরে বা নিচে ক্রস করে, তখন একই সময়ে মূল্য হাল মিডল ব্যান্ড ভেদ করে এবং আপার বা লোয়ার ব্যান্ডের সাথে ডাইভারজেন্স তৈরি করে, আর ভোলাটিলিটি অসিলেটর ওভারবট/ওভারসোল্ড এলাকায় থাকে। এর মাধ্যমে কিছু মিথ্যা ব্রেকআউট সংকেত ফিল্টার করা যায় এবং এন্ট্রির নির্ভুলতা বাড়ে।

স্টপ লস নির্ধারণ করা হয় একটি নির্দিষ্ট সময়কালের (ডিফল্ট ২০টি ক্যান্ডেল) মধ্যে সর্বনিম্ন ট্রফ বা সর্বোচ্চ পিক খুঁজে বের করে, আর লাভ নির্ধারণ করা হয় স্টপ লসের শতাংশকে কনফিগার করা টেক প্রফিট অনুপাত (ডিফল্ট ৩ গুণ) দিয়ে গুণ করে। পজিশনের আকার হিসাব করা হয় অ্যাকাউন্টের মোট সম্পদের শতাংশ (ডিফল্ট ৩%) এবং নির্দিষ্ট সম্পদের স্টপ লসের পরিমাণের ভিত্তিতে।

সুবিধা

- কম্প্রেশন ইন্ডিকেটর প্রযুক্তি ব্যবহার করে মূল্যের প্রধান ট্রেডিং সংকেত নিষ্কাশন করে লাভের সম্ভাবনা বাড়ায়

- একাধিক সূচকের সংমিশ্রণ যাচাই করে মিথ্যা ব্রেকআউট এড়িয়ে যায় এবং ট্রেন্ডের দিক সঠিকভাবে নির্ধারণ করে

- গতিশীল স্টপ লস ও টেক প্রফিট নির্ধারণ করে ঝুঁকি নিয়ন্ত্রণযোগ্য ট্রেন্ড ট্র্যাকিং নিশ্চিত করে

- উচ্চ অস্থিরতার পরিবেশে ট্রেড নিশ্চিত করতে ভোলাটিলিটি সূচক ব্যবহার করে

- বহু-সময়সীমা বিশ্লেষণ কৌশলের স্থিতিশীলতা বাড়ায়

ঝুঁকি

- বুম হান্টার সূচকে কম্প্রেশন বিকৃত হতে পারে, যা ভুল সংকেত তৈরি করতে পারে

- হাল স্যুটের মিডল ব্যান্ডে পিছিয়ে পড়ার প্রবণতা আছে, ফলে তা মূল্য পরিবর্তন দ্রুত ট্র্যাক করতে পারে না

- অস্থিরতা কমে গেলে ট্রেডের সুযোগ হাতছাড়া হতে পারে বা ক্ষতি-বহির্ভূত পজিশন ক্লোজ হতে পারে

সমাধানের উপায়:

- কম্প্রেশন সূচকের প্যারামিটার সমন্বয় করে সংবেদনশীলতা ভারসাম্য রক্ষা করা

- EHMA-এর মতো এক্সপোনেনশিয়াল মুভিং এভারেজ ব্যবহার করে মিডল ব্যান্ড প্রতিস্থাপন করা

- অস্থিরতার ভ্রান্তি এড়াতে অন্যান্য বিচার সূচক যুক্ত করা

অপ্টিমাইজেশন

এই কৌশলটি নিম্নলিখিত দিকগুলি থেকে অপ্টিমাইজ করা যেতে পারে:

-

প্যারামিটার অপ্টিমাইজেশন: সূচকের প্যারামিটার যেমন পিরিয়ড দৈর্ঘ্য, কম্প্রেশন কোএফিশিয়েন্ট ইত্যাদি পরিবর্তন করে সর্বোত্তম প্যারামিটার কম্বিনেশন পাওয়া

-

টাইমফ্রেম অপ্টিমাইজেশন: বিভিন্ন সময়সীমা (১ মিনিট, ৫ মিনিট, ৩০ মিনিট ইত্যাদি) পরীক্ষা করে সবচেয়ে উপযুক্ত ট্রেডিং পিরিয়ড খুঁজে বের করা

-

পজিশন সাইজ অপ্টিমাইজেশন: প্রতিটি ট্রেডের পজিশনের আকার ও অনুপাত পরিবর্তন করে সর্বোত্তম মূলধন ব্যবহার কৌশল বের করা

-

স্টপ লস অপ্টিমাইজেশন: বিভিন্ন ট্রেডিং জোড়ার জন্য স্টপ লস অবস্থান সামঞ্জস্য করে সর্বোত্তম রিস্ক-রিওয়ার্ড অনুপাত অর্জন করা

-

শর্ত অপ্টিমাইজেশন: সূচকের ফিল্টার শর্ত বাড়ানো বা কমানোর মাধ্যমে আরও নির্ভুল এন্ট্রি টাইমিং পাওয়া

উপসংহার

এই কৌশলটি বুম হান্টার, হাল স্যুট এবং ভোলাটিলিটি অসিলেটর – এই তিনটি সূচকের সমন্বিত ব্যবহারের মাধ্যমে বহু-সময়সীমায় ট্রেন্ড ট্র্যাকিং ট্রেডিং বাস্তবায়ন করে, যা মূল্যের আকস্মিক আচরণ কার্যকরভাবে শনাক্ত করতে পারে এবং উচ্চ অস্থিলতা সম্পন্ন ডিজিটাল সম্পদের জন্য উপযুক্ত। এই কৌশলটির ঝুঁকি নিয়ন্ত্রণযোগ্য, এবং প্যারামিটার, ফিল্টার শর্ত ও স্টপ লস ইত্যাদির বিভিন্ন দিক থেকে অপ্টিমাইজেশন করে একে আরও কার্যকর ও সম্প্রসারণযোগ্য করা যায়।

- 1