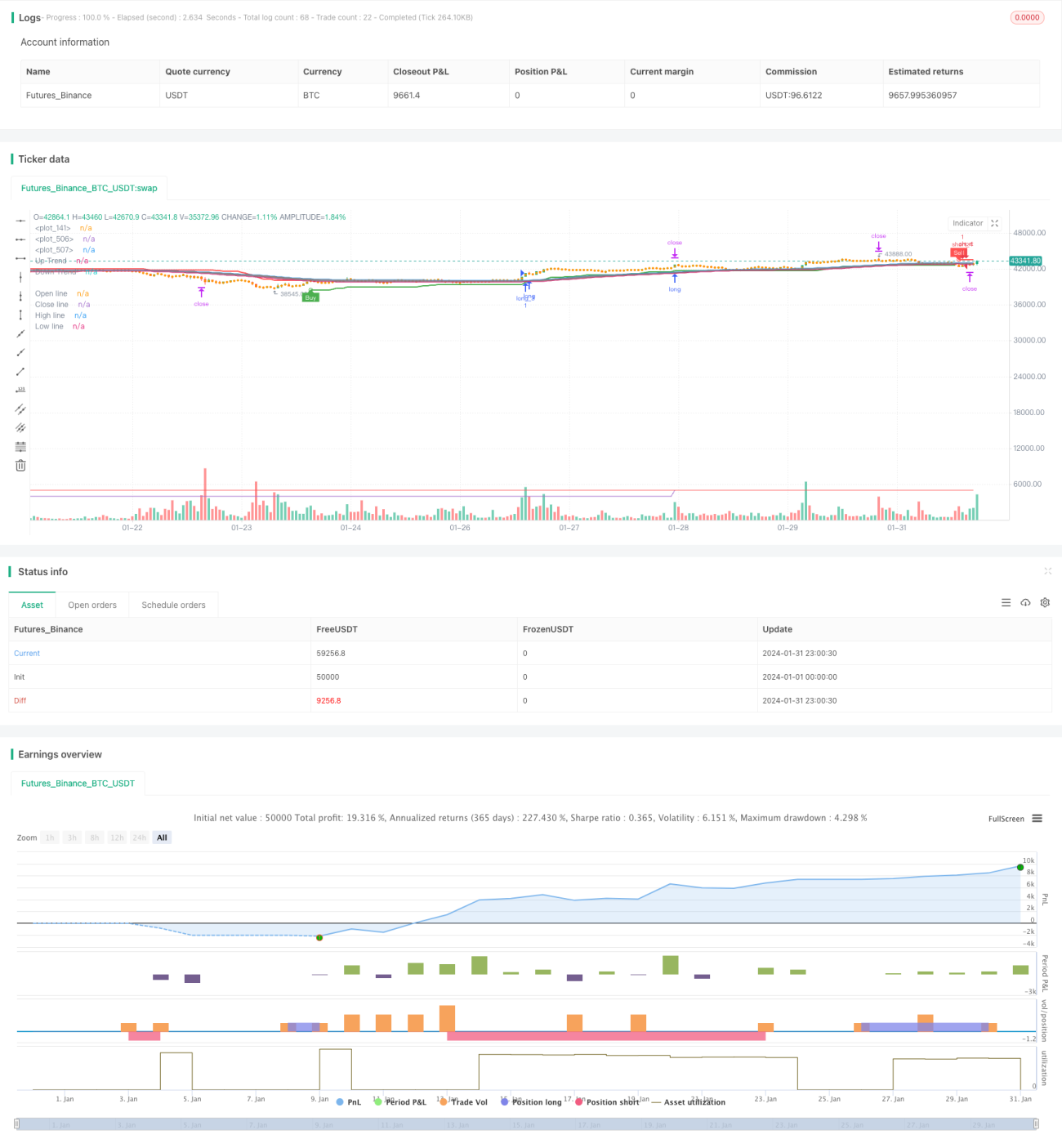

তিনটি নিশ্চিতকরণসহ প্রবণতা অনুসরণ কৌশল

সারসংক্ষেপ

ট্রিপল কনফার্মেশন ট্রেন্ড ফলোয়িং স্ট্রাটেজি তিনটি প্রধান ইন্ডিকেটর—মুভিং এভারেজ, মাইন্ড লাইন এবং সুপার ট্রেন্ড—এর সংকেত একত্রিত করে উচ্চ সম্ভাবনার সাথে ট্রেন্ড ধরা সম্ভব করে। যখন তিনটি ইন্ডিকেটর একইসাথে ক্রয় বা বিক্রয় সংকেত দেয়, কৌশলটি সময়মতো পজিশনে প্রবেশ করে ট্রেন্ড অনুসরণ করে; ট্রেন্ড বিপরীত হলে দ্রুত লস কেটে শর্ট পজিশন নেয়।

কৌশলের নীতি

মুভিং এভারেজ দিয়ে প্রধান ট্রেন্ড নির্ধারণ

কৌশলটি প্রধান ট্রেন্ডের দিক নির্ধারণ করতে ৫২ পিরিয়ডের মুভিং এভারেজ ব্যবহার করে। যখন দাম মুভিং এভারেজের উপরে উঠে যায়, তখন আপট্রেন্ড ধরা হয়; যখন দাম নিচে নামে, তখন ডাউনট্রেন্ড ধরা হয়।

মাইন্ড লাইন দিয়ে সেকেন্ডারি রিভার্সাল শনাক্তকরণ

একইসাথে কৌশলটি স্বল্পমেয়াদী সেকেন্ডারি রিভার্সাল শনাক্ত করতে মাইন্ড লাইন ব্যবহার করে। মাইন্ড লাইনের গণনা মুভিং এভারেজের মতোই, তবে CLOSE মূল্যের পরিবর্তে ওপেন মূল্য ব্যবহার করা হয়, যা দামের রিভার্সাল তথ্য আরও দ্রুত প্রতিফলিত করে। যখন দাম নিম্নগামী মাইন্ড লাইনের উপরে উঠে যায়, তখন এটি প্রাইসের স্বল্পমেয়াদী স্থিতিশীলতা ও পুনরুদ্ধারের সংকেত দেয়; যখন দাম ঊর্ধ্বগামী মাইন্ড লাইনের নিচে নামে, তখন এটি প্রাইসের স্বল্পমেয়াদী পতনের সংকেত দেয়।

সুপার ট্রেন্ড দিয়ে রিভার্সাল পয়েন্ট নির্ধারণ

কৌশলটি আরও সুপার ট্রেন্ড ইন্ডিকেটরের সাথে যুক্ত হয় যা গুরুত্বপূর্ণ রিভার্সাল পয়েন্ট নির্ধারণ করে। সুপার ট্রেন্ড ইন্ডিকেটর ATR ইন্ডিকেটরের উইন্ডো পিরিয়ড এবং দামের ডেটা একত্রিত করে চ্যানেলের উপর ও নিচের রেখা গতিশীলভাবে সমন্বয় করে, যার ফলে রিভার্সালের সময় নির্ধারণ করে।

ট্রিপল কনফার্মেশন সিগন্যাল ফিল্টারিং

যখন মুভিং এভারেজ, মাইন্ড লাইন এবং সুপার ট্রেন্ড—এই তিনটি ইন্ডিকেটর একইসাথে ক্রয় সংকেত দেয়, তখনই কৌশলটি লং পজিশন নেবে; যখন তিনটি ইন্ডিকেটর একইসাথে বিক্রয় সংকেত দেয়, তখনই কৌশলটি শর্ট পজিশন নেবে। ট্রিপল ইন্ডিকেটর কনফার্মেশনের মাধ্যমে ভুয়া সংকেত কার্যকরভাবে ফিল্টার করা যায় এবং এন্ট্রির সম্ভাবনা বৃদ্ধি পায়।

সুবিধা বিশ্লেষণ

বহুমাত্রিক বিচার, উচ্চ সম্ভাবনা

কৌশলটি তিনটি ইন্ডিকেটর—মুভিং এভারেজ, মাইন্ড লাইন এবং সুপার ট্রেন্ড—একত্রিত করে বিভিন্ন মাত্রা থেকে ট্রেন্ড এবং গুরুত্বপূর্ণ পয়েন্ট নির্ধারণ করে, যা উচ্চ সম্ভাবনার এন্ট্রি নিশ্চিত করে।

দ্রুত প্রতিক্রিয়া, রিয়েল-টাইম ট্র্যাকিং

মাইন্ড লাইনের অন্তর্ভুক্তি নিশ্চিত করে যে কৌশলটি দামের স্বল্পমেয়াদী রিভার্সালে দ্রুত প্রতিক্রিয়া জানাতে পারে; ATR অ্যাডাপ্টিভ চ্যানেলের সুপার ট্রেন্ড ইন্ডিকেটরও রিয়েল-টাইমে দামের পরিবর্তন ট্র্যাক করতে পারে।

স্বয়ংক্রিয় টেক প্রফিট ও স্টপ লস, কার্যকর ঝুঁকি নিয়ন্ত্রণ

কৌশলটিতে অন্তর্নির্মিত স্বয়ংক্রিয় টেক প্রফিট ও স্টপ লস যুক্তি রয়েছে, যা ATR অনুযায়ী গতিশীলভাবে টেক প্রফিট ও স্টপ লস পয়েন্ট সমন্বয় করে, একক লস কার্যকরভাবে নিয়ন্ত্রণ করে।

ঝুঁকি ও সমাধান

অত্যধিক ট্রেডিং ফ্রিকোয়েন্সির ঝুঁকি

কৌশলের ট্রেডিং সংকেত ঘন ঘন আসার কারণে অত্যধিক ট্রেডিং হতে পারে। মুভিং এভারেজের পিরিয়ড প্যারামিটার যথাযথভাবে বাড়িয়ে ট্রেডিং ফ্রিকোয়েন্সি কমানো যেতে পারে।

রিভার্সাল অনিশ্চয়তার ঝুঁকি

মাইন্ড লাইন এবং সুপার ট্রেন্ড ইন্ডিকেটর দ্বারা রিভার্সাল পয়েন্ট নির্ধারণের কার্যকারিতা নিশ্চিত নয়, ভুল বিচারের ঝুঁকি থাকতে পারে। ইন্ডিকেটর প্যারামিটারে ফিল্টারিং শর্ত যোগ করা যেতে পারে যাতে উচ্চতর সম্ভাবনার রিভার্সাল সংকেত নিশ্চিত হয়।

রেঞ্জ বাজারে লসের ঝুঁকি

রেঞ্জ বাজারে বারবার ক্রসওভারের কারণে কৌশলটি ঘন ঘন পজিশন খোলে এবং স্টপ লসে আঘাত করে, যার ফলে লসের ঝুঁকি তৈরি হয়। রেঞ্জ বাজার শনাক্ত করে এই পর্যায়ে কৌশল ট্রেডিং বন্ধ রাখা যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

ভোলাটিলিটি ইন্ডিকেটর যুক্ত করা

বলিঞ্জার ব্যান্ডের মতো ভোলাটিলিটি ইন্ডিকেটর যুক্ত করার কথা বিবেচনা করা যেতে পারে। যখন দাম বলিঞ্জার ব্যান্ডের উপরের বা নিচের রেখার কাছে পৌঁছায়, তখন নতুন পজিশন খোলা এড়ানো যায়, যা রেঞ্জ বাজারের ঝুঁকি কার্যকরভাবে এড়াতে সাহায্য করে।

এন্ট্রি ফিল্টারিং শর্ত বৃদ্ধি

অন্যান্য সহায়ক ইন্ডিকেটর যেমন KDJ, MACD ইত্যাদি যোগ করার চেষ্টা করা যেতে পারে; যখন সেগুলিও একইসাথে সংকেত দেয়, তখনই এন্ট্রি করা উচিত। এটি ভুয়া সংকেত আরও ফিল্টার করতে এবং অপ্রয়োজনীয় ট্রেডিং কমাতে সাহায্য করে।

টেক প্রফিট ও স্টপ লস কৌশল অপ্টিমাইজেশন

টেক প্রফিট ও স্টপ লস কৌশল অপ্টিমাইজ করা যেতে পারে, যেমন ট্রেইলিং স্টপ, এক্সপোনেনশিয়াল ট্রেইলিং স্টপ, হাফ পজিশন ইন্টারভাল টেক প্রফিট ইত্যাদি পদ্ধতি ব্যবহার করে, যাতে মুনাফা আরও বেশি এবং স্থিতিশীল হয়।

সারসংক্ষেপ

ট্রিপল কনফার্মেশন ট্রেন্ড ফলোয়িং স্ট্রাটেজি মুভিং এভারেজ, মাইন্ড লাইন এবং সুপার ট্রেন্ড—এই তিনটি প্রধান ইন্ডিকেটরের সুবিধা সম্পূর্ণরূপে ব্যবহার করে, যার ফলে উচ্চ সম্ভাবনার সাথে ট্রেন্ড সনাক্ত ও ধরা সম্ভব হয়। একইসাথে স্বয়ংক্রিয় টেক প্রফিট ও স্টপ লস ব্যবস্থা একক লস কার্যকরভাবে নিয়ন্ত্রণ করে। আরও অপ্টিমাইজেশনের যোগ্য দিক হলো, অন্যান্য সহায়ক ইন্ডিকেটর যুক্ত করে এন্ট্রি ফিল্টার করা এবং টেক প্রফিট ও স্টপ লস কৌশল উন্নত করা, যা কৌশলটিকে আরও ব্যবহারিক করে তুলবে।

- 1