বহু সূচক ট্রেন্ড ফলোয়িং কৌশল

সারসংক্ষেপ

এই কৌশলটির নাম "Jancok Strategycs v3"। এটি একটি মাল্টি-ইন্ডিকেটর ট্রেন্ড ফলোয়িং কৌশল যা মুভিং এভারেজ (MA), মুভিং এভারেজ কনভার্জেন্স ডাইভার্জেন্স (MACD), রিলেটিভ স্ট্রেন্থ ইনডেক্স (RSI) এবং এভারেজ ট্রু রেঞ্জ (ATR) এর উপর ভিত্তি করে তৈরি। এই কৌশলের মূল ধারণা হলো একাধিক ইন্ডিকেটরের সমন্বয় ব্যবহার করে বাজারের ট্রেন্ড নির্ণয় করা এবং সেই ট্রেন্ডের দিকে ট্রেড করা। একই সাথে, এই কৌশলটি ডায়নামিক স্টপ লস এবং টেক প্রফিট পদ্ধতি এবং ATR-ভিত্তিক রিস্ক ম্যানেজমেন্ট ব্যবহার করে ঝুঁকি নিয়ন্ত্রণ ও লাভ অপ্টিমাইজ করে।

কৌশলের মূলনীতি

এই কৌশলটি বাজারের ট্রেন্ড নির্ণয়ের জন্য নিম্নলিখিত চারটি ইন্ডিকেটর ব্যবহার করে:

- মুভিং এভারেজ (MA): স্বল্পমেয়াদী (9 পিরিয়ড) এবং দীর্ঘমেয়াদী (21 পিরিয়ড) মুভিং এভারেজ গণনা করা হয়। যখন স্বল্পমেয়াদী এভারেজ দীর্ঘমেয়াদী এভারেজের উপরে উঠে যায়, তখন তা ঊর্ধ্বমুখী ট্রেন্ড নির্দেশ করে; যখন স্বল্পমেয়াদী এভারেজ দীর্ঘমেয়াদী এভারেজের নিচে নেমে যায়, তখন তা নিম্নমুখী ট্রেন্ড নির্দেশ করে।

- মুভিং এভারেজ কনভার্জেন্স ডাইভার্জেন্স (MACD): MACD লাইন এবং সিগন্যাল লাইন গণনা করা হয়। যখন MACD লাইন সিগন্যাল লাইনের উপরে উঠে যায়, তখন তা ঊর্ধ্বমুখী ট্রেন্ড নির্দেশ করে; যখন MACD লাইন সিগন্যাল লাইনের নিচে নেমে যায়, তখন তা নিম্নমুখী ট্রেন্ড নির্দেশ করে।

- রিলেটিভ স্ট্রেন্থ ইনডেক্স (RSI): 14 পিরিয়ডের RSI গণনা করা হয়। যখন RSI 70-এর বেশি হয়, তখন বাজার অতিরিক্ত কেনা হতে পারে; যখন RSI 30-এর কম হয়, তখন বাজার অতিরিক্ত বিক্রি হতে পারে।

- এভারেজ ট্রু রেঞ্জ (ATR): 14 পিরিয়ডের ATR গণনা করা হয়, যা বাজারের অস্থিরতা পরিমাপ করতে এবং স্টপ লস ও টেক প্রফিট পয়েন্ট নির্ধারণ করতে ব্যবহৃত হয়।

এই কৌশলের ট্রেডিং লজিক নিম্নরূপ:

- যখন স্বল্পমেয়াদী এভারেজ দীর্ঘমেয়াদী এভারেজের উপরে উঠে যায়, MACD লাইন সিগন্যাল লাইনের উপরে উঠে যায়, ভলিউম তার মুভিং এভারেজের চেয়ে বেশি হয় এবং অস্থিরতা থ্রেশহোল্ডের নিচে থাকে, তখন লং পজিশন খোলা হয়।

- যখন স্বল্পমেয়াদী এভারেজ দীর্ঘমেয়াদী এভারেজের নিচে নেমে যায়, MACD লাইন সিগন্যাল লাইনের নিচে নেমে যায়, ভলিউম তার মুভিং এভারেজের চেয়ে বেশি হয় এবং অস্থিরতা থ্রেশহোল্ডের নিচে থাকে, তখন শর্ট পজিশন খোলা হয়।

- স্টপ লস এবং টেক প্রফিট পয়েন্ট ATR-এর ভিত্তিতে ডায়নামিকভাবে সেট করা হয়: স্টপ লস ATR-এর 2 গুণ এবং টেক প্রফিট ATR-এর 4 গুণ।

- ঐচ্ছিকভাবে ATR-ভিত্তিক ট্রেইলিং স্টপ ব্যবহার করা যেতে পারে, যেখানে ট্রেইলিং স্টপ পয়েন্ট ATR-এর 2.5 গুণ।

কৌশলের সুবিধা

- একাধিক ইন্ডিকেটরের সমন্বয়ে ট্রেন্ড নির্ণয় করা, যা ট্রেন্ড নির্ণয়ের নির্ভুলতা বাড়ায়।

- ডায়নামিক স্টপ লস এবং টেক প্রফিট, যা বাজারের অস্থিরতার সাথে নিজেকে খাপ খাইয়ে নেয় এবং ঝুঁকি নিয়ন্ত্রণ ও লাভ অপ্টিমাইজ করতে সাহায্য করে।

- ভলিউম এবং অস্থিরতা ফিল্টার অন্তর্ভুক্ত করা হয়েছে, যা কম তারল্য এবং উচ্চ অস্থিরতার সময় ট্রেড এড়িয়ে মিথ্যা সংকেত কমায়।

- ঐচ্ছিক ট্রেইলিং স্টপ, যা ট্রেন্ড অব্যাহত থাকলে আরও বেশি মুনাফা ধরে রাখতে সাহায্য করে।

কৌশলের ঝুঁকি

- সাইডওয়ে মার্কেট বা ট্রেন্ড পরিবর্তনের সময় মিথ্যা সংকেত তৈরি হতে পারে, যার ফলে লোকসান হতে পারে।

- প্যারামিটার সেটিংস কৌশলের পারফরম্যান্সের উপর বড় প্রভাব ফেলে এবং বিভিন্ন বাজার ও সম্পদের জন্য অপটিমাইজ করতে হয়।

- অতিরিক্ত অপটিমাইজেশন ওভারফিটিং-এর কারণ হতে পারে, যা প্রকৃত ট্রেডিংয়ে খারাপ ফলাফল দিতে পারে।

- বাজারের অস্বাভাবিক অস্থিরতা বা ব্ল্যাক সোয়ান ঘটনা发生时, কৌশলটি বড় ক্ষতির সম্মুখীন হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- আরও ইন্ডিকেটর অন্তর্ভুক্ত করা, যেমন বোলিঙ্গার ব্যান্ড, স্টোকাস্টিক ইত্যাদি, যা ট্রেন্ড নির্ণয়ের নির্ভুলতা আরও বাড়াতে পারে।

- প্যারামিটার নির্বাচন অপ্টিমাইজ করা, যেমন জিনেটিক অ্যালগরিদম, গ্রিড সার্চ ইত্যাদি ব্যবহার করে সর্বোত্তম প্যারামিটার সংমিশ্রণ খুঁজে বের করা।

- বিভিন্ন বাজার এবং সম্পদের জন্য ভিন্ন প্যারামিটার এবং নিয়ম সেট করা, যা কৌশলের অভিযোজনযোগ্যতা বাড়ায়।

- পজিশন ম্যানেজমেন্ট যোগ করা, বাজারের ট্রেন্ড শক্তি এবং অ্যাকাউন্টের ঝুঁকির উপর ভিত্তি করে পজিশনের সাইজ ডায়নামিকভাবে সামঞ্জস্য করা।

- সর্বোচ্চ ড্রডাউন সীমা নির্ধারণ করা, যখন অ্যাকাউন্ট সর্বোচ্চ ড্রডাউনে পৌঁছায়, তখন ট্রেড স্থগিত করা বা পজিশনের সাইজ কমিয়ে ঝুঁকি নিয়ন্ত্রণ করা।

সারসংক্ষেপ

"Jancok Strategycs v3" হল একটি মাল্টি-ইন্ডিকেটর কম্বিনেশন ভিত্তিক ট্রেন্ড ফলোয়িং কৌশল। এটি মুভিং এভারেজ, MACD, RSI এবং ATR-এর মতো ইন্ডিকেটর ব্যবহার করে বাজারের ট্রেন্ড নির্ণয় করে এবং ডায়নামিক স্টপ লস-টেক প্রফিট ও ট্রেইলিং স্টপের মতো রিস্ক ম্যানেজমেন্ট পদ্ধতি ব্যবহার করে ঝুঁকি নিয়ন্ত্রণ ও লাভ অপ্টিমাইজ করে। এই কৌশলের সুবিধা হলো ট্রেন্ড নির্ণয়ের উচ্চ নির্ভুলতা, নমনীয় রিস্ক ম্যানেজমেন্ট এবং শক্তিশালী অভিযোজনযোগ্যতা। তবে এতে কিছু ঝুঁকিও রয়েছে, যেমন মিথ্যা সংকেত, প্যারামিটার সেটিংসের সংবেদনশীলতা এবং ব্ল্যাক সোয়ান ঘটনা। ভবিষ্যতে আরও ইন্ডিকেটর অন্তর্ভুক্ত করা, প্যারামিটার নির্বাচন অপ্টিমাইজ করা, পজিশন ম্যানেজমেন্ট যোগ করা এবং সর্বোচ্চ ড্রডাউন সীমা নির্ধারণের মাধ্যমে কৌশলের পারফরম্যান্স এবং স্থিতিশীলতা আরও উন্নত করা যেতে পারে।

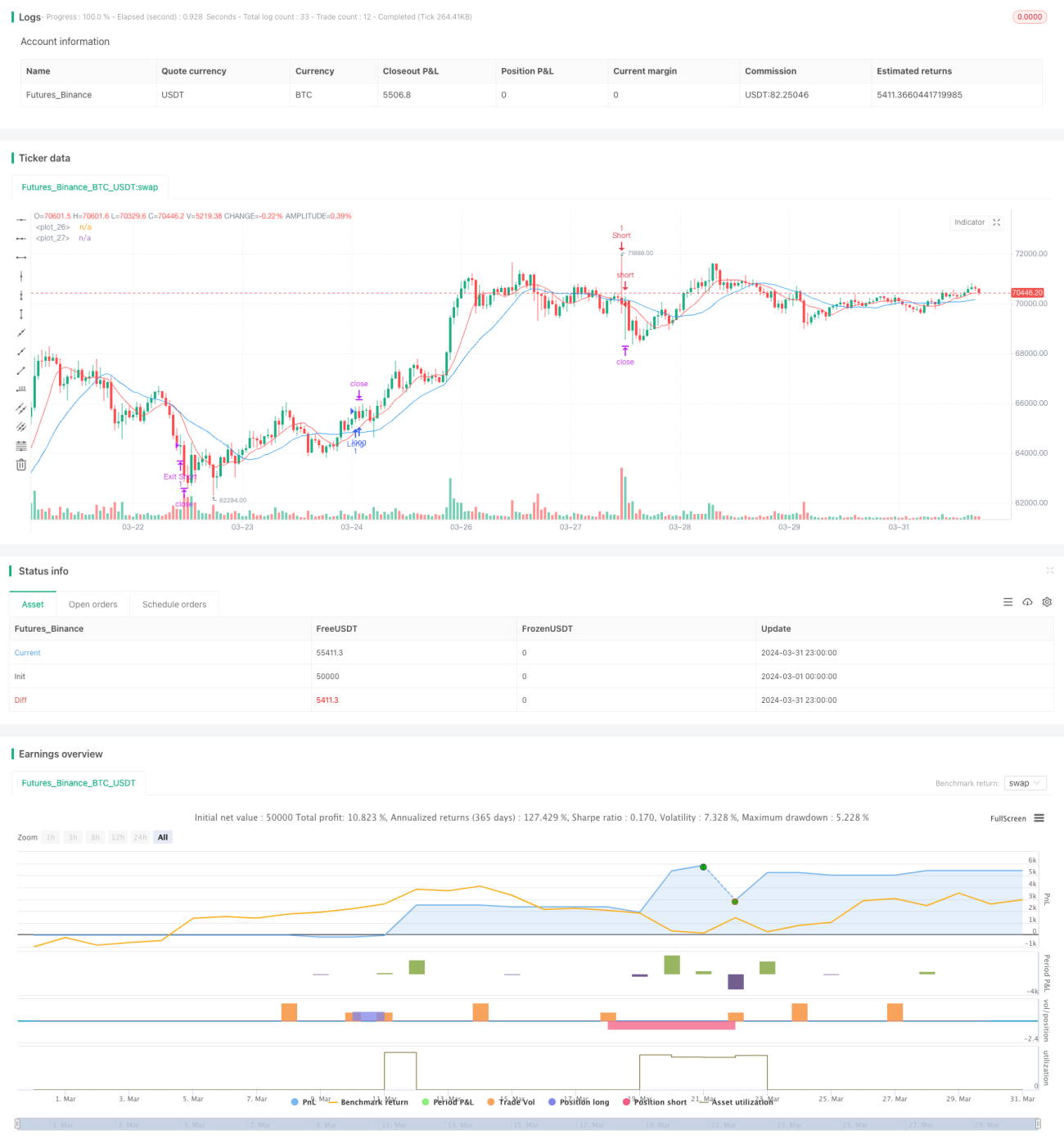

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © financialAccou42381

//@version=5- 1