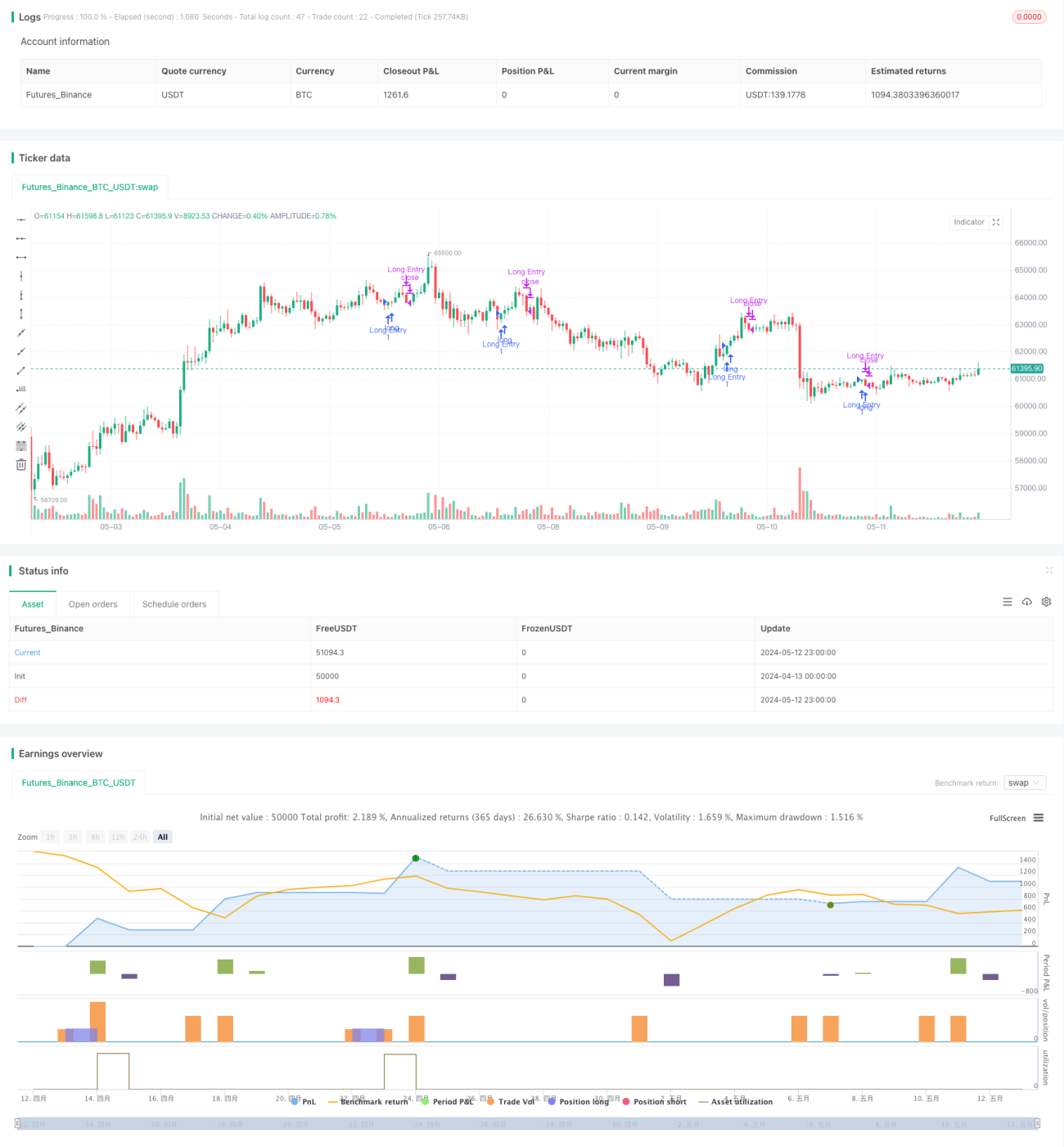

সংক্ষিপ্ত বিবরণ

এই কৌশলের মূল ধারণা হল উপরের শেডবিহীন বুলিশ ক্যান্ডেল খুঁজে বের করা ক্রয় সংকেত হিসেবে, এবং যখন দাম আগের ক্যান্ডেলের সর্বনিম্ন স্তরের নিচে নেমে যায় তখন পজিশন বন্ধ করা। কৌশলটি বুলিশ ক্যান্ডেলের খুব ছোট উপরের শেডের বৈশিষ্ট্য ব্যবহার করে, যা ইঙ্গিত দেয় যে বহু পক্ষের শক্তি প্রবল এবং শেয়ারের দাম বাড়ার সম্ভাবনা বেশি। একই সাথে, আগের ক্যান্ডেলের সর্বনিম্ন স্তর স্টপ-লস হিসেবে ব্যবহার করে কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করা যায়।

কৌশলের নীতি

- বর্তমান ক্যান্ডেলটি বুলিশ ক্যান্ডেল কিনা তা নির্ধারণ করুন (ক্লোজ মূল্য ওপেন মূল্যের চেয়ে বেশি)।

- বর্তমান ক্যান্ডেলের উপরের শেডের দৈর্ঘ্য এবং ক্যান্ডেলের বডির দৈর্ঘ্যের অনুপাত গণনা করুন।

- যদি উপরের শেডের অনুপাত ৫% এর কম হয়, তাহলে এটি একটি বৈধ উপরের শেডবিহীন বুলিশ ক্যান্ডেল হিসেবে বিবেচিত হবে এবং ক্রয় সংকেত তৈরি হবে।

- ক্রয়ের পর আগের ক্যান্ডেলের সর্বনিম্ন মূল্য স্টপ-লস স্তর হিসেবে রেকর্ড করুন।

- যখন দাম স্টপ-লস স্তরের নিচে নেমে যায়, তখন পজিশন বন্ধ করে প্রস্থান করুন।

কৌশলের সুবিধা

- উপরের শেডবিহীন বুলিশ ক্যান্ডেল নির্বাচন করে প্রবেশ করলে ট্রেন্ডের শক্তি বেশি থাকে এবং সাফল্যের হার বেশি হয়।

- আগের ক্যান্ডেলের সর্বনিম্ন স্তর স্টপ-লস হিসেবে ব্যবহার করায় ঝুঁকি নিয়ন্ত্রণযোগ্য।

- যুক্তি সহজ, বাস্তবায়ন এবং অপ্টিমাইজ করা সহজ।

- ট্রেন্ডিং মার্কেটে ব্যবহারের জন্য উপযুক্ত।

কৌশলের ঝুঁকি

- ক্রয় সংকেতের পরপরই দাম ফিরে এসে স্টপ-লস ট্রিগার হওয়ার সম্ভাবনা থাকে।

- উচ্চ অস্থিরতার জন্য যন্ত্রের ক্ষেত্রে স্টপ-লস স্তর ক্রয় মূল্যের খুব কাছাকাছি নির্ধারণ করা হতে পারে, যার ফলে অকাল স্টপ-আউট হতে পারে।

- লাভের লক্ষ্যের অভাব থাকায় সর্বোত্তম প্রস্থান সময় নির্ধারণ করা কঠিন।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- এমএ, ম্যাকডি ইত্যাদি অন্যান্য সূচকের সাথে সমন্বয় করে ট্রেন্ডের শক্তি নিশ্চিত করা যেতে পারে, যা প্রবেশ সংকেতের কার্যকারিতা উন্নত করবে।

- উচ্চ অস্থিরতার যন্ত্রের জন্য স্টপ-লস স্তর আরও দূরবর্তী স্থানে নির্ধারণ করা যেতে পারে, যেমন আগের এন সংখ্যক ক্যান্ডেলের সর্বনিম্ন বিন্দু, যা স্টপ-লসের ফ্রিকোয়েন্সি কমাবে।

- লাভের লক্ষ্য নির্ধারণ করা যেতে পারে, যেমন এন গুণ এটিআর বা শতাংশ লাভ, যাতে সময়মত মুনাফা লক করা যায়।

- পজিশন ম্যানেজমেন্ট যোগ করার কথা বিবেচনা করা যেতে পারে, যেমন সংকেতের শক্তি অনুযায়ী পজিশনের আকার সামঞ্জস্য করা।

সারসংক্ষেপ

এই কৌশলটি উপরের শেডবিহীন বুলিশ ক্যান্ডেল নির্বাচন করে প্রবেশ করে এবং আগের ক্যান্ডেলের সর্বনিম্ন স্তর স্টপ-লস হিসেবে ব্যবহার করে ট্রেন্ডিং মার্কেটে কার্যকরভাবে মুনাফা অর্জন করতে পারে। তবে কৌশলটির কিছু সীমাবদ্ধতা রয়েছে, যেমন স্টপ-লসের স্থান নমনীয় নয় এবং লাভের লক্ষ্যের অভাব রয়েছে। অন্যান্য সূচক সংযোজন করে সংকেত ফিল্টার করা, স্টপ-লসের অবস্থান অপ্টিমাইজ করা এবং লাভের লক্ষ্য নির্ধারণ করার মাধ্যমে উন্নতি করা যেতে পারে, যা কৌশলটিকে আরও স্থিতিশীল এবং কার্যকর করবে।

- 1