RSI দ্বৈত পার্থক্য কৌশল

সংক্ষিপ্ত বিবরণ

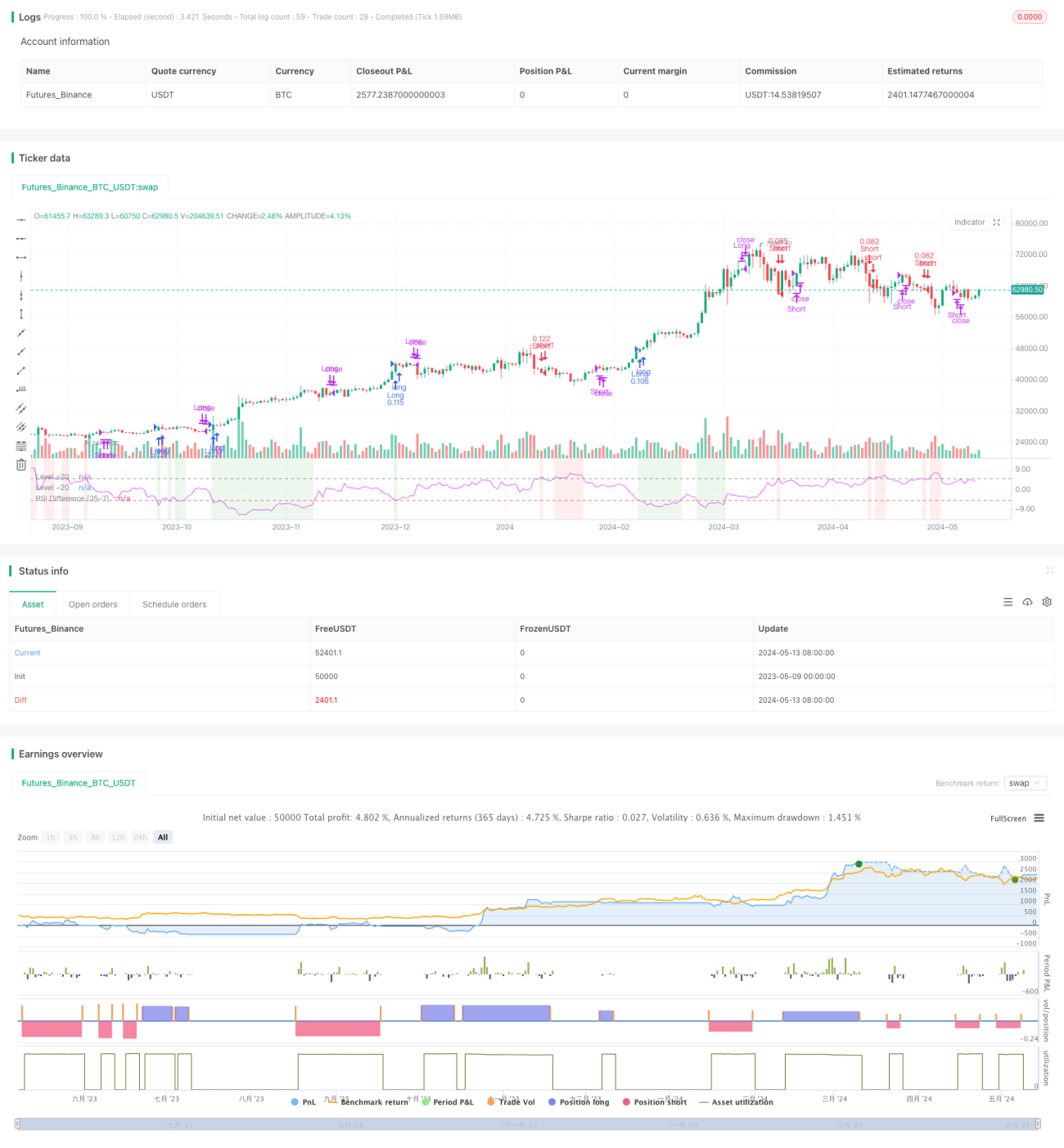

RSI দ্বৈত পার্থক্য কৌশল হল একটি কৌশল যা দুটি ভিন্ন সময়কালের আপেক্ষিক শক্তি সূচক (RSI)-এর মধ্যে পার্থক্য ব্যবহার করে ট্রেডিং সিদ্ধান্ত নেওয়ার জন্য। ঐতিহ্যবাহী একক RSI কৌশল থেকে ভিন্ন, এই কৌশল স্বল্পমেয়াদী RSI এবং দীর্ঘমেয়াদী RSI-এর পার্থক্য বিশ্লেষণ করে বাজারের গতিশীলতা সম্পর্কে আরও সূক্ষ্ম বিশ্লেষণ পদ্ধতি প্রদান করে। এই পদ্ধতি ট্রেডারদের অতিরিক্ত কেনা এবং অতিরিক্ত বিক্রির বাজার পরিস্থিতি আরও সঠিকভাবে বুঝতে সাহায্য করে, যার ফলে আরও নির্ভুল ট্রেডিং সিদ্ধান্ত নেওয়া যায়।

কৌশলের মূলনীতি

এই কৌশলের মূল ভিত্তি হল দুটি ভিন্ন সময়কালের RSI সূচক গণনা করা এবং তাদের মধ্যে পার্থক্য বিশ্লেষণ করা। বিশেষভাবে, এই কৌশলটি একটি স্বল্পমেয়াদী RSI (ডিফল্ট ২১ দিন) এবং একটি দীর্ঘমেয়াদী RSI (ডিফল্ট ৪২ দিন) ব্যবহার করে। দীর্ঘমেয়াদী RSI থেকে স্বল্পমেয়াদী RSI-এর পার্থক্য গণনা করে আমরা একটি RSI পার্থক্য সূচক পাই। যখন RSI পার্থক্য সূচক -৫-এর নিচে থাকে, তখন এটি নির্দেশ করে যে স্বল্পমেয়াদী গতি বৃদ্ধি পাচ্ছে, এবং সেই সময়ে লং (কেনা) অবস্থান নেওয়ার কথা বিবেচনা করা যেতে পারে; যখন RSI পার্থক্য সূচক +৫-এর উপরে থাকে, তখন এটি নির্দেশ করে যে স্বল্পমেয়াদী গতি দুর্বল হচ্ছে, এবং সেই সময়ে শর্ট (বিক্রি) অবস্থান নেওয়ার কথা বিবেচনা করা যেতে পারে।

কৌশলের সুবিধা

RSI দ্বৈত পার্থক্য কৌশলের সুবিধা হল এটি বাজারের আরও সূক্ষ্ম বিশ্লেষণ পদ্ধতি প্রদান করে। বিভিন্ন সময়কালের RSI-এর মধ্যে পার্থক্য বিশ্লেষণ করে এই কৌশলটি বাজারের গতির পরিবর্তন আরও নির্ভুলভাবে চিহ্নিত করতে সক্ষম, ফলে ট্রেডারদের জন্য আরও নির্ভরযোগ্য ট্রেডিং সংকেত প্রদান করে। এছাড়াও, এই কৌশলে পজিশন হোল্ডিং দিন এবং লাভ স্টপ ও লস স্টপের ব্যবস্থা যুক্ত করা হয়েছে, যা ট্রেডারদের তাদের ঝুঁকি এক্সপোজার আরও নমনীয়ভাবে নিয়ন্ত্রণ করতে সহায়তা করে।

কৌশলের ঝুঁকি

যদিও RSI দ্বৈত পার্থক্য কৌশলের অনেক সুবিধা রয়েছে, তবুও এতে কিছু সম্ভাব্য ঝুঁকি রয়েছে। প্রথমত, এই কৌশলটি RSI পার্থক্য সূচকের সঠিক ব্যাখ্যার উপর নির্ভর করে; যদি ট্রেডারের সূচক সম্পর্কে বোধগম্যতায় ভুল থাকে, তাহলে এটি ভুল ট্রেডিং সিদ্ধান্তের দিকে নিয়ে যেতে পারে। দ্বিতীয়ত, অস্থির বাজার পরিবেশে এই কৌশলটি বেশি সংখ্যক ভুয়া সংকেত তৈরি করতে পারে, যা ঘন ঘন ট্রেডিং এবং উচ্চ ট্রেডিং খরচের কারণ হতে পারে। এই ঝুঁকিগুলি কমানোর জন্য, ট্রেডাররা RSI দ্বৈত পার্থক্য কৌশলের ট্রেডিং সংকেতগুলি যাচাই করার জন্য অন্যান্য প্রযুক্তিগত সূচক বা মৌলিক বিশ্লেষণ যুক্ত করার কথা বিবেচনা করতে পারেন।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

RSI দ্বৈত পার্থক্য কৌশলের কর্মক্ষমতা আরও উন্নত করার জন্য আমরা নিম্নলিখিত দিকগুলি থেকে কৌশলটি অপ্টিমাইজ করার কথা বিবেচনা করতে পারি:

-

প্যারামিটার অপ্টিমাইজেশন: RSI সময়কাল, RSI পার্থক্য থ্রেশহোল্ড, পজিশন হোল্ডিং দিন ইত্যাদি প্যারামিটারগুলি অপ্টিমাইজ করে আমরা বর্তমান বাজার পরিবেশের জন্য সবচেয়ে উপযুক্ত প্যারামিটার সংমিশ্রণ খুঁজে পেতে পারি, যার ফলে কৌশলের লাভজনকতা এবং স্থিতিশীলতা বৃদ্ধি পাবে।

-

সংকেত ফিল্টারিং: অন্যান্য প্রযুক্তিগত সূচক বা বাজারের মনোভাব সূচক যুক্ত করে RSI দ্বৈত পার্থক্য কৌশলের ট্রেডিং সংকেতগুলির দ্বিতীয় নিশ্চিতকরণ করা, যাতে ভুয়া সংকেতের উপস্থিতি হ্রাস পায়।

-

ঝুঁকি নিয়ন্ত্রণ: লাভ স্টপ ও লস স্টপের ব্যবস্থা অপ্টিমাইজ করা, অথবা গতিশীল ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা চালু করা, যা বাজারের অস্থিরতার পরিবর্তনের সাথে সাথে পজিশনের আকার গতিশীলভাবে সামঞ্জস্য করে, যাতে কৌশলের ঝুঁকি এক্সপোজার আরও ভালভাবে নিয়ন্ত্রণ করা যায়।

-

বহু-বাজার অভিযোজন: RSI দ্বৈত পার্থক্য কৌশলটি অন্যান্য আর্থিক বাজারগুলিতে (যেমন বৈদেশিক মুদ্রা, পণ্য, বন্ড ইত্যাদি) সম্প্রসারণ করে কৌশলটির সার্বজনীনতা এবং দৃঢ়তা যাচাই করা।

সারসংক্ষেপ

RSI দ্বৈত পার্থক্য কৌশল হল আপেক্ষিক শক্তি সূচকের উপর ভিত্তি করে একটি গতি ট্রেডিং কৌশল, যা বিভিন্ন সময়কালের RSI-এর মধ্যে পার্থক্য বিশ্লেষণ করে ট্রেডারদের জন্য বাজারের আরও সূক্ষ্ম বিশ্লেষণ পদ্ধতি প্রদান করে। যদিও এই কৌশলটিতে কিছু সম্ভাব্য ঝুঁকি রয়েছে, তবে উপযুক্ত অপ্টিমাইজেশন এবং উন্নতির মাধ্যমে আমরা এই কৌশলটির কর্মক্ষমতা আরও বাড়িয়ে তুলতে পারি, এটিকে আরও নির্ভরযোগ্য এবং কার্যকর ট্রেডিং সরঞ্জামে পরিণত করতে পারি।

/*backtest

start: 2023-05-09 00:00:00

end: 2024-05-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy stands out by using two distinct RSI lengths, analyzing the differential between these to make precise trading decisions. - 1