আরএসআই ট্রেন্ড স্ট্র্যাটেজি

1

Follow

1802

Followers

সংক্ষিপ্ত বিবরণ

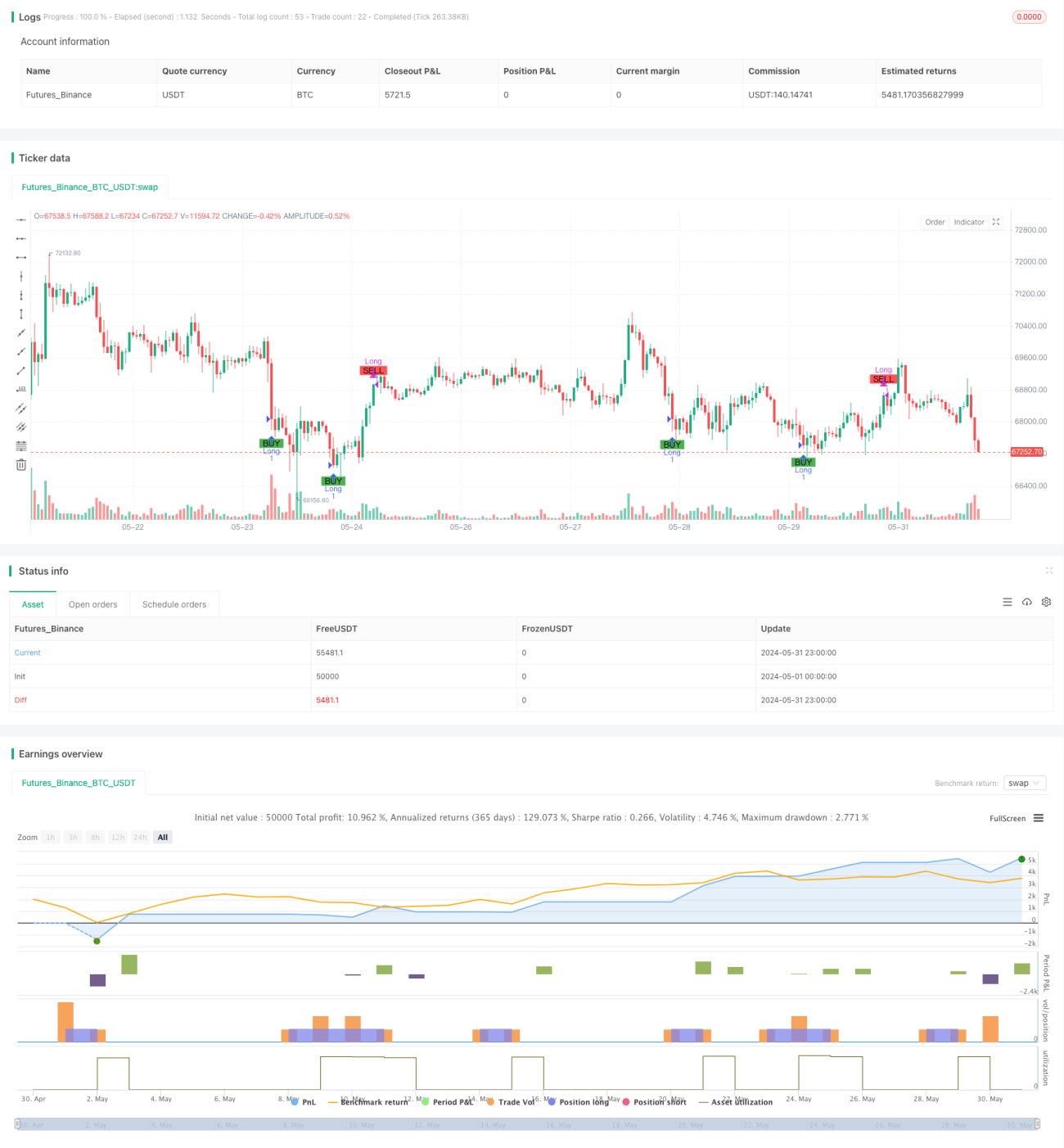

এই কৌশলটি রিলেটিভ স্ট্রেংথ ইনডেক্স (RSI) নির্দেশকের উপর ভিত্তি করে তৈরি। এটি RSI নির্দেশকের মান পূর্বনির্ধারিত উপরের ও নিচের থ্রেশহোল্ড অতিক্রম করেছে কিনা তা বিচার করে ক্রয় ও বিক্রয় সংকেত নির্ধারণ করে। একইসাথে, এই কৌশলে ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস এবং পজিশন হোল্ডিং সময়ের সীমা নির্ধারণ করা হয়েছে।

কৌশলের নীতি

- RSI নির্দেশকের মান গণনা করা।

- যখন RSI মান পূর্বনির্ধারিত ক্রয় থ্রেশহোল্ডের নিচে যায়, তখন ক্রয় সংকেত তৈরি হয়; যখন RSI মান পূর্বনির্ধারিত বিক্রয় থ্রেশহোল্ডের উপরে যায়, তখন বিক্রয় সংকেত তৈরি হয়।

- ক্রয় সংকেত অনুযায়ী, বর্তমান ক্লোজিং মূল্যের ভিত্তিতে ক্রয় পরিমাণ গণনা করে অর্ডার দেওয়া হয়।

- যদি স্টপ-লস অনুপাত নির্ধারণ করা থাকে, তাহলে স্টপ-লস মূল্য গণনা করে অর্ডার দেওয়া হয়।

- বিক্রয় সংকেত বা স্টপ-লস শর্ত অনুযায়ী, সমস্ত পজিশন বন্ধ করা হয়।

- যদি সর্বোচ্চ হোল্ডিং সময় নির্ধারণ করা থাকে, তাহলে হোল্ডিং সময় সর্বোচ্চ সময় অতিক্রম করলে, লাভ বা ক্ষতি নির্বিশেষে, সমস্ত পজিশন বন্ধ করা হয়।

কৌশলের সুবিধা

- RSI নির্দেশক একটি ব্যাপকভাবে ব্যবহৃত প্রযুক্তিগত বিশ্লেষণ নির্দেশক, যা বাজারের ওভারবট এবং ওভারসল্ড সংকেত কার্যকরভাবে সনাক্ত করতে পারে।

- এই কৌশলটি স্টপ-লস এবং পজিশন হোল্ডিং সময়ের সীমা যুক্ত করে, যা ঝুঁকি নিয়ন্ত্রণে সহায়তা করে।

- কৌশলের যুক্তি পরিষ্কার, বোঝা এবং বাস্তবায়ন করা সহজ।

- RSI-এর প্যারামিটার এবং থ্রেশহোল্ড সমন্বয় করে, বিভিন্ন বাজার পরিবেশের সাথে খাপ খাওয়ানো যায়।

কৌশলের ঝুঁকি

- কিছু ক্ষেত্রে RSI নির্দেশক ভুল সংকেত দিতে পারে, যার ফলে কৌশলে ক্ষতি হতে পারে।

- এই কৌশলটি ট্রেডিং সম্পদের মৌলিক বিষয়গুলি বিবেচনা করে না, শুধুমাত্র প্রযুক্তিগত নির্দেশকের উপর নির্ভর করে, তাই বাজারের অপ্রত্যাশিত ঘটনার সম্মুখীন হতে পারে।

- নির্দিষ্ট স্টপ-লস অনুপাত বাজারের অস্থিরতার পরিবর্তনের সাথে মানিয়ে নিতে পারবে না।

- কৌশলের কর্মক্ষমতা প্যারামিটার সেটিংয়ের দ্বারা প্রভাবিত হতে পারে; অনুপযুক্ত প্যারামিটারের কারণে কৌশলের কর্মক্ষমতা খারাপ হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- কৌশলের নির্ভরযোগ্যতা বাড়ানোর জন্য অন্যান্য প্রযুক্তিগত নির্দেশক, যেমন মুভিং এভারেজ, যুক্ত করা।

- স্টপ-লস কৌশল অপ্টিমাইজ করা, যেমন মুভিং স্টপ-লস বা ভোলাটিলিটি-ভিত্তিক ডায়নামিক স্টপ-লস ব্যবহার করা।

- বাজার পরিস্থিতি অনুযায়ী RSI-এর প্যারামিটার এবং থ্রেশহোল্ড গতিশীলভাবে সামঞ্জস্য করা।

- কৌশলের ঝুঁকি নিয়ন্ত্রণ ক্ষমতা উন্নত করতে ট্রেডিং সম্পদের মৌলিক বিশ্লেষণের সাথে একত্রিত করা।

- সর্বোত্তম প্যারামিটার সমন্বয় খুঁজে পেতে কৌশলের ব্যাকটেস্টিং এবং প্যারামিটার অপ্টিমাইজেশন করা।

উপসংহার

এই কৌশলটি RSI নির্দেশক ব্যবহার করে বাজারের ওভারবট এবং ওভারসল্ড সংকেত সনাক্ত করে, একইসাথে ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস এবং পজিশন হোল্ডিং সময়ের সীমা যুক্ত করে। কৌশলের যুক্তি সহজ এবং স্পষ্ট, বাস্তবায়ন ও অপ্টিমাইজ করা সহজ। তবে, কৌশলের কর্মক্ষমতা বাজারের অস্থিরতা এবং প্যারামিটার সেটিংয়ের দ্বারা প্রভাবিত হতে পারে, তাই কৌশলের দৃঢ়তা এবং লাভক্ষমতা বাড়ানোর জন্য অন্যান্য বিশ্লেষণ পদ্ধতি এবং ঝুঁকি ব্যবস্থাপনার উপায় একত্রিত করা প্রয়োজন।

Source

Pine

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Simple RSI Strategy", overlay=true, initial_capital=20, commission_value=0.1, commission_type=strategy.commission.percent)

// Define the hardcoded date (Year, Month, Day, Hour, Minute)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1