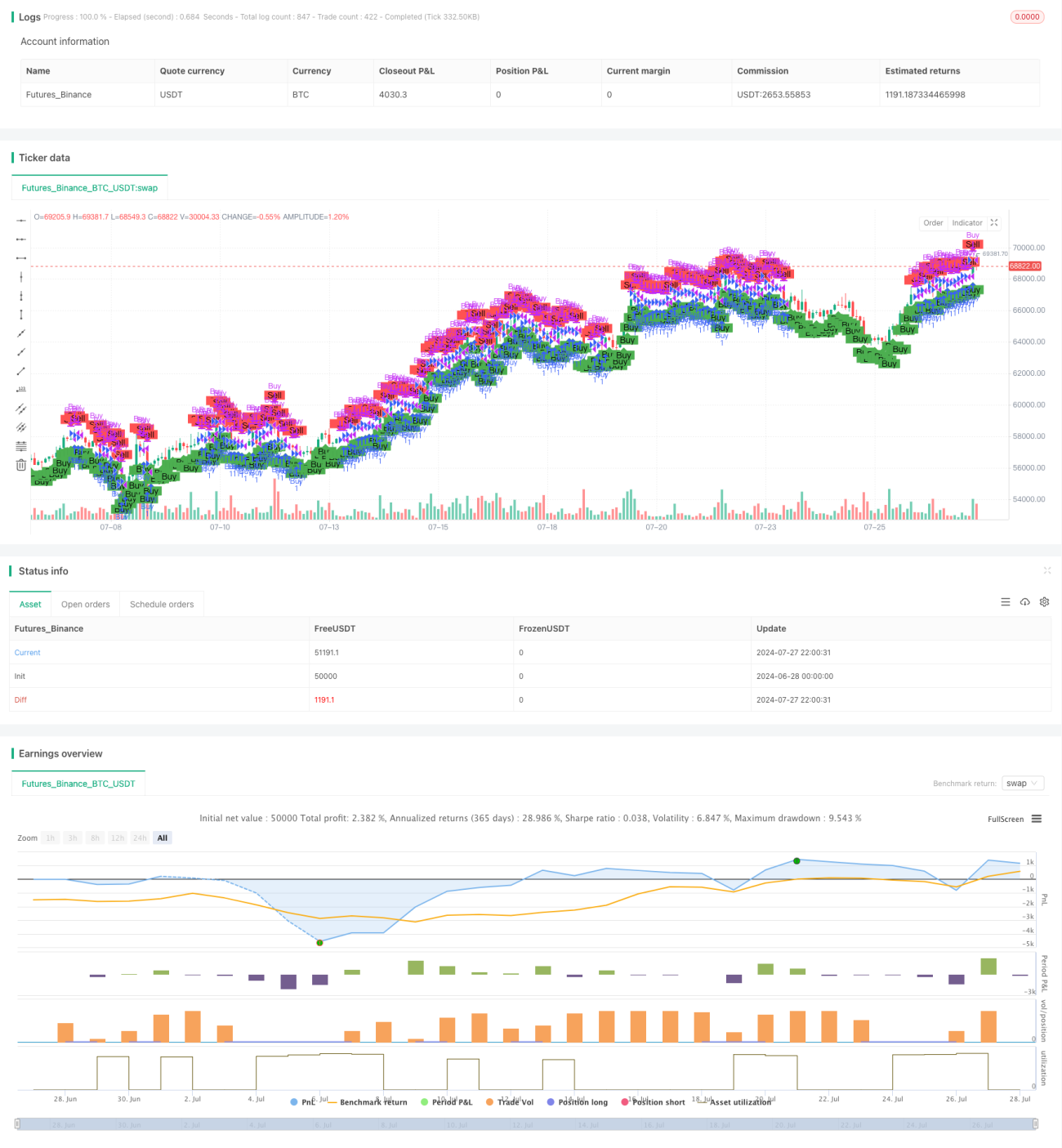

তিন পর্যায়ের উচ্চ-নিম্ন বিন্দু মোমেন্টাম ট্রেডিং কৌশল

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি ত্রি-কালীন উচ্চ-নিম্ন বিন্দুভিত্তিক মোমেন্টাম ট্রেডিং কৌশল। এটি সাম্প্রতিক তিন সপ্তাহের মূল্য ডেটা ব্যবহার করে সম্ভাব্য ক্রয় ও বিক্রয়ের সুযোগ সনাক্ত করে। কৌশলটি মূলত সর্বশেষ উচ্চ বিন্দু, সর্বশেষ ক্লোজিং মূল্য এবং তিন সপ্তাহ আগের ক্লোজিং মূল্যের মধ্যে সম্পর্কের ওপর ফোকাস করে এবং এই মূল্য স্তরগুলির তুলনা করে ট্রেডিং সিগন্যাল তৈরি করে। এই পদ্ধতির লক্ষ্য হল মধ্যমেয়াদী মূল্য ধারা ধরা, পাশাপাশি স্বল্পমেয়াদী বাজারের গোলমালের প্রভাব এড়ানো।

কৌশলের মূলনীতি

কৌশলের মূলনীতিতে নিম্নলিখিত গুরুত্বপূর্ণ উপাদানগুলি অন্তর্ভুক্ত রয়েছে:

-

সূচক গণনা:

- সর্বশেষ উচ্চ বিন্দু: ta.highest() ফাংশন ব্যবহার করে শেষ ৩০ ট্রেডিং দিনের (প্রায় ৪ সপ্তাহ) সর্বোচ্চ মূল্য গণনা করা।

- সর্বশেষ ক্লোজিং মূল্য: close[1] ব্যবহার করে আগের দিনের ক্লোজিং মূল্য পাওয়া।

- তিন সপ্তাহ আগের ক্লোজিং মূল্য: close[30] ব্যবহার করে ৩০ ট্রেডিং দিন আগের ক্লোজিং মূল্য পাওয়া।

-

ক্রয়ের শর্ত:

- শর্ত ১: সর্বশেষ উচ্চ বিন্দু তিন সপ্তাহ আগের ক্লোজিং মূল্যের চেয়ে বড় বা সমান।

- শর্ত ২: সর্বশেষ ক্লোজিং মূল্য তিন সপ্তাহ আগের ক্লোজিং মূল্যের চেয়ে বড়।

-

বিক্রয়ের শর্ত:

- যখন সর্বশেষ ক্লোজিং মূল্য তিন সপ্তাহ আগের ক্লোজিং মূল্যের চেয়ে বড় হয়, তখন বিক্রয় সিগন্যাল ট্রিগার হয়।

-

ট্রেড সম্পাদন:

- ক্রয় সিগন্যাল ট্রিগার হলে, লং পজিশনে প্রবেশ করা হয়।

- বিক্রয় সিগন্যাল ট্রিগার হলে, বর্তমান লং পজিশন বন্ধ করা হয়।

-

ভিজুয়ালাইজেশন:

- plotshape() ফাংশন ব্যবহার করে চার্টে ক্রয় ও বিক্রয় সিগন্যাল চিহ্নিত করা হয়।

এই নকশার লক্ষ্য হল মূল্য যখন তিন সপ্তাহ আগের স্তর ভেঙে উপরের দিকে যায় তখন উত্থান মোমেন্টাম ধরা, এবং মূল্য নিচে নেমে গেলে মুনাফা রক্ষার জন্য সময়মতো পজিশন বন্ধ করা।

কৌশলের সুবিধা

-

মধ্যমেয়াদী ধারা ধরা: বর্তমান মূল্যের সাথে তিন সপ্তাহ আগের মূল্য স্তরের তুলনা করে কৌশলটি কার্যকরভাবে মধ্যমেয়াদী ধারার গঠন ও ধারাবাহিকতা সনাক্ত করতে পারে।

-

গোলমাল ফিল্টারিং: তিন-সপ্তাহের সময় কাঠামো ব্যবহার করে স্বল্পমেয়াদী বাজারের ওঠানামা ফিল্টার করতে সাহায্য করে, যার ফলে সিগন্যালের নির্ভরযোগ্যতা বাড়ে।

-

গতিশীল অভিযোজন: কৌশলটি সর্বশেষ মূল্য ডেটার ভিত্তিতে তার সিদ্ধান্তের মানদণ্ড ক্রমাগত আপডেট করে, ফলে বাজারের পরিবর্তনের সাথে গতিশীলভাবে খাপ খাইয়ে নিতে পারে।

-

ঝুঁকি ব্যবস্থাপনা: স্পষ্ট বিক্রয়ের শর্ত নির্ধারণ করে, বাজার ঘুরে গেলে সময়মতো পজিশন বন্ধ করতে পারে, যা কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করে।

-

সহজবোধ্য: কৌশলের যুক্তি সহজ ও বোধগম্য, যা নতুন এবং অভিজ্ঞ ট্রেডার উভয়ের জন্যই সহজে বাস্তবায়নযোগ্য।

-

ভিজুয়াল সাপোর্ট: চার্টে ক্রয়-বিক্রয় সিগন্যাল স্পষ্টভাবে চিহ্নিত করা হয়, যা ট্রেডারদের সহজে বিচার ও ব্যাকটেস্ট বিশ্লেষণ করতে সাহায্য করে।

কৌশলের ঝুঁকি

-

মিথ্যা ব্রেকআউট ঝুঁকি: পার্শ্ববর্তী বাজারে ঘন ঘন মিথ্যা ব্রেকআউট হতে পারে, যার ফলে অতিরিক্ত ট্রেড ও অপ্রয়োজনীয় কমিশন ক্ষতি হতে পারে।

-

পিছিয়ে পড়া: তিন সপ্তাহের ঐতিহাসিক ডেটা ব্যবহার করায় সিগন্যালে পিছিয়ে পড়া দেখা দিতে পারে, দ্রুত পরিবর্তনশীল বাজারে সেরা প্রবেশের সুযোগ হাতছাড়া হতে পারে।

-

একক সময় কাঠামোর সীমাবদ্ধতা: শুধুমাত্র তিন সপ্তাহের ডেটার ওপর নির্ভর করলে অন্যান্য সময় কাঠামোর গুরুত্বপূর্ণ বাজার তথ্য উপেক্ষিত হতে পারে।

-

স্টপ-লস ব্যবস্থার অভাব: বর্তমান কৌশলে স্পষ্ট স্টপ-লস ব্যবস্থা নেই, ফলে বাজারের তীব্র ওঠানামায় বড় ক্ষতির সম্মুখীন হতে পারে।

-

ক্লোজিং মূল্যের ওপর অতিরিক্ত নির্ভরতা: কৌশলটি মূলত ক্লোজিং মূল্যের ওপর ভিত্তি করে সিদ্ধান্ত নেয়, যার ফলে ট্রেডিং সেশনের গুরুত্বপূর্ণ মূল্য পরিবর্তন উপেক্ষিত হতে পারে।

-

ভলিউম নিশ্চিতকরণের অভাব: ভলিউম ফ্যাক্টর বিবেচনা না করায় কম ভলিউমের সময়ে মিথ্যা সিগন্যাল তৈরি হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

বহু-সময় কাঠামো বিশ্লেষণ: ডে, উইক ও মান্থলি চার্টের মতো একাধিক সময় কাঠামোর ডেটা একীভূত করে আরও বিস্তৃত বাজার দৃষ্টিভঙ্গি প্রদান করা।

-

ভলিউম সূচক অন্তর্ভুক্তি: ভলিউম বিশ্লেষণের সাথে মিলিয়ে সিগন্যালের নির্ভরযোগ্যতা বাড়ানো সম্ভব, বিশেষ করে ব্রেকআউট নিশ্চিতকরণের ক্ষেত্রে।

-

গতিশীল স্টপ-লস ব্যবস্থা: ট্রেইলিং স্টপ বা ATR-ভিত্তিক স্টপের মতো অভিযোজিত স্টপ-লস কৌশল বাস্তবায়ন করে ভালো ঝুঁকি ব্যবস্থাপনা নিশ্চিত করা।

-

সিগন্যাল ফিল্টার: RSI বা MACD-এর মতো অতিরিক্ত টেকনিক্যাল ইন্ডিকেটর বা বাজারের অনুভূতি নির্দেশক যোগ করে মিথ্যা সিগন্যাল কমানো।

-

প্রবেশ অপ্টিমাইজেশন: সরাসরি মার্কেট অর্ডারের পরিবর্তে লিমিট অর্ডার বা পর্যবেক্ষণ অঞ্চল ব্যবহার করে ভালো মূল্যে প্রবেশের চেষ্টা করা।

-

পজিশন ম্যানেজমেন্ট: বাজারের অস্থিরতা ও অ্যাকাউন্টের ঝুঁকির ভিত্তিতে প্রতিটি ট্রেডের পজিশন সাইজ সমন্বয় করে গতিশীল পজিশন ম্যানেজমেন্ট কৌশল বাস্তবায়ন করা।

-

বাজার অবস্থা সনাক্তকরণ: বাজারের অবস্থা (ট্রেন্ড, রেঞ্জ, উচ্চ অস্থিরতা) সনাক্ত করার লজিক যুক্ত করে বিভিন্ন বাজার পরিবেশে ভিন্ন ট্রেডিং প্যারামিটার ব্যবহার করা।

-

ব্যাকটেস্ট ও অপ্টিমাইজেশন: ব্যাপক ঐতিহাসিক ডেটা ব্যাকটেস্ট করে সময়কাল, শর্তের থ্রেশহোল্ড ইত্যাদি প্যারামিটার অপ্টিমাইজ করা।

সারসংক্ষেপ

ত্রি-কালীন উচ্চ-নিম্ন বিন্দু মোমেন্টাম ট্রেডিং কৌশল একটি সহজ ও কার্যকর মধ্যমেয়াদী ট্রেন্ড ফলোয়িং পদ্ধতি। সর্বশেষ উচ্চ বিন্দু, সর্বশেষ ক্লোজিং মূল্য ও তিন সপ্তাহ আগের ক্লোজিং মূল্যের তুলনা করে কৌশলটি মূল্য ব্রেকআউট ও মোমেন্টাম পরিবর্তন ধরে। এর সুবিধা হলো স্বল্পমেয়াদী গোলমাল ফিল্টার করা, মধ্যমেয়াদী ধারা ধরা এবং যুক্তি সহজবোধ্য। তবে, কৌশলটি মিথ্যা ব্রেকআউট, সিগন্যালে পিছিয়ে পড়া ও অপর্যাপ্ত ঝুঁকি ব্যবস্থাপনার চ্যালেঞ্জের মুখোমুখি।

ভবিষ্যতের অপ্টিমাইজেশনের দিকনির্দেশনা বহু-সময় কাঠামো বিশ্লেষণ, ভলিউম নিশ্চিতকরণ, গতিশীল ঝুঁকি ব্যবস্থাপনা ও বাজার অবস্থা সনাক্তকরণের দিকে নজর দেওয়া উচিত। এই উন্নতির মাধ্যমে কৌশলটি বিভিন্ন বাজার পরিবেশে আরও স্থিতিশীল পারফর্ম করবে এবং ট্রেডারদের জন্য আরও নির্ভরযোগ্য সিদ্ধান্ত সহায়তা প্রদান করবে।

সামগ্রিকভাবে, এই কৌশলটি কোয়ান্টিটেটিভ ট্রেডিংয়ের জন্য একটি ভালো সূচনা পয়েন্ট প্রদান করে। ক্রমাগত অপ্টিমাইজেশন ও পরিমার্জনের মাধ্যমে এটি একটি শক্তিশালী ট্রেডিং টুলে পরিণত হওয়ার সম্ভাবনা রাখে। তবে, বিনিয়োগকারীদের বাস্তব প্রয়োগে সতর্ক থাকা উচিত, বাজারের ঝুঁকি সম্পূর্ণভাবে বুঝতে হবে এবং নিজের ঝুঁকি সহনশীলতা ও বিনিয়োগ লক্ষ্যের সাথে সঙ্গতি রেখে কৌশলটি ব্যবহার করতে হবে।

৪. ঝুঁকি ব্যবস্থাপনা: স্পষ্ট বিক্রয় শর্তের মাধ্যমে, বাজার ঘুরে গেলে কৌশলটি তাৎক্ষণিকভাবে পজিশন বন্ধ করতে পারে, কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করে।

৫. সহজ ও বোধগম্য: কৌশলটির যুক্তি স্বজ্ঞাত, সহজে বোঝা ও বাস্তবায়ন করা যায়, যা নবীন ও অভিজ্ঞ উভয় প্রকার ব্যবসায়ীর জন্যই উপযুক্ত।

৬. ভিজ্যুয়াল সহায়তা: চার্টে ক্রয় ও বিক্রয় সংকেত স্পষ্টভাবে চিহ্নিত করা থাকে, যা ব্যবসায়ীদের স্বজ্ঞাত বিচার ও ব্যাকটেস্টিং বিশ্লেষণে সুবিধা দেয়।

কৌশলের ঝুঁকি

১. মিথ্যা ব্রেকআউট ঝুঁকি: সাইডওয়ে বাজারে ঘন ঘন মিথ্যা ব্রেকআউট ঘটতে পারে, যা অতিরিক্ত ট্রেডিং এবং অপ্রয়োজনীয় লেনদেন ফি ক্ষতির কারণ হয়।

২. পিছিয়ে থাকা প্রকৃতি: তিন সপ্তাহের ঐতিহাসিক তথ্য ব্যবহার করায় সংকেত পিছিয়ে যেতে পারে, দ্রুত পরিবর্তনশীল বাজারে সর্বোত্তম প্রবেশ বিন্দু মিস হতে পারে।

৩. একক টাইমফ্রেম সীমাবদ্ধতা: শুধুমাত্র তিন সপ্তাহের তথ্যের ওপর নির্ভর করায় অন্যান্য টাইমফ্রেমের গুরুত্বপূর্ণ বাজার তথ্য উপেক্ষিত হতে পারে।

৪. স্টপ-লস প্রক্রিয়ার অভাব: বর্তমান কৌশলে স্পষ্ট স্টপ-লস প্রক্রিয়া নেই, যা তীব্র বাজার ওঠানামার সময় বড় ক্ষতির সম্মুখীন হতে পারে।

৫. ক্লোজিং প্রাইসের ওপর অতিরিক্ত নির্ভরতা: কৌশলটি মূলত ক্লোজিং প্রাইসের ওপর ভিত্তি করে বিচার করে, যা গুরুত্বপূর্ণ ইন্ট্রাডে মূল্য আন্দোলন উপেক্ষা করতে পারে।

৬. ভলিউম নিশ্চিতকরণের অভাব: ভলিউম ফ্যাক্টর বিবেচনা না করায় কম ট্রেডিং ভলিউমের সময় মিথ্যা সংকেত তৈরি হতে পারে।

কৌশল অপ্টিমাইজেশন নির্দেশনা

১. মাল্টি-টাইমফ্রেম বিশ্লেষণ: দৈনিক, সাপ্তাহিক ও মাসিকের মতো একাধিক টাইমফ্রেমের তথ্য একীভূত করে আরও ব্যাপক বাজার দৃষ্টিভঙ্গি প্রদান করা।

২. ভলিউম নির্দেশক অন্তর্ভুক্তি: ভলিউম বিশ্লেষণ যুক্ত করলে সংকেত নির্ভরযোগ্যতা বৃদ্ধি পায়, বিশেষ করে ব্রেকআউট নিশ্চিতকরণে।

৩. গতিশীল স্টপ-লস প্রক্রিয়া: ট্রেইলিং স্টপ বা এটিআর-ভিত্তিক স্টপের মতো অভিযোজিত স্টপ-লস কৌশল বাস্তবায়ন করে উন্নত ঝুঁকি ব্যবস্থাপনা করা।

৪. সংকেত ফিল্টার: আরএসআই বা ম্যাকডি-র মতো অতিরিক্ত প্রযুক্তিগত বা বাজার অনুভূতি নির্দেশক যোগ করে মিথ্যা সংকেত কমানো।

৫. এন্ট্রি অপ্টিমাইজেশন: সরাসরি মার্কেট অর্ডারের পরিবর্তে লিমিট অর্ডার বা পর্যবেক্ষণ জোন ব্যবহার করে ভালো এক্সিকিউশন মূল্য পাওয়া।

৬. পজিশন ম্যানেজমেন্ট: বাজারের অস্থিরতা ও অ্যাকাউন্ট ঝুঁকির ভিত্তিতে প্রতিটি ট্রেডের আকার সামঞ্জস্য করে গতিশীল পজিশন সাইজিং কৌশল বাস্তবায়ন করা।

৭. বাজার অবস্থা চিহ্নিতকরণ: বাজারের অবস্থা (ট্রেন্ডিং, রেঞ্জিং, উচ্চ অস্থিরতা) চিহ্নিত করার যুক্তি যোগ করে এবং বিভিন্ন বাজার পরিবেশের জন্য ভিন্ন ট্রেডিং প্যারামিটার গ্রহণ করা।

৮. ব্যাকটেস্টিং ও অপ্টিমাইজেশন: ব্যাপক ঐতিহাসিক ডেটা ব্যাকটেস্টিং পরিচালনা করে সময়কাল ও শর্ত সীমার মতো কৌশল প্যারামিটার অপ্টিমাইজ করা।

সারসংক্ষেপ

থ্রি-উইক হাই-লো মোমেন্টাম ট্রেডিং কৌশলটি মধ্যমেয়াদী ট্রেন্ড অনুসরণের জন্য একটি সহজ কিন্তু কার্যকর পদ্ধতি। সর্বশেষ উচ্চ, সর্বশেষ ক্লোজ এবং তিন সপ্তাহ আগের ক্লোজিং প্রাইসের তুলনা করে কৌশলটি মূল্য ব্রেকআউট ও মোমেন্টাম পরিবর্তন ধরতে পারে। এর শক্তি হলো স্বল্পমেয়াদী শব্দ ফিল্টার করা, মধ্যমেয়াদী ট্রেন্ড ধরা এবং সহজ, বোধগম্য যুক্তি। তবে কৌশলটি মিথ্যা ব্রেকআউট, সংকেত পিছিয়ে যাওয়া এবং অপর্যাপ্ত ঝুঁকি ব্যবস্থাপনার মতো চ্যালেঞ্জেরও সম্মুখীন।

ভবিষ্যত অপ্টিমাইজেশন নির্দেশনাগুলি মাল্টি-টাইমফ্রেম বিশ্লেষণ, ভলিউম নিশ্চিতকরণ, গতিশীল ঝুঁকি ব্যবস্থাপনা এবং বাজার অবস্থা চিহ্নিতকরণের ওপর কেন্দ্রীভূত হওয়া উচিত। এই উন্নতিগুলির মাধ্যমে কৌশলটি বিভিন্ন বাজার পরিবেশে আরও শক্তিশালী পারফরম্যান্স দেখানোর সম্ভাবনা রাখে, যা ব্যবসায়ীদের আরও নির্ভরযোগ্য সিদ্ধান্ত সহায়তা প্রদান করে।

সামগ্রিকভাবে, এই কৌশলটি কোয়ান্টিটেটিভ ট্রেডিংয়ের জন্য একটি ভালো শুরুর বিন্দু প্রদান করে। ক্রমাগত অপ্টিমাইজেশন ও পরিশোধন সহ এটি একটি শক্তিশালী ট্রেডিং টুল হয়ে উঠতে পারে। তবে বিনিয়োগকারীদের বাস্তবে প্রয়োগের সময় সতর্ক হওয়া উচিত, বাজারের ঝুঁকি সম্পূর্ণরূপে উপলব্ধি করে এবং নিজস্ব ঝুঁকি সহনশীলতা ও বিনিয়োগ উদ্দেশ্যের সাথে কৌশলটি ব্যবহার করা উচিত।

- 1