**উচ্চতর এক্সপোনেনশিয়াল মুভিং এভারেজ মোমেন্টাম ট্রেন্ড ট্রেডিং কৌশল**

সারসংক্ষেপ

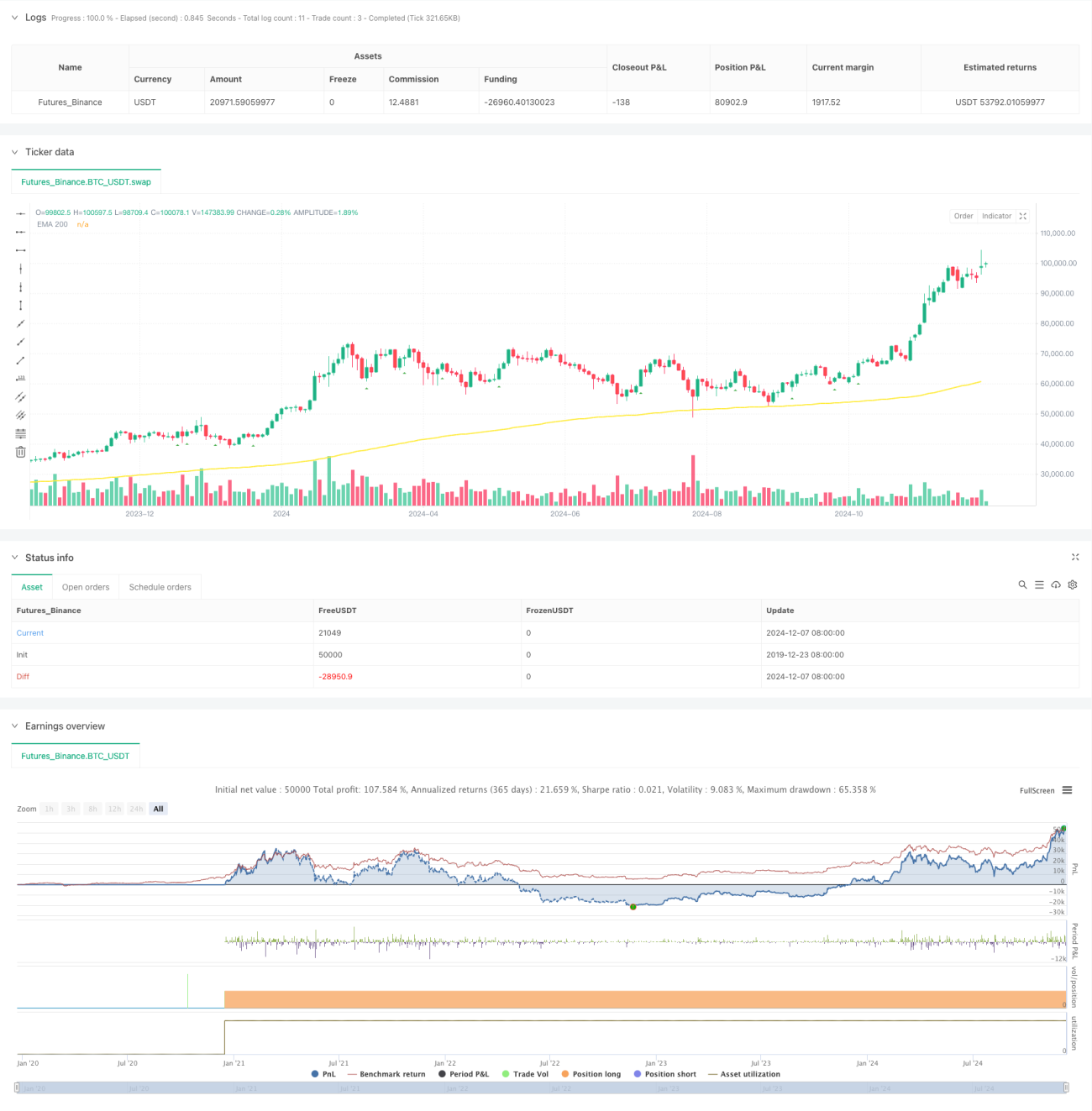

এই কৌশলটি একটি ট্রেন্ড ফলোয়িং কৌশল যা এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA) এবং মোমেন্টাম সূচকের উপর ভিত্তি করে তৈরি। এটি মোমেন্টাম ব্রেকআউট সিগন্যাল এবং EMA ট্রেন্ড ফিল্টারের সমন্বয় ব্যবহার করে, বাজারের স্পষ্ট ট্রেন্ড থাকাকালীন ট্রেড করে। কৌশলটিতে একটি সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা মডিউল, নমনীয় ট্রেডিং সময় ফিল্টার এবং বিস্তারিত পরিসংখ্যানগত বিশ্লেষণ ফিচার রয়েছে, যা কৌশলের স্থিতিশীলতা ও নির্ভরযোগ্যতা বাড়ায়।

কৌশলের নীতি

কৌশলের মূল লজিক নিম্নলিখিত মূল উপাদানগুলির উপর ভিত্তি করে তৈরি:

- মোমেন্টাম সিগন্যাল সনাক্তকরণ: ব্যবহারকারী নির্ধারিত সময়সীমার মধ্যে মোমেন্টাম মান গণনা করে। যখন মোমেন্টাম ঊর্ধ্বমুখী থ্রেশহোল্ড ভেঙে যায়, তখন লং সিগন্যাল তৈরি হয় এবং যখন এটি নিম্নমুখী থ্রেশহোল্ড ভেঙে যায়, তখন শর্ট সিগন্যাল তৈরি হয়।

- EMA ট্রেন্ড ফিল্টার: ট্রেন্ড নির্ধারণের জন্য ২০০-পিরিয়ড EMA ব্যবহার করা হয়। দাম EMA-এর উপরে থাকলে লং করার অনুমতি দেওয়া হয় এবং দাম EMA-এর নিচে থাকলে শর্ট করার অনুমতি দেওয়া হয়।

- সময় ফিল্টার: নির্দিষ্ট ট্রেডিং সেশন নির্ধারণ করা যায় এবং GMT টাইমজোন সমন্বয় সমর্থিত, যা কৌশলটিকে বিভিন্ন বাজারের ট্রেডিং সময়ের সাথে খাপ খাইয়ে নিতে সাহায্য করে।

- ঝুঁকি নিয়ন্ত্রণ: ATR বা নির্দিষ্ট শতাংশের উপর ভিত্তি করে স্টপ লস ও টার্গেট প্রফিট সেটিং সমর্থন করে এবং দৈনিক সর্বোচ্চ ট্রেড সংখ্যা সীমিত করে।

কৌশলের সুবিধা

- শক্তিশালী ট্রেন্ড ফলোয়িং ক্ষমতা: EMA এবং মোমেন্টামের দ্বৈত নিশ্চিতকরণের মাধ্যমে কার্যকরভাবে মূল ট্রেন্ড মুভমেন্ট ক্যাপচার করা যায়।

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: একাধিক স্টপ লস বিকল্প প্রদান করে, যার মধ্যে ATR ভিত্তিক ডায়নামিক স্টপ লস এবং নির্দিষ্ট শতাংশ স্টপ লস উভয়ই ব্যবহার করা যায়।

- ব্যাপক পরিসংখ্যানগত বিশ্লেষণ: লং/শার্ট জয় রেট, রিস্ক-রিওয়ার্ড রেশিও ইত্যাদি সহ একাধিক পারফরম্যান্স মেট্রিক রিয়েল-টাইমে ট্র্যাক করে।

- নমনীয় এবং সামঞ্জস্যযোগ্য প্যারামিটার: প্রধান প্যারামিটারগুলি বিভিন্ন বাজারের বৈশিষ্ট্য অনুযায়ী অপ্টিমাইজ ও সমন্বয় করা যায়।

কৌশলের ঝুঁকি

-

রেঞ্জ-বাউন্ড মার্কেটের ঝুঁকি: পাশাপাশি চলা বাজারে ঘন ঘন মিথ্যা ব্রেকআউট সিগন্যাল তৈরি হতে পারে।

সম্ভাব্য সমাধান: অসিলেটর ফিল্টার যুক্ত করা বা ব্রেকআউট থ্রেশহোল্ড বাড়ানো। -

স্লিপেজ ঝুঁকি: অত্যন্ত অস্থির সময়ে বড় স্লিপেজের সম্মুখীন হতে পারে।

সম্ভাব্য সমাধান: যুক্তিসঙ্গত স্টপ লস রেঞ্জ নির্ধারণ করা এবং উচ্চ অস্থিরতার সময় ট্রেড না করা। -

অতিরিক্ত ট্রেডিং ঝুঁকি: সিগন্যাল খুব ঘন ঘন তৈরি হলে অতিরিক্ত ট্রেডিং হতে পারে।

সম্ভাব্য সমাধান: দৈনিক সর্বোচ্চ ট্রেড সংখ্যার সীমা যুক্তিসঙ্গতভাবে নির্ধারণ করা।

কৌশলের অপ্টিমাইজেশন দিকনির্দেশনা

- ডায়নামিক প্যারামিটার অপ্টিমাইজেশন: বাজারের অস্থিরতার উপর ভিত্তি করে মোমেন্টাম থ্রেশহোল্ড এবং EMA পিরিয়ড স্বয়ংক্রিয়ভাবে সামঞ্জস্য করা যায়।

- মাল্টি-টাইমফ্রেম বিশ্লেষণ: একাধিক টাইমফ্রেমের ট্রেন্ড নিশ্চিতকরণ যুক্ত করে সিগন্যালের নির্ভরযোগ্যতা বৃদ্ধি করা।

- মার্কেট এনভায়রনমেন্ট সনাক্তকরণ: অস্থিরতা বিশ্লেষণ মডিউল যুক্ত করে বিভিন্ন বাজার পরিবেশে ভিন্ন প্যারামিটার সেটিং ব্যবহার করা।

- সিগন্যাল শক্তি গ্রেডিং: ব্রেকআউট সিগন্যালের শক্তি অনুযায়ী গ্রেডিং করে এবং সিগন্যাল শক্তির উপর ভিত্তি করে পজিশনের আকার ডায়নামিকভাবে সামঞ্জস্য করা।

উপসংহার

এটি একটি ভালোভাবে ডিজাইন করা ট্রেন্ড ফলোয়িং কৌশল, যা মোমেন্টাম ব্রেকআউট এবং EMA ট্রেন্ডের সমন্বয়ের মাধ্যমে বাজারের সুযোগ ক্যাপচার করে। কৌশলটির ঝুঁকি ব্যবস্থাপনা সিস্টেম সম্পূর্ণ, পরিসংখ্যানগত বিশ্লেষণ ক্ষমতা শক্তিশালী এবং ভালো ব্যবহারিকতা ও সম্প্রসারণযোগ্যতা রয়েছে। ক্রমাগত অপ্টিমাইজেশন ও উন্নয়নের মাধ্যমে, এই কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল কর্মক্ষমতা প্রদর্শনের সম্ভাবনা রাখে।

- 1