সারসংক্ষেপ

এই কৌশলটি বুলিঞ্জার ব্যান্ড এবং ট্রিপল সুপারট্রেন্ড ইন্ডিকেটরের সমন্বয় ব্যবহার করে ট্রেডিং করে। বুলিঞ্জার ব্যান্ডের অস্থিরতা নির্ধারণ এবং ট্রিপল সুপারট্রেন্ডের ট্রেন্ড নিশ্চিতকরণের মাধ্যমে একটি শক্তিশালী ট্রেন্ড-ফলোয়িং সিস্টেম তৈরি হয়। বুলিঞ্জার ব্যান্ড দামের চরম অস্থিরতা চিহ্নিত করতে ব্যবহৃত হয়, অন্যদিকে ট্রিপল সুপারট্রেন্ড বিভিন্ন প্যারামিটার সেটিংসের মাধ্যমে ট্রেন্ডের দিক নির্ধারণের বহুস্তর নিশ্চিতকরণ প্রদান করে। সমস্ত সিগন্যাল একমত হলেই ট্রেড করা হয়, যাতে ভুয়া সিগন্যালের ঝুঁকি কমানো যায়। এই সমন্বিত পদ্ধতি ট্রেন্ড-ফলোয়িংয়ের সুবিধা বজায় রেখে ট্রেডিংয়ের নির্ভরযোগ্যতা বাড়ায়।

কৌশলের মূলনীতি

কৌশলের মূল লজিকে নিম্নলিখিত গুরুত্বপূর্ণ অংশগুলি অন্তর্ভুক্ত রয়েছে:

- 20 পিরিয়ডের বুলিঞ্জার ব্যান্ড ব্যবহার করা হয়, স্ট্যান্ডার্ড ডেভিয়েশন গুণক 2.0, যা দামের অস্থিরতা নির্ধারণ করতে ব্যবহৃত হয়।

- তিনটি সুপারট্রেন্ড লাইন সেট করা হয়, পিরিয়ড 10 এবং প্যারামিটারগুলি যথাক্রমে 3.0, 4.0 এবং 5.0।

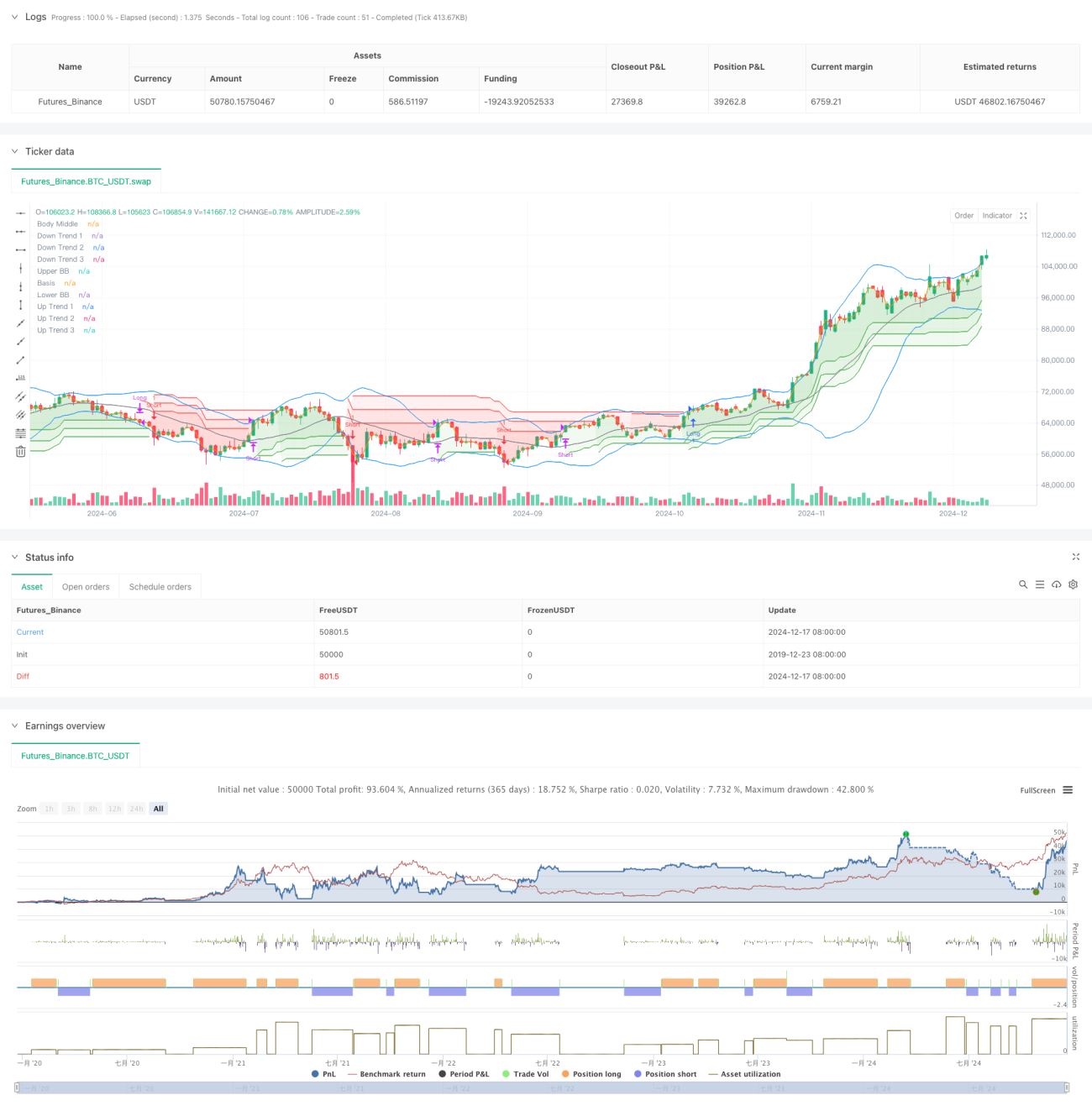

- লং এন্ট্রি শর্ত: দাম বুলিঞ্জার ব্যান্ডের উপরের রেখা ভেঙে যায় এবং তিনটি সুপারট্রেন্ড লাইনই ঊর্ধ্বমুখী ট্রেন্ড দেখায়।

- শর্ট এন্ট্রি শর্ত: দাম বুলিঞ্জার ব্যান্ডের নিচের রেখা ভেঙে পড়ে এবং তিনটি সুপারট্রেন্ড লাইনই নিম্নমুখী ট্রেন্ড দেখায়।

- যেকোনো একটি সুপারট্রেন্ড লাইনের দিক পরিবর্তন করলে, বর্তমান পজিশন বন্ধ করা হয়।

- মধ্যম দামের রেখা ভিজুয়াল বর্ধনের জন্য রেফারেন্স হিসেবে ব্যবহার করা হয়।

কৌশলের সুবিধা

- বহুস্তর নিশ্চিতকরণ প্রক্রিয়া: বুলিঞ্জার ব্যান্ড এবং ট্রিপল সুপারট্রেন্ডের সমন্বয় ভুয়া সিগন্যাল অনেকাংশে কমিয়ে দেয়।

- শক্তিশালী ট্রেন্ড অনুসরণ: সুপারট্রেন্ড ইন্ডিকেটরের ধাপে ধাপে প্যারামিটার সেটিং বিভিন্ন স্তরের ট্রেন্ড কার্যকরভাবে ধরতে সক্ষম।

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: ট্রেন্ডে পরিবর্তনের ইঙ্গিত পেলেই দ্রুত পজিশন বন্ধ করে, ড্রডাউন নিয়ন্ত্রণ করে।

- উচ্চ প্যারামিটার সামঞ্জস্যতা: বিভিন্ন বাজারের বৈশিষ্ট্য অনুযায়ী প্রতিটি ইন্ডিকেটরের প্যারামিটার অপটিমাইজ করা যায়।

- উচ্চ অটোমেশন: কৌশলের লজিক স্পষ্ট, যা সিস্টেমেটিক বাস্তবায়নের জন্য সহজ।

কৌশলের ঝুঁকি

- সাইডওয়ে মার্কেটের ঝুঁকি: পাশাপাশি চলমান বাজারে ঘন ঘন ভুয়া ব্রেকআউট সিগন্যাল হতে পারে।

- স্লিপেজের প্রভাব: তীব্র অস্থিরতার সময়ে বড় স্লিপেজ ক্ষতির সম্মুখীন হতে পারে।

- বিলম্বের ঝুঁকি: বহুস্তর নিশ্চিতকরণ প্রক্রিয়ার কারণে এন্ট্রির সময় একটু দেরি হতে পারে।

- প্যারামিটার সংবেদনশীলতা: বিভিন্ন প্যারামিটার সংমিশ্রণের কারণে কৌশলের পারফরম্যান্সে বড় পার্থক্য দেখা দিতে পারে।

- বাজার পরিবেশের উপর নির্ভরশীলতা: স্পষ্ট ট্রেন্ডযুক্ত বাজারে কৌশলটি ভালো পারফর্ম করে।

কৌশল অপটিমাইজেশনের দিকনির্দেশনা

- ভলিউম ইন্ডিকেটর অন্তর্ভুক্ত করা: দামের ব্রেকআউটের বৈধতা নিশ্চিত করতে ট্রেডিং ভলিউম ব্যবহার করা।

- স্টপ-লস পদ্ধতি অপটিমাইজ করা: ট্রেইলিং স্টপ বা ATR-ভিত্তিক ডায়নামিক স্টপ যোগ করা।

- সময় ফিল্টার যোগ করা: নির্দিষ্ট সময়ে ট্রেডিং নিষিদ্ধ করা, অদক্ষ অস্থিরতা এড়াতে।

- অস্থিরতা ফিল্টার যোগ করা: অত্যধিক অস্থিরতার সময়ে পজিশন সাইজ সামঞ্জস্য করা বা ট্রেডিং বন্ধ রাখা।

- প্যারামিটার অ্যাডাপ্টিভ মেকানিজম তৈরি করা: বাজারের অবস্থা অনুযায়ী প্যারামিটার গতিশীলভাবে সমন্বয় করা।

সারসংক্ষেপ

এটি একটি ট্রেন্ড-ফলোয়িং কৌশল যা বুলিঞ্জার ব্যান্ড এবং ট্রিপল সুপারট্রেন্ডকে একত্রিত করে, একাধিক টেকনিক্যাল ইন্ডিকেটরের নিশ্চিতকরণের মাধ্যমে ট্রেডিংয়ের নির্ভরযোগ্যতা বাড়ায়। কৌশলটির ট্রেন্ড ধরার ক্ষমতা এবং ঝুঁকি নিয়ন্ত্রণ ক্ষমতা শক্তিশালী, তবে বাজার পরিবেশের প্রভাবের দিকেও নজর দিতে হবে। ক্রমাগত অপটিমাইজেশন এবং উন্নতির মাধ্যমে, কৌশলটি বিভিন্ন বাজার পরিস্থিতিতে স্থিতিশীল পারফরম্যান্স বজায় রাখতে সক্ষম হবে বলে আশা করা যায়। লাইভ ট্রেডিংয়ের আগে পর্যাপ্ত ব্যাকটেস্টিং এবং প্যারামিটার অপটিমাইজেশন করার পাশাপাশি বাজারের বাস্তব অবস্থার সাথে উপযুক্ত সমন্বয় করার পরামর্শ দেওয়া হচ্ছে।

//@version=5

strategy("Demo GPT - Bollinger + Triple Supertrend Combo", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// -------------------------------

// User Input for Date Range

// -------------------------------

startDate = input(title="Start Date", defval=timestamp("2018-01-01 00:00:00"))

endDate = input(title="End Date", defval=timestamp("2069-12-31 23:59:59"))

// -------------------------------

// Bollinger Band Inputs

// -------------------------------- 1