# গতিশীল ট্রেন্ড মোমেন্টাম অপটিমাইজেশন কৌশল জি চ্যানেল ইন্ডিকেটরের সাথে মিলিত

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি G-চ্যানেল, RSI এবং MACD সূচক সমন্বিত একটি উন্নত ট্রেন্ড ট্র্যাকিং ট্রেডিং সিস্টেম। এটি গতিশীলভাবে সমর্থন এবং প্রতিরোধ অঞ্চল গণনা করে, মোমেন্টাম ইন্ডিকেটরের সাথে মিলিয়ে উচ্চ সম্ভাবনার ট্রেডিং সুযোগ সনাক্ত করে। কৌশলটির মূল ভিত্তি হল কাস্টম G-চ্যানেল সূচক ব্যবহার করে বাজারের প্রবণতা নির্ধারণ করা, একইসাথে RSI এবং MACD ব্যবহার করে মোমেন্টাম পরিবর্তন নিশ্চিত করা, যা আরও নির্ভুল ট্রেডিং সিগন্যাল তৈরি করে।

কৌশল নীতি

কৌশলটি ট্রেডিং সিগন্যালের নির্ভরযোগ্যতা নিশ্চিত করতে ট্রিপল ফিল্টারিং মেকানিজম ব্যবহার করে। প্রথমত, G-চ্যানেল নির্দিষ্ট সময়সীমার মধ্যে সর্বোচ্চ এবং সর্বনিম্ন মূল্য গণনা করে গতিশীলভাবে সমর্থন এবং প্রতিরোধ অঞ্চল তৈরি করে। যখন দাম চ্যানেল ভেঙে ফেলে, তখন সিস্টেম সম্ভাব্য প্রবণতা পরিবর্তনের পয়েন্ট চিহ্নিত করে। দ্বিতীয়ত, RSI সূচক ব্যবহার করে বাজারটি অতিরিক্ত কেনা বা অতিরিক্ত বিক্রির অবস্থায় আছে কিনা তা নিশ্চিত করা হয়, যা আরও মূল্যবান ট্রেডিং সুযোগ নির্বাচনে সাহায্য করে। শেষত, MACD সূচক হিস্টোগ্রামের পজিটিভ এবং নেগেটিভ মানের মাধ্যমে মোমেন্টামের দিক এবং শক্তি নিশ্চিত করে। এই তিনটি শর্ত পূরণ হলেই সিস্টেম ট্রেডিং সিগন্যাল জারি করে।

কৌশল সুবিধা

- মাল্টি-ডাইমেনশনাল সিগন্যাল কনফার্মেশন মেকানিজম ট্রেডিংয়ের নির্ভুলতা উল্লেখযোগ্যভাবে বৃদ্ধি করে

- গতিশীল স্টপ-লস এবং টেক-প্রফিট সেটিং কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করে

- G-চ্যানেলের অভিযোজিত বৈশিষ্ট্য কৌশলটিকে বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে সাহায্য করে

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা সিস্টেম, যার মধ্যে পজিশন ম্যানেজমেন্ট এবং মানি ম্যানেজমেন্ট অন্তর্ভুক্ত

- ভিজুয়াল লেবেল সিস্টেম সরাসরি ট্রেডিং সিগন্যাল দেখায়, বিশ্লেষণ এবং অপ্টিমাইজেশন সহজ করে

কৌশল ঝুঁকি

- অস্থির বাজারে মিথ্যা সিগন্যাল তৈরি হতে পারে, বাজার পরিবেশ সনাক্তকরণ প্রয়োজন

- প্যারামিটার অপ্টিমাইজেশনের অতিরিক্ত ব্যবহার ওভারফিটিং ঝুঁকি বাড়াতে পারে

- উচ্চ অস্থিরতার সময় মাল্টিপল ইন্ডিকেটর ল্যাগ ইফেক্ট তৈরি করতে পারে

- স্টপ-লস লেভেলের ভুল সেটিং বড় ড্রডাউনের কারণ হতে পারে

কৌশল অপ্টিমাইজেশন দিকনির্দেশনা

- বাজার পরিবেশ সনাক্তকরণ মডিউল অন্তর্ভুক্ত করা, বিভিন্ন বাজার অবস্থায় বিভিন্ন প্যারামিটার সেটিং ব্যবহার করা

- অভিযোজিত স্টপ-লস মেকানিজম তৈরি করা, বাজার অস্থিরতা অনুযায়ী গতিশীলভাবে স্টপ-লস লেভেল সামঞ্জস্য করা

- ট্রেডিং ভলিউম বিশ্লেষণ ইন্ডিকেটর যোগ করা, সিগন্যালের নির্ভরযোগ্যতা বৃদ্ধি করা

- G-চ্যানেলের গণনা পদ্ধতি অপ্টিমাইজ করা, ল্যাগ ইফেক্ট কমানো

সারসংক্ষেপ

এই কৌশলটি একাধিক প্রযুক্তিগত সূচক সমন্বয় করে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করেছে। এর মূল শক্তি হল মাল্টি-ডাইমেনশনাল সিগন্যাল কনফার্মেশন মেকানিজম এবং সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা সিস্টেম। ক্রমাগত অপ্টিমাইজেশন এবং উন্নতির মাধ্যমে, কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল পারফরম্যান্স বজায় রাখতে সক্ষম হতে পারে। ট্রেডারদের লাইভ ট্রেডিংয়ে যাওয়ার আগে বিভিন্ন প্যারামিটার কম্বিনেশন পুঙ্খানুপুঙ্খভাবে পরীক্ষা করার এবং নির্দিষ্ট বাজার বৈশিষ্ট্য অনুযায়ী যথাযথ সমন্বয় করার পরামর্শ দেওয়া হয়।

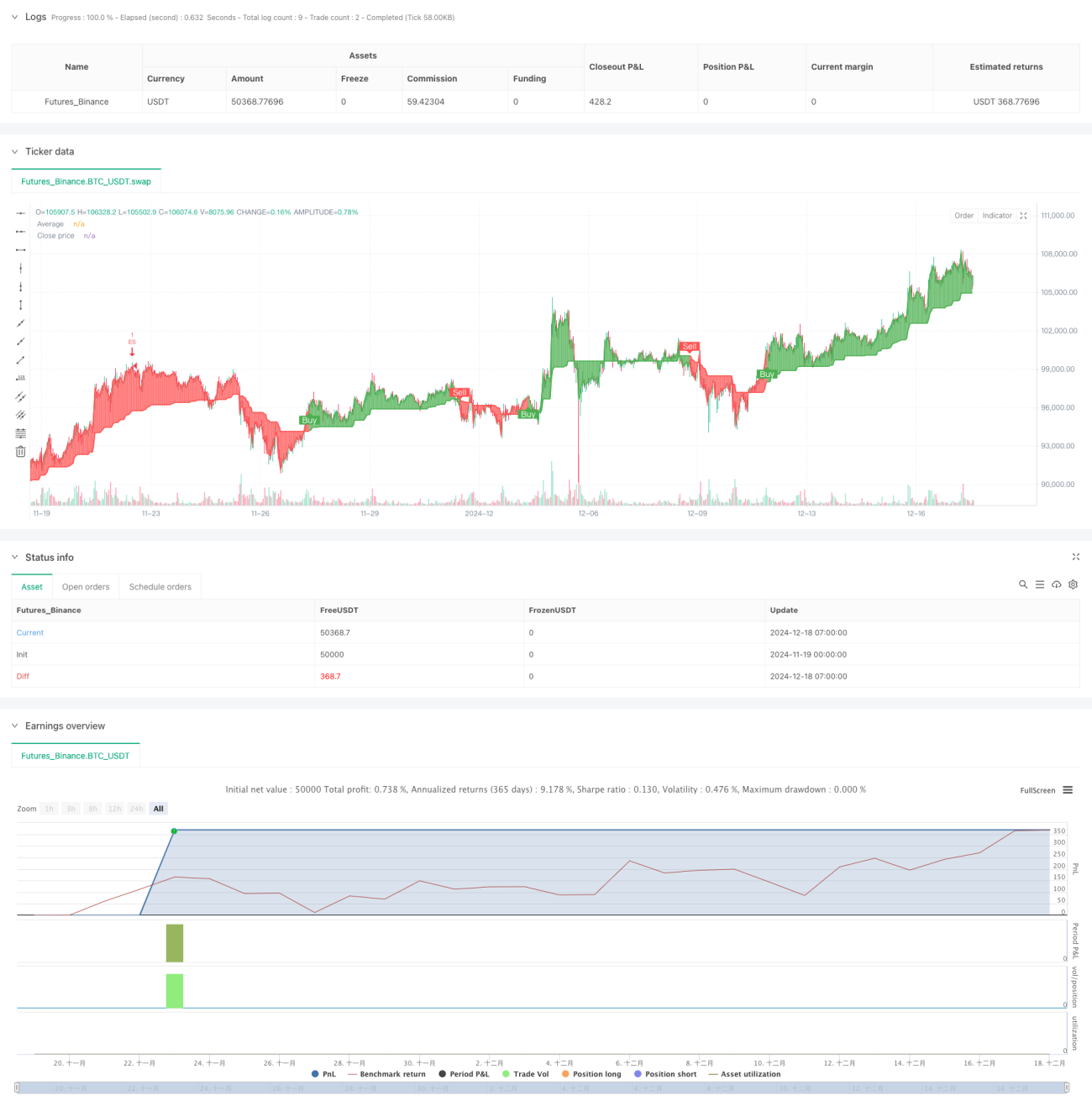

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("VinSpace Optimized Strategy", shorttitle="VinSpace Magic", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input Parameters- 1