বহু মুভিং এভারেজ ক্রসওভার ও ক্যামারিলা সাপোর্ট রেজিস্ট্যান্স ট্রেন্ড ট্রেডিং সিস্টেম

সংক্ষিপ্ত বিবরণ

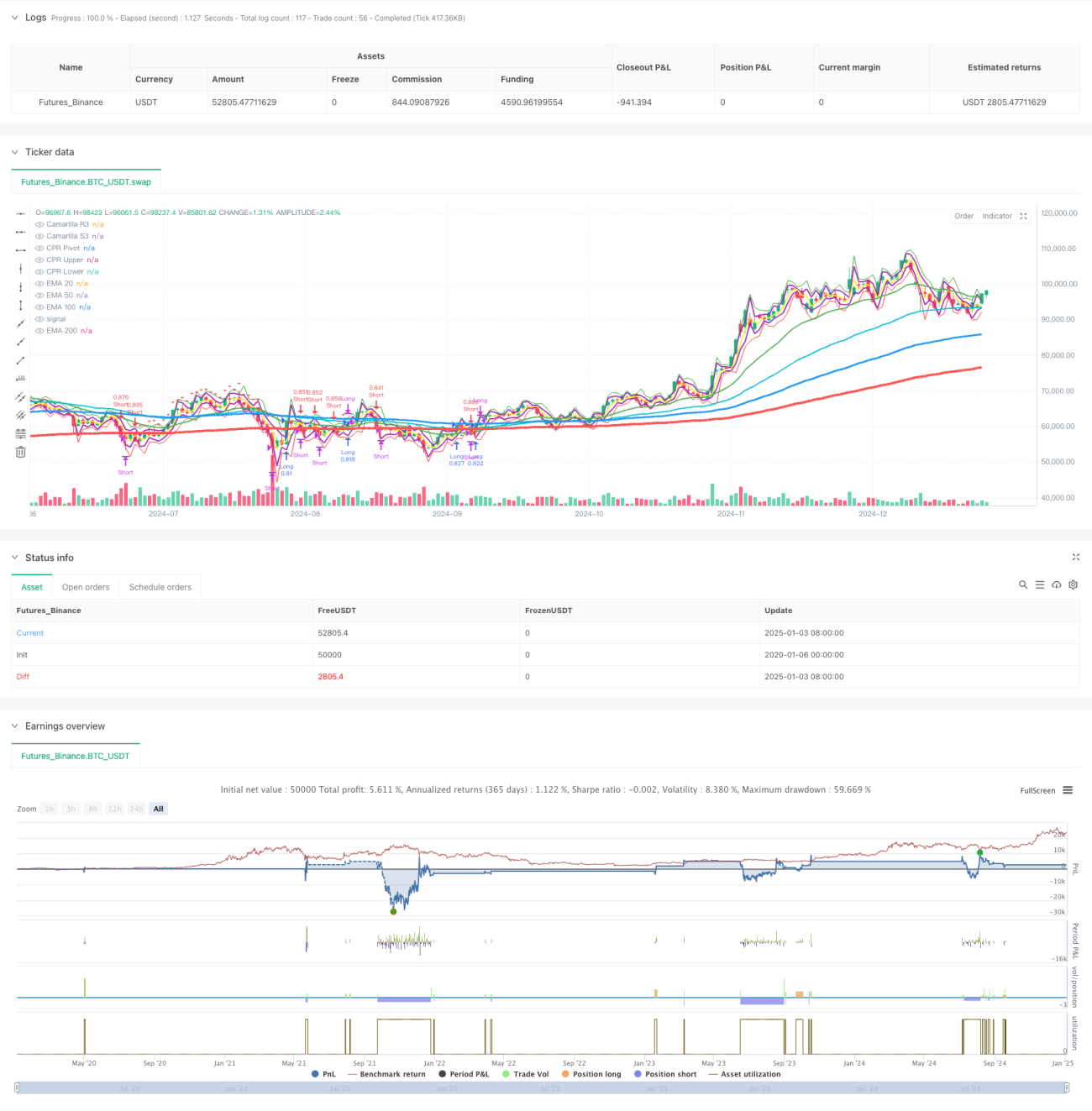

এই কৌশলটি একাধিক এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA), ক্যামারিলা সাপোর্ট-রেজিস্ট্যান্স লেভেল এবং সেন্ট্রাল পিভট রেঞ্জ (CPR) এর সমন্বয়ে গঠিত একটি ট্রেন্ড ফলোয়িং ট্রেডিং সিস্টেম। এই কৌশলটি দাম এবং একাধিক মুভিং এভারেজের সম্পর্ক এবং গুরুত্বপূর্ণ মূল্য পরিসীমা বিশ্লেষণ করে বাজারের ট্রেন্ড এবং সম্ভাব্য ট্রেডিং সুযোগ চিহ্নিত করে। সিস্টেমটি কঠোর মানি ম্যানেজমেন্ট এবং ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা গ্রহণ করে, যার মধ্যে শতাংশভিত্তিক পজিশন সাইজিং এবং বিবিধ এক্সিট মেকানিজম অন্তর্ভুক্ত।

কৌশল নীতি

কৌশলটি মূলত নিম্নলিখিত মূল উপাদানগুলির উপর ভিত্তি করে তৈরি:

- মাল্টিপল মুভিং এভারেজ সিস্টেম (EMA20/50/100/200) ট্রেন্ডের দিক এবং শক্তি নিশ্চিত করতে ব্যবহৃত হয়।

- ক্যামারিলা সাপোর্ট-রেজিস্ট্যান্স লেভেল (R3/S3) মূল্য স্তর চিহ্নিত করতে ব্যবহৃত হয়।

- সেন্ট্রাল পিভট রেঞ্জ (CPR) দৈনিক ট্রেডিং রেঞ্জ নির্ধারণ করতে ব্যবহৃত হয়।

- এন্ট্রি সিগন্যাল দামের EMA200 ক্রসিং এবং EMA20 এর নিশ্চিতকরণের উপর ভিত্তি করে তৈরি।

- এক্সিট কৌশলে দুটি মোড অন্তর্ভুক্ত: নির্দিষ্ট পয়েন্ট এবং শতাংশভিত্তিক মুভমেন্ট।

- মানি ম্যানেজমেন্ট সিস্টেম অ্যাকাউন্ট আকারের উপর ভিত্তি করে পজিশনের আকার গতিশীলভাবে সমন্বয় করে।

কৌশলের সুবিধা

- বহুমাত্রিক প্রযুক্তিগত সূচকের সমন্বয় আরও নির্ভরযোগ্য ট্রেডিং সিগন্যাল প্রদান করে।

- নমনীয় এক্সিট মেকানিজম বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে পারে।

- সুসংহত মানি ম্যানেজমেন্ট সিস্টেম কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করে।

- ট্রেন্ড ফলোয়িং বৈশিষ্ট্য বড় মুভমেন্ট ক্যাপচার করতে সহায়তা করে।

- ভিজুয়াল উপাদান ব্যবসায়ীদের বাজারের কাঠামো বুঝতে সহায়তা করে।

কৌশলের ঝুঁকি

- পাশ কাটানো বাজারে মিথ্যা সিগন্যাল তৈরি হতে পারে।

- একাধিক সূচক ট্রেডিং সিগন্যালে পিছিয়ে পড়ার কারণ হতে পারে।

- নির্দিষ্ট এক্সিট পয়েন্ট উচ্চ অস্থিরতার বাজারে ভালো পারফর্ম নাও করতে পারে।

- ড্রডাউন সহ্য করার জন্য বড় মূলধনের প্রয়োজন হয়।

- ট্রেডিং খরচ সামগ্রিক লাভকে প্রভাবিত করতে পারে।

কৌশল অপ্টিমাইজেশনের দিক

- অস্থিরতা সূচক যুক্ত করে ইনপুট এবং আউটপুট প্যারামিটার গতিশীলভাবে সমন্বয় করা।

- বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে বাজার অবস্থা শনাক্তকরণ মডিউল যুক্ত করা।

- মানি ম্যানেজমেন্ট সিস্টেম অপ্টিমাইজ করে গতিশীল পজিশন ম্যানেজমেন্ট যুক্ত করা।

- সিগন্যালের গুণমান উন্নত করতে ট্রেডিং টাইম ফিল্টার যুক্ত করা।

- সিগন্যাল নির্ভরযোগ্যতা বাড়াতে ভলিউম বিশ্লেষণ যুক্ত করার কথা বিবেচনা করা।

সারসংক্ষেপ

এই কৌশলটি একাধিক ক্লাসিক প্রযুক্তিগত বিশ্লেষণ টুল একীভূত করে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করেছে। সিস্টেমটির সুবিধা হলো বহুমাত্রিক বাজার বিশ্লেষণ এবং কঠোর ঝুঁকি ব্যবস্থাপনা, তবে বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নেওয়ার বিষয়টি বিবেচনায় নেওয়া জরুরি। ক্রমাগত অপ্টিমাইজেশন এবং উন্নতির মাধ্যমে, কৌশলটি স্থিতিশীলতা বজায় রেখে লাভজনকতা বাড়ানোর সম্ভাবনা রাখে।

- 1