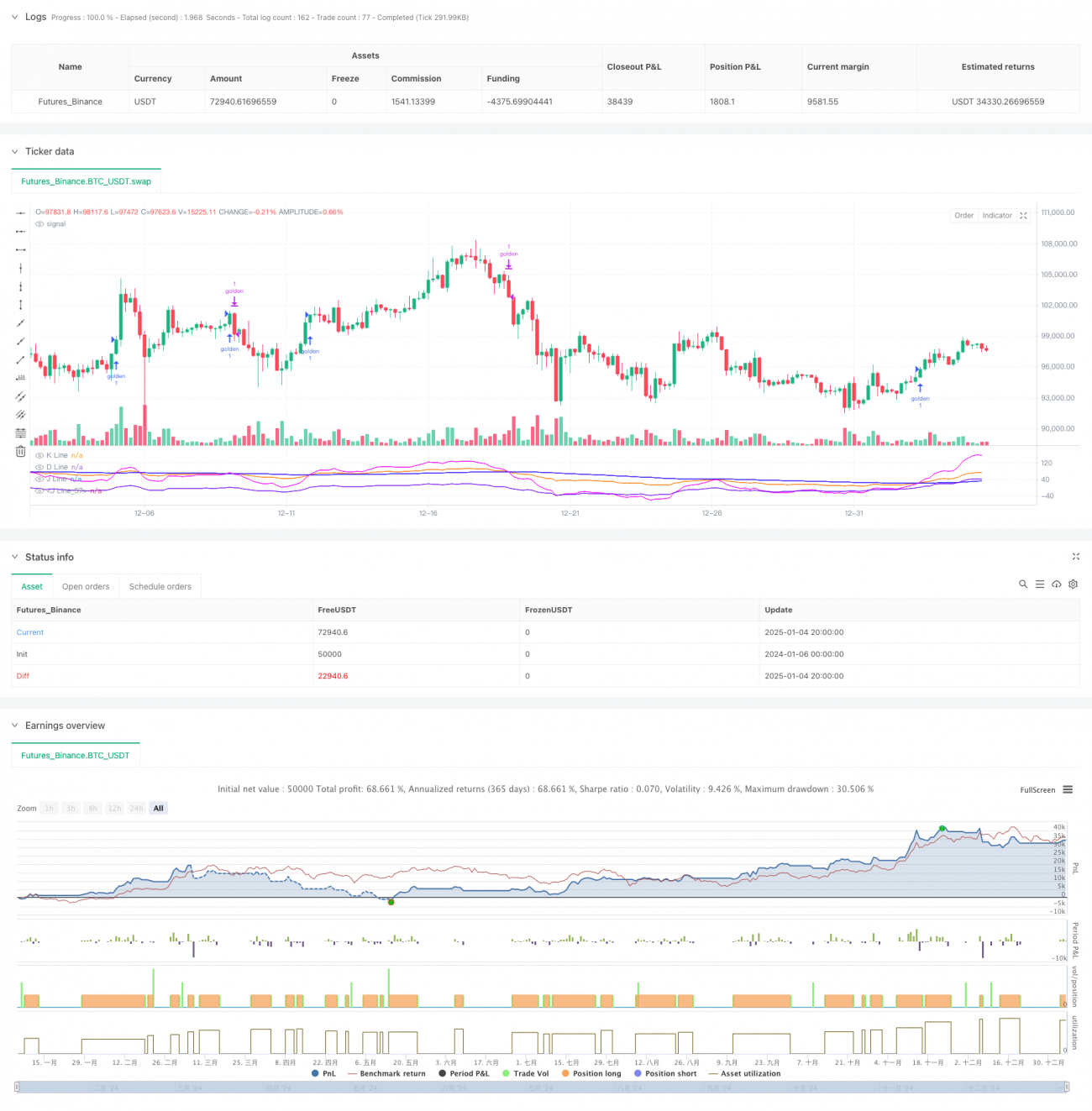

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি KDJ নির্দেশকের উপর ভিত্তি করে উন্নত ট্রেডিং সিস্টেম, যা K লাইন, D লাইন এবং J লাইনের ক্রসওভার প্যাটার্নের গভীর বিশ্লেষণের মাধ্যমে বাজারের প্রবণতা ধারণ করে। কৌশলটি একটি কাস্টমাইজড BCWSMA স্মুথিং অ্যালগরিদমকে একীভূত করে, যা স্টোকাস্টিক নির্দেশকের অপ্টিমাইজড গণনার মাধ্যমে সংকেতের নির্ভরযোগ্যতা বৃদ্ধি করে। সিস্টেমটি স্টপ-লস এবং ট্রেলিং স্টপ-লস ফাংশন সহ কঠোর ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা ব্যবহার করে, যাতে মজবুত পুঁজি ব্যবস্থাপনা নিশ্চিত করা যায়।

কৌশলের নীতি

কৌশলের মূল যুক্তি নিম্নলিখিত মূল উপাদানগুলির উপর ভিত্তি করে:

- KDJ নির্দেশক গণনার জন্য কাস্টমাইজড BCWSMA (ওয়েটেড মুভিং অ্যাভারেজ) অ্যালগরিদম ব্যবহার করা, যা নির্দেশকের মসৃণতা এবং স্থিতিশীলতা বৃদ্ধি করে।

- RSV (অপরিণত স্টোকাস্টিক মান) গণনার মাধ্যমে, দামকে 0-100 পরিসরের একটি সংখ্যায় রূপান্তর করা, যা উচ্চ-নিম্ন পয়েন্টের মধ্যে দামের অবস্থানকে ভালোভাবে প্রতিফলিত করে।

- একটি অনন্য J লাইন এবং J5 লাইন (ডেরিভেটিভ নির্দেশক) ক্রস-ভেরিফিকেশন মেকানিজম ডিজাইন করা, যা একাধিক নিশ্চিতকরণের মাধ্যমে ট্রেডিং সংকেতের নির্ভুলতা বৃদ্ধি করে।

- ধারাবাহিকতার উপর ভিত্তি করে একটি প্রবণতা নিশ্চিতকরণ ব্যবস্থা প্রতিষ্ঠা করা, যার জন্য J লাইনকে প্রবণতার বৈধতা নিশ্চিত করতে পরপর 3 দিন D লাইনের উপরে থাকতে হবে।

- শতাংশ স্টপ-লস এবং ট্রেলিং স্টপ-লসের সমন্বয়ে গঠিত একটি যৌগিক ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা একীভূত করা।

কৌশলের সুবিধা

- সংকেত জেনারেশন মেকানিজম উন্নত: একাধিক প্রযুক্তিগত নির্দেশকের ক্রস-ভেরিফিকেশনের মাধ্যমে, মিথ্যা সংকেতের প্রভাব উল্লেখযোগ্যভাবে হ্রাস পায়।

- ঝুঁকি নিয়ন্ত্রণ সম্পূর্ণ: নির্দিষ্ট স্টপ-লস এবং ট্রেলিং স্টপ-লস সহ বহুস্তরীয় ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা ব্যবহার করে, নিম্নগামী ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করা যায়।

- প্যারামিটার সামঞ্জস্যক্ষমতা শক্তিশালী: KDJ পিরিয়ড, সংকেত স্মুথিং সহগ ইত্যাদি মূল প্যারামিটারগুলি বাজারের পরিস্থিতি অনুযায়ী নমনীয়ভাবে সামঞ্জস্য করা যায়।

- গণনার দক্ষতা উচ্চ: অপ্টিমাইজড BCWSMA অ্যালগরিদম ব্যবহার করে, গণনার জটিলতা হ্রাস পায় এবং কৌশল কার্যকর করার দক্ষতা বৃদ্ধি পায়।

- অভিযোজনক্ষমতা ভাল: বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে পারে এবং প্যারামিটার সমন্বয়ের মাধ্যমে কৌশলের কর্মক্ষমতা অপ্টিমাইজ করা যায়।

কৌশলের ঝুঁকি

- অস্থির বাজার ঝুঁকি: সাইডওয়ে বা রেঞ্জ-বাউন্ড বাজারে ঘন ঘন মিথ্যা ব্রেকআউট সংকেত তৈরি হতে পারে, যা ট্রেডিং খরচ বাড়িয়ে দেয়।

- ল্যাগ ঝুঁকি: মুভিং এভারেজ স্মুথিং ব্যবহারের কারণে, সংকেত কিছুটা বিলম্বিত হতে পারে।

- প্যারামিটার সংবেদনশীলতা: কৌশলের ফলাফল প্যারামিটার সেটিংসের প্রতি অত্যন্ত সংবেদনশীল; অনুপযুক্ত প্যারামিটার সেটিংস কৌশলের কার্যকারিতা উল্লেখযোগ্যভাবে হ্রাস করতে পারে।

- বাজার পরিবেশের উপর নির্ভরশীলতা: নির্দিষ্ট কিছু বাজার পরিবেশে, কৌশলের কর্মক্ষমতা প্রত্যাশা অনুযায়ী ভাল নাও হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- সংকেত ফিল্টারিং মেকানিজম অপ্টিমাইজেশন: ট্রেডিং ভলিউম, অস্থিরতা ইত্যাদি সহায়ক নির্দেশক অন্তর্ভুক্ত করে সংকেতের নির্ভরযোগ্যতা বাড়ানো যায়।

- ডায়নামিক প্যারামিটার অ্যাডজাস্টমেন্ট: বাজারের অস্থিরতা অনুযায়ী KDJ প্যারামিটার এবং স্টপ-লস প্যারামিটার গতিশীলভাবে সামঞ্জস্য করা।

- বাজার পরিবেশ সনাক্তকরণ: বাজার পরিবেশ মূল্যায়ন মডিউল যুক্ত করা, যাতে বিভিন্ন বাজার পরিবেশে ভিন্ন ট্রেডিং কৌশল ব্যবহার করা যায়।

- ঝুঁকি নিয়ন্ত্রণ বৃদ্ধি: সর্বোচ্চ ড্রডাউন নিয়ন্ত্রণ, পজিশন হোল্ডিং সময় সীমা ইত্যাদি অতিরিক্ত ঝুঁকি নিয়ন্ত্রণ পদ্ধতি যোগ করা যায়।

- কর্মক্ষমতা অপ্টিমাইজেশন: BCWSMA অ্যালগরিদম আরও অপ্টিমাইজ করে গণনার দক্ষতা বাড়ানো।

সারসংক্ষেপ

এই কৌশলটি উদ্ভাবনী প্রযুক্তিগত নির্দেশকের সমন্বয় এবং কঠোর ঝুঁকি নিয়ন্ত্রণের মাধ্যমে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করেছে। কৌশলটির মূল সুবিধা হলো একাধিক সংকেত নিশ্চিতকরণ ব্যবস্থা এবং পূর্ণাঙ্গ ঝুঁকি নিয়ন্ত্রণ কাঠামো, তবে প্যারামিটার অপ্টিমাইজেশন এবং বাজার পরিবেশের সাথে অভিযোজনযোগ্যতার বিষয়টিও লক্ষ্য রাখতে হবে। ধারাবাহিক অপ্টিমাইজেশন এবং উন্নতির মাধ্যমে, কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল কর্মক্ষমতা বজায় রাখার আশা করা যায়।

- 1