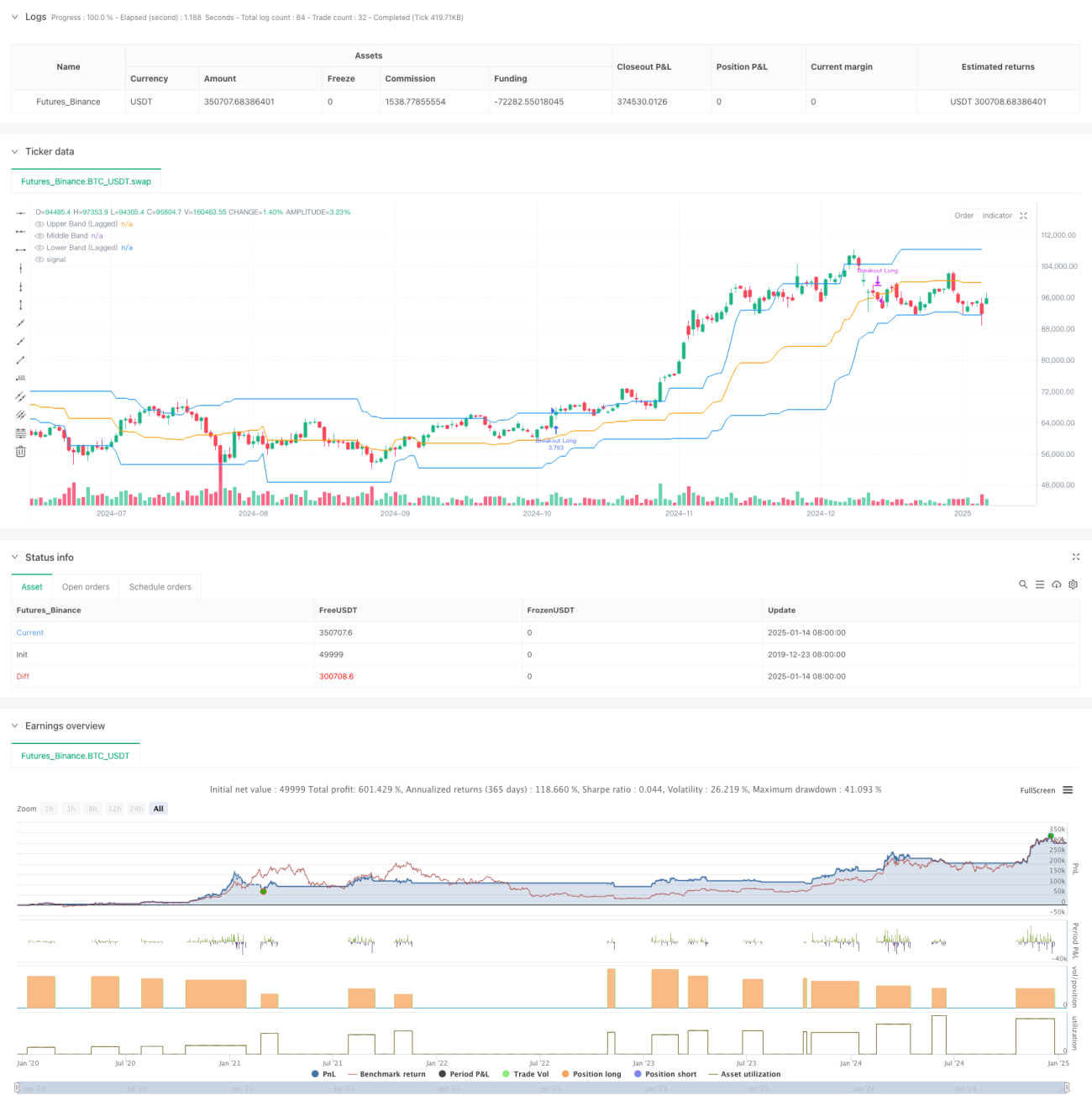

সংক্ষিপ্ত বিবরণ

এটি একটি ডনচিয়ান চ্যানেল (Donchian Channel) ভিত্তিক মোমেন্টাম ব্রেকআউট ট্রেডিং কৌশল, যা মূল্য ব্রেকআউট এবং ট্রেডিং ভলিউম নিশ্চিতকরণ — এই দুটি গুরুত্বপূর্ণ শর্তকে একত্রিত করে। এই কৌশলটি পূর্বনির্ধারিত মূল্য পরিসীমা অতিক্রম করে কিনা এবং ভলিউম সমর্থন রয়েছে কিনা তা পর্যবেক্ষণ করে বাজারের ঊর্ধ্বমুখী প্রবণতা ধারণ করে। কৌশলটি চ্যানেলের স্থিতিশীলতা বাড়ানোর জন্য ল্যাগ প্যারামিটার ব্যবহার করে এবং প্রস্থানের শর্ত নির্বাচনের নমনীয়তা প্রদান করে।

কৌশলের নীতি

কৌশলের মূল লজিক নিম্নলিখিত গুরুত্বপূর্ণ অংশগুলি নিয়ে গঠিত:

- প্রধান প্রযুক্তিগত নির্দেশক হিসেবে ল্যাগযুক্ত ডনচিয়ান চ্যানেল ব্যবহার করা হয়, যা গত ২৭টি পিরিয়ডের সর্বোচ্চ ও সর্বনিম্ন মূল্য গণনা করে উচ্চতর রেখা, মধ্যম রেখা এবং নিম্নতর রেখা তৈরি করে।

- প্রবেশের শর্ত একসঙ্গে পূরণ করতে হবে:

- ক্লোজিং মূল্য ডনচিয়ান চ্যানেলের উচ্চতর রেখা ভেঙে যায়

- বর্তমান ট্রেডিং ভলিউম গত ২৭ পিরিয়ডের গড় ভলিউমের ১.৪ গুণের বেশি হয়

- প্রস্থানের শর্ত নমনীয়ভাবে নির্বাচনযোগ্য:

- মূল্য উচ্চতর, মধ্যম বা নিম্নতর রেখা ভেঙে গেলে প্রস্থান করার বিকল্প রয়েছে

- ডিফল্ট হিসাবে মধ্যম রেখা প্রস্থান সিগন্যাল হিসাবে ব্যবহৃত হয়

- ১০ পিরিয়ডের ল্যাগ প্যারামিটারের মাধ্যমে চ্যানেলের স্থিতিশীলতা বৃদ্ধি করা হয় এবং মিথ্যা ব্রেকআউট কমানো হয়।

কৌশলের সুবিধা

- বহু-নিশ্চিতকরণ প্রক্রিয়া: মূল্য ব্রেকআউট এবং ভলিউম নিশ্চিতকরণ একত্রিত করে মিথ্যা সিগন্যালের ঝুঁকি ব্যাপকভাবে হ্রাস পায়।

- অভিযোজন ক্ষমতা: প্যারামিটারাইজড ডিজাইনের মাধ্যমে কৌশলটি বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে পারে।

- ঝুঁকি নিয়ন্ত্রণ সম্পূর্ণ: একাধিক প্রস্থান শর্তের বিকল্প রয়েছে, যা বিভিন্ন ঝুঁকি পছন্দ অনুযায়ী সামঞ্জস্য করা সহজ করে।

- স্পষ্ট কার্যকারিতা: প্রবেশ ও প্রস্থানের শর্ত পরিষ্কার, অস্পষ্টতা নেই।

- বাস্তবায়ন সহজ: কৌশলের লজিক সহজ ও সরল, বাস্তব ট্রেডিংয়ের জন্য সুবিধাজনক।

কৌশলের ঝুঁকি

- বাজার অস্থিরতার ঝুঁকি: অস্থির বাজারে ঘন ঘন মিথ্যা ব্রেকআউট সিগন্যাল তৈরি হতে পারে।

- স্লিপেজ ঝুঁকি: ব্রেকআউটের সময় ট্রেডিং ভলিউম প্রায়ই বেশি হয়, ফলে বড় স্লিপেজের সম্মুখীন হওয়া সম্ভব।

- ট্রেন্ড রিভার্সাল ঝুঁকি: যদি বাজার হঠাৎ করে উল্টে যায়, তাহলে সময়মতো প্রস্থান করা সম্ভব নাও হতে পারে।

- প্যারামিটার সংবেদনশীলতা: কৌশলের ফলাফল প্যারামিটার সেটিংসের প্রতি সংবেদনশীল, যত্ন সহকারে অপ্টিমাইজেশন প্রয়োজন।

কৌশলের অপ্টিমাইজেশন দিকনির্দেশনা

- ট্রেন্ড ফিল্টার যোগ করা: চলমান গড় সিস্টেমের মতো অতিরিক্ত ট্রেন্ড নির্ধারণকারী নির্দেশক যুক্ত করা যেতে পারে।

- ভলিউম নির্দেশক অপ্টিমাইজ করা: OBV বা মানি ফ্লো ইনডেক্সের মতো আরও জটিল ভলিউম বিশ্লেষণ পদ্ধতি ব্যবহার করা যেতে পারে।

- স্টপ-লস প্রক্রিয়া সম্পূর্ণ করা: ট্রেইলিং স্টপ-লস বা নির্দিষ্ট স্টপ-লস ফাংশন যুক্ত করা।

- সময় ফিল্টার যোগ করা: দিনের মধ্যে সময় ফিল্টার যুক্ত করে উচ্চ অস্থিরতার সময় (যেমন খোলা ও বন্ধের সময়) ট্রেডিং এড়ানো যেতে পারে।

- অস্থিরতা অভিযোজন প্রবর্তন: বাজারের অস্থিরতার উপর ভিত্তি করে স্বয়ংক্রিয়ভাবে প্যারামিটার সমন্বয় করে কৌশলের অভিযোজন ক্ষমতা বাড়ানো।

সারসংক্ষেপ

এটি একটি যুক্তিযুক্ত ও পরিষ্কার লজিকসম্পন্ন ট্রেন্ড-অনুসরণকারী কৌশল। মূল্য ব্রেকআউট এবং ভলিউম নিশ্চিতকরণ একত্রিত করে কৌশলটি নির্ভরযোগ্যতা বজায় রেখে ভাল নমনীয়তাও বজায় রাখে। কৌশলের প্যারামিটারাইজড ডিজাইন এটিকে ভাল অভিযোজন ক্ষমতা প্রদান করে, তবে একইসঙ্গে বিনিয়োগকারীদের নির্দিষ্ট বাজার পরিস্থিতি অনুযায়ী অপ্টিমাইজেশন ও সমন্বয় করতে হয়। সামগ্রিকভাবে, এটি একটি কৌশল কাঠামো যা আরও অপ্টিমাইজেশন এবং অনুশীলনের যোগ্য।

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-15 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=6

strategy("Breakout Strategy", overlay=true, calc_on_every_tick=false, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.1, pyramiding=1, fill_orders_on_standard_ohlc=true)

- 1