উন্নত মাল্টিপল ট্রেন্ড কনফার্মেশন সহ EMA সাপ্লাই-ডিমান্ড জোন ডায়নামিক আর্ভিট্রাজ কৌশল

সারসংক্ষেপ

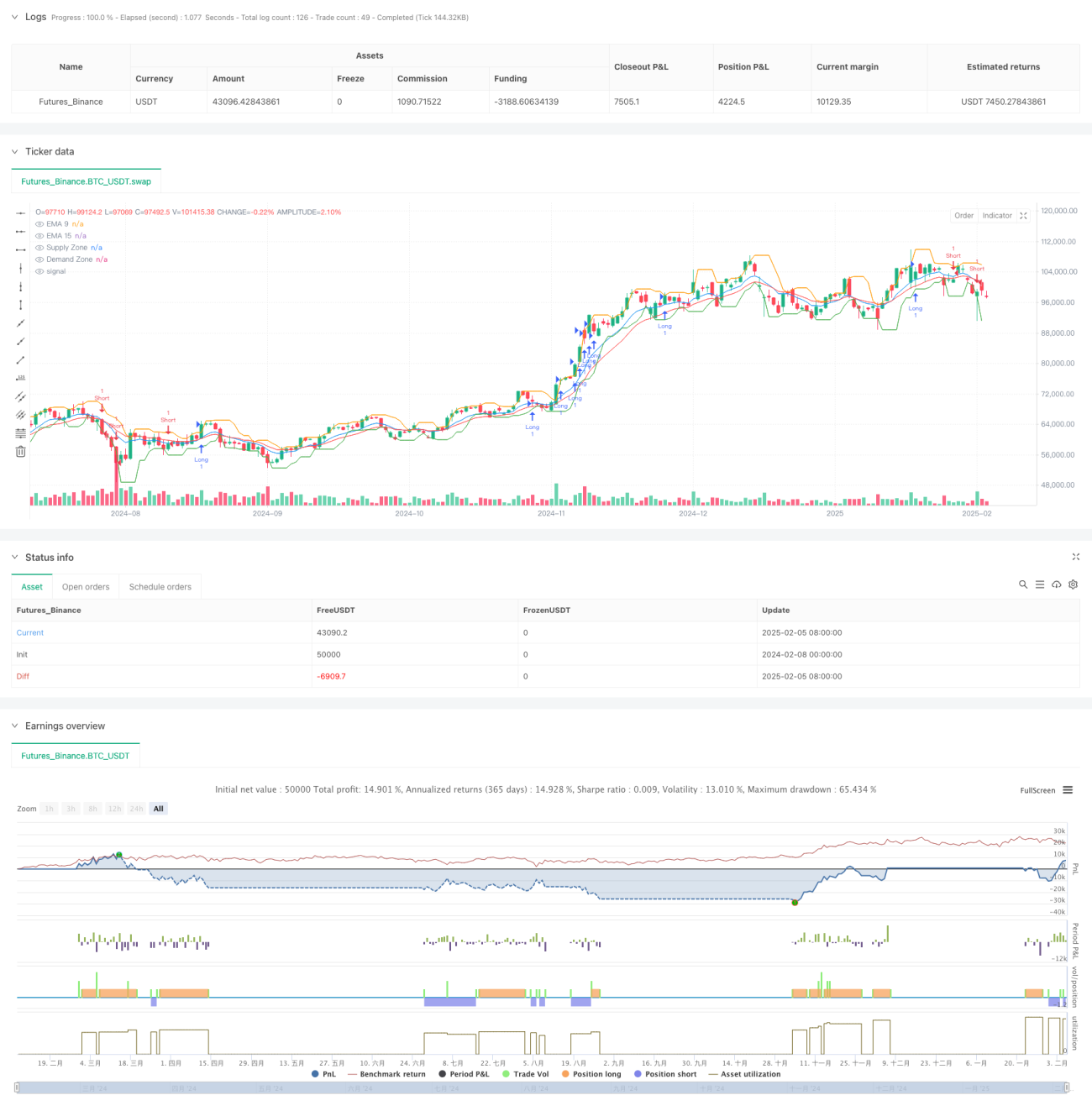

এই কৌশলটি একটি উন্নত অভিযোজনযোগ্য আর্বিট্রেজ কৌশল যা মুভিং এভারেজ (EMA), সরবরাহ ও চাহিদা অঞ্চল এবং ট্রেডিং ভলিউমকে একত্রিত করে। এটি একাধিক প্রযুক্তিগত সূচকের ক্রস-কনফার্মেশন ব্যবহার করে বাজারের প্রবণতা চিহ্নিত করে এবং মূল সরবরাহ ও চাহিদা অঞ্চলের কাছাকাছি ট্রেড করে। কৌশলটি গতিশীল স্টপ-লস এবং লাভের লক্ষ্য ব্যবহার করে এবং ATR সূচকের মাধ্যমে বাজারের অস্থিরতার সাথে খাপ খায়।

কৌশলের মূলনীতি

কৌশলের মূল লজিক নিম্নলিখিত মূল উপাদানের উপর ভিত্তি করে তৈরি:

- ৯-পিরিয়ড এবং ১৫-পিরিয়ড EMA-র প্রবণতার দিকটি প্রধান ট্রেডিং সিগন্যাল হিসেবে ব্যবহার করা

- উচ্চতর টাইমফ্রেম (১৫ মিনিট) এর সরবরাহ ও চাহিদা অঞ্চলের মাধ্যমে গুরুত্বপূর্ণ দামের স্তর নির্ধারণ করা

- ট্রেডিং ভলিউম কনফার্মেশন ব্যবহার করে প্রবণতার বৈধতা যাচাই করা

- ATR-ভিত্তিক গতিশীল স্টপ-লস এবং লাভের লক্ষ্য ব্যবহার করে ঝুঁকি ব্যবস্থাপনা করা

- একাধিক শর্ত একসাথে পূরণ হলেই ট্রেড করা

বিশেষভাবে, যখন ৯-পিরিয়ড EMA টানা ৩ পিরিয়ড ধরে ঊর্ধ্বমুখী হয়, ১৫-পিরিয়ড EMA ও ঊর্ধ্বমুখী প্রবণতায় থাকে এবং দাম চাহিদা অঞ্চলের উপরে থাকে, এবং একই সাথে ২০-পিরিয়ড ভলিউম মুভিং এভারেজ ৫০-পিরিয়ড ভলিউম মুভিং এভারেজের চেয়ে বেশি হয়, তখন সিস্টেম লং সিগন্যাল জারি করে। শর্ট সিগন্যালের লজিক বিপরীত।

কৌশলের সুবিধা

- একাধিক কনফার্মেশন মেকানিজম ট্রেডের নির্ভরযোগ্যতা উল্লেখযোগ্যভাবে বৃদ্ধি করে

- গতিশীল স্টপ-লস এবং লাভের লক্ষ্য বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে সক্ষম

- সরবরাহ ও চাহিদা অঞ্চলের ফিল্টারিং প্রতিকূল দামের অঞ্চলে ট্রেড করা এড়াতে সাহায্য করে

- ভলিউম কনফার্মেশন অতিরিক্ত প্রবণতা যাচাইকরণ প্রদান করে

- ঝুঁকি-পুরস্কার অনুপাত বাজারের অবস্থা অনুযায়ী নমনীয়ভাবে সমন্বয় করা যায়

- কৌশলটি ভাল অভিযোজনযোগ্যতা রাখে এবং বিভিন্ন বাজার অবস্থার জন্য উপযুক্ত

কৌশলের ঝুঁকি

- উচ্চ অস্থির বাজারে মিথ্যা সিগন্যাল দেখা দিতে পারে

- একাধিক কনফার্মেশন শর্ত কিছু ট্রেডিং সুযোগ মিস করতে পারে

- সরবরাহ ও চাহিদা অঞ্চল শনাক্তকরণে পিছিয়ে থাকা সম্ভব

- সাইডওয়ে বাজারে ঘন ঘন ট্রেডিং সিগন্যাল তৈরি হতে পারে

ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা:

- বাজারের অস্থিরতার সাথে খাপ খাইয়ে গতিশীল ATR স্টপ-লস ব্যবহার

- ভলিউম কনফার্মেশনের মাধ্যমে মিথ্যা সিগন্যাল ফিল্টার করা

- কঠোর ঝুঁকি-পুরস্কার অনুপাত নিয়ন্ত্রণ প্রয়োগ

- মূল দামের স্তরের কাছাকাছি ট্রেড করা

কৌশল অপ্টিমাইজেশনের দিকনির্দেশ

- অভিযোজনযোগ্য EMA পিরিয়ড অন্তর্ভুক্ত করা যা বাজারের অস্থিরতা অনুযায়ী স্বয়ংক্রিয়ভাবে সমন্বয় করতে পারে

- বাজার অবস্থা শনাক্তকরণ মডিউল যোগ করা যাতে বিভিন্ন বাজার পরিবেশে ভিন্ন প্যারামিটার ব্যবহার করা যায়

- সরবরাহ ও চাহিদা অঞ্চল গণনার পদ্ধতি অপ্টিমাইজ করে শনাক্তকরণের নির্ভুলতা বাড়ানো

- আরও বেশি বাজার মাইক্রোস্ট্রাকচার বিশ্লেষণ অন্তর্ভুক্ত করা

- গতিশীল ঝুঁকি-পুরস্কার অনুপাত সমন্বয় ব্যবস্থা তৈরি করা

উপসংহার

এটি একটি সম্পূর্ণ ট্রেডিং সিস্টেম যা একাধিক প্রযুক্তিগত বিশ্লেষণ সরঞ্জামকে একত্রিত করে এবং একাধিক কনফার্মেশন মেকানিজমের মাধ্যমে ট্রেডের নির্ভরযোগ্যতা বাড়ায়। কৌশলটির শক্তি তার অভিযোজনযোগ্যতা এবং ঝুঁকি ব্যবস্থাপনা ক্ষমতার মধ্যে নিহিত, তবে বিভিন্ন বাজার পরিবেশে কর্মক্ষমতার পার্থক্যের দিকেও নজর দিতে হবে। প্রস্তাবিত অপ্টিমাইজেশন দিকনির্দেশ অনুসরণ করলে কৌশলটির আরও উন্নতির সম্ভাবনা রয়েছে।

- 1