গতিশীল ট্রেন্ড ফলোয়িং EMA-ADX মাল্টি-লেভেল টেক প্রফিট কৌশল

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি EMA এবং ADX সূচক ভিত্তিক ট্রেন্ড ট্র্যাকিং ট্রেডিং সিস্টেম, যা মাল্টি-লেভেল প্রফিট টেকিং এবং ট্রেলিং স্টপ লসের মাধ্যমে অর্থ ব্যবস্থাপনাকে অপ্টিমাইজ করে। কৌশলটি ট্রেন্ড দিক নির্ধারণের জন্য EMA মুভিং এভারেজ, ট্রেন্ড শক্তি ফিল্টার করার জন্য ADX সূচক ব্যবহার করে এবং ধাপে ধাপে লাভ তোলার জন্য তিন স্তরের প্রফিট টেকিং মেকানিজম তৈরি করে, পাশাপাশি এটিআর ব্যবহার করে গতিশীলভাবে স্টপ লস অবস্থান সমন্বয় করে ঝুঁকি নিয়ন্ত্রণ করে।

কৌশলের মূলনীতি

কৌশলের মূল যুক্তিতে নিম্নলিখিত গুরুত্বপূর্ণ অংশগুলি অন্তর্ভুক্ত রয়েছে:

- ট্রেন্ড দিক নির্ধারণের জন্য ৫০-পিরিয়ড EMA মুভিং এভারেজ ব্যবহার করা হয়; দাম EMA-এর উপরে ভেঙে গেলে লং, নিচে ভেঙে গেলে শর্ট খোলা হয়।

- দুর্বল ট্রেন্ড ফিল্টার করতে ১৪-পিরিয়ড ADX সূচক ব্যবহার করা হয়; ADX > 20 হলে ট্রেন্ড কার্যকর বলে নিশ্চিত করা হয়।

- ১৪-পিরিয়ড এটিআরের ভিত্তিতে গতিশীল স্টপ লস অবস্থান গণনা করা হয়: লং পজিশনের ক্ষেত্রে সর্বনিম্ন দাম থেকে ১ এটিআর বিয়োগ, শর্ট পজিশনের ক্ষেত্রে সর্বোচ্চ দামের সাথে ১ এটিআর যোগ।

- তিন স্তরের প্রফিট টেকিং মেকানিজম ব্যবহার করা হয়:

- প্রথম স্তর: ৩০% অবস্থান ১ গুণ এটিআরে প্রফিট টেকিং

- দ্বিতীয় স্তর: ৫০% অবস্থান ২ গুণ এটিআরে প্রফিট টেকিং

- তৃতীয় স্তর: ২০% অবস্থানের জন্য ৩ গুণ এটিআরের ট্রেলিং প্রফিট টেকিং

- দাম দ্বিতীয় স্তরের প্রফিট টেকিং অবস্থানে পৌঁছালে, স্বয়ংক্রিয়ভাবে সমস্ত অবশিষ্ট অবস্থান বন্ধ করা হয়।

কৌশলের সুবিধা

- মাল্টি-লেভেল প্রফিট টেকিং ডিজাইন সময়মতো লাভ লক করতে পারে, আবার বড় মুভমেন্ট মিস না করতেও সহায়তা করে।

- ট্রেলিং স্টপ লস মেকানিজম বাজারের অস্থিরতার সাথে খাপ খাইয়ে নিতে পারে, গতিশীল ঝুঁকি নিয়ন্ত্রণ প্রদান করে।

- ADX ফিল্টার কার্যকরভাবে সাইডওয়েজ বাজারের ভুয়া সিগন্যাল এড়াতে সাহায্য করে।

- EMA এবং দামের ক্রসওভার পরিষ্কার এন্ট্রি সিগন্যাল প্রদান করে।

- ধাপে ধাপে প্রফিট টেকিং মানসিক ওঠানামা কমায়, যা কৌশলের দীর্ঘমেয়াদী বাস্তবায়নে সহায়ক।

কৌশলের ঝুঁকি

- সাইডওয়েজ বাজারে ঘন ঘন এন্ট্রি-এক্সিটের কারণে খরচ বাড়তে পারে।

- EMA একটি ল্যাগিং ইন্ডিকেটর হওয়ায় দ্রুত রিভার্সালের ক্ষেত্রে সময়মতো প্রতিক্রিয়া নাও দিতে পারে।

- নির্দিষ্ট ADX থ্রেশহোল্ড বিভিন্ন বাজার পরিবেশে সমন্বয়ের প্রয়োজন হতে পারে।

- মাল্টি-লেভেল প্রফিট টেকিং একমুখী ট্রেন্ডে অকালেই পজিশন কমিয়ে দিতে পারে।

প্রতিকার ব্যবস্থা:

- বিভিন্ন বাজার চক্র অনুযায়ী ADX থ্রেশহোল্ড গতিশীলভাবে সমন্বয় করা যেতে পারে।

- ট্রেন্ড নিশ্চিতকরণের জন্য অতিরিক্ত সূচক যুক্ত করার কথা বিবেচনা করা যেতে পারে।

- প্রফিট টেকিং অনুপাতের জন্য আরও সূক্ষ্ম প্যারামিটার অপ্টিমাইজেশন করা যেতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- ট্রেন্ড নিশ্চিতকরণ বাড়ানোর জন্য ভলিউম সূচক অন্তর্ভুক্ত করা।

- বাজারের অস্থিরতা অনুযায়ী ADX থ্রেশহোল্ড গতিশীলভাবে সমন্বয় করা।

- প্রফিট টেকিং স্তরের পজিশন বরাদ্দের অনুপাত অপ্টিমাইজ করা।

- ট্রেন্ড শক্তির গ্রেডিং যোগ করে বিভিন্ন প্রফিট টেকিং কৌশল প্রয়োগ করা।

- মৌসুমী কারণ এবং বাজার চক্র বিচার বিবেচনায় নেওয়া।

সারসংক্ষেপ

এটি একটি পূর্ণাঙ্গ কাঠামো এবং স্পষ্ট যুক্তিসম্পন্ন ট্রেন্ড ট্র্যাকিং কৌশল, যা মাল্টি-লেভেল প্রফিট টেকিং এবং গতিশীল স্টপ লসের মাধ্যমে লাভ ও ঝুঁকির ভারসাম্য বজায় রাখে। কৌশলটির সামগ্রিক নকশা পরিমাণগত ট্রেডিংয়ের মৌলিক নীতির সাথে সামঞ্জস্যপূর্ণ, এবং এর ভাল প্রসারণযোগ্যতা ও অপ্টিমাইজেশনের সুযোগ রয়েছে। যুক্তিসঙ্গত প্যারামিটার সমন্বয় ও আপগ্রেডের মাধ্যমে এই কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল কর্মক্ষমতা প্রদানে সক্ষম।

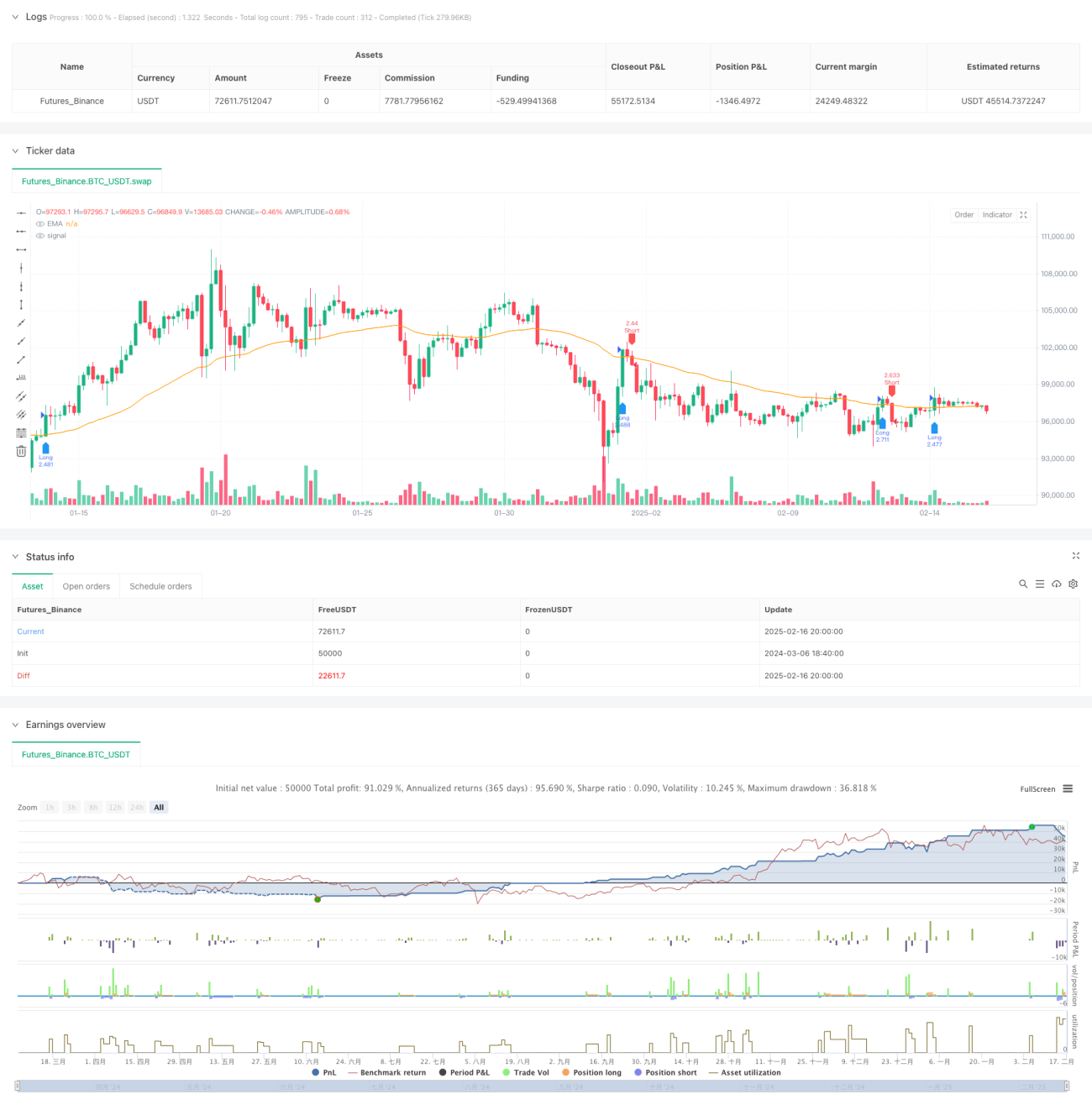

/*backtest

start: 2024-03-06 18:40:00

end: 2025-02-17 00:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("BTC Optimized Strategy v6", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// === 參數設定 ===- 1