একাধিক সূচকের ট্রেন্ড মোমেন্টাম ATR টার্গেট প্রাইস ট্রেডিং স্ট্র্যাটেজি

সারসংক্ষেপ

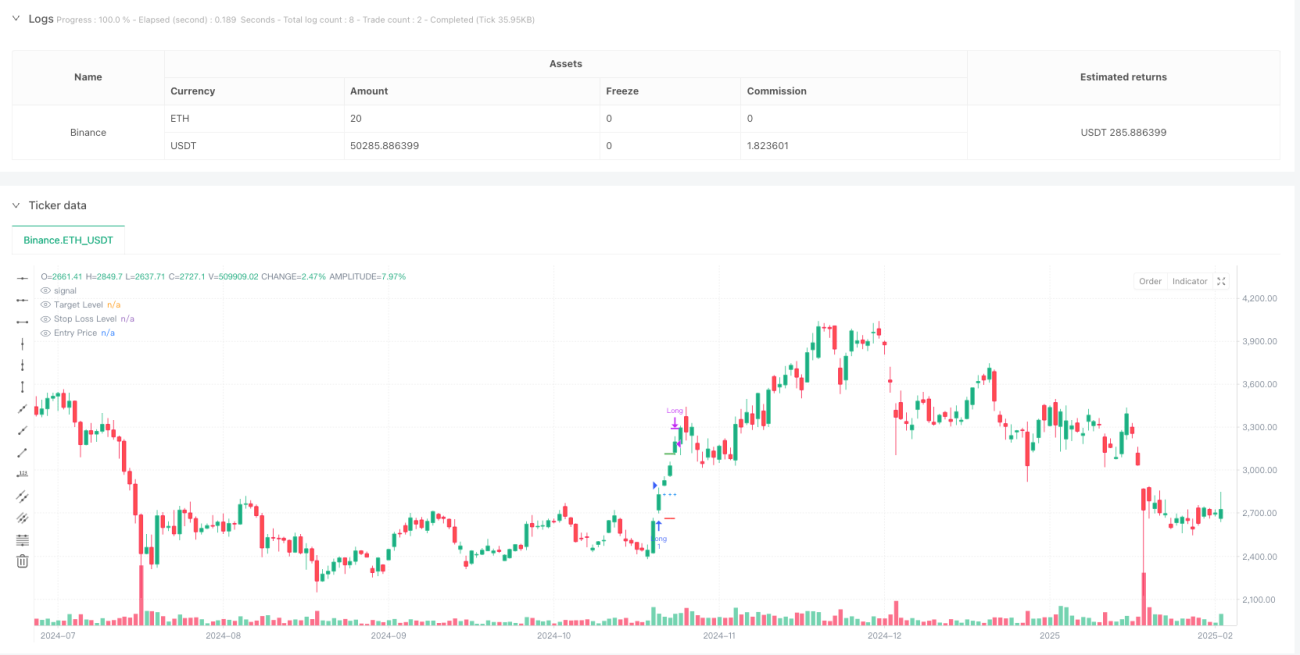

এই কৌশলটি একটি বহু প্রযুক্তিগত সূচক-ভিত্তিক ট্রেন্ড ট্র্যাকিং এবং মোমেন্টাম ট্রেডিং সিস্টেম। এটি প্রধানত এডিএক্স (ADX), আরএসআই (RSI) এবং এটিআর (ATR) একত্রিত করে সম্ভাব্য লং সুযোগ চিহ্নিত করে এবং এটিআর ব্যবহার করে গতিশীল লাভ ও স্টপ-লস স্তর নির্ধারণ করে। এই কৌশলটি বিশেষভাবে ১ মিনিটের সময়সীমার অপশন ট্রেডিংয়ের জন্য উপযোগী, কঠোর এন্ট্রি শর্ত এবং ঝুঁকি ব্যবস্থাপনার মাধ্যমে ট্রেডের সফলতার হার বৃদ্ধি করে।

কৌশল নীতি

কৌশলের মূল যুক্তি নিম্নলিখিত গুরুত্বপূর্ণ উপাদানগুলি অন্তর্ভুক্ত করে:

- ট্রেন্ড নিশ্চিতকরণ: ADX>18 এবং +DI -DI-এর চেয়ে বেশি হলে বাজার ঊর্ধ্বমুখী ট্রেন্ডে আছে তা নিশ্চিত করতে।

- মোমেন্টাম যাচাই: RSI ৬০ অতিক্রম করে এবং এর ২০-পিরিয়ড মুভিং এভারেজের উপরে থাকে, যা মূল্যের গতি যাচাই করে।

- এন্ট্রি সময়: যখন ট্রেন্ড এবং মোমেন্টাম উভয় শর্ত পূরণ হয়, তখন সিস্টেম বর্তমান ক্লোজিং মূল্যে লং পজিশন খোলে।

- লক্ষ্য ব্যবস্থাপনা: এন্ট্রির সময় ATR মানের ভিত্তিতে গতিশীল লাভ লক্ষ্য (২.৫ গুণ ATR) এবং স্টপ-লস (১.৫ গুণ ATR) নির্ধারণ করে।

কৌশলের সুবিধা

- বহুমাত্রিক নিশ্চিতকরণ: ট্রেন্ড এবং মোমেন্টাম সূচক একত্রিত করে আরও নির্ভরযোগ্য ট্রেডিং সিগন্যাল প্রদান করে।

- গতিশীল ঝুঁকি ব্যবস্থাপনা: ATR ব্যবহার করে লাভ ও স্টপ-লস স্তর গতিশীলভাবে সামঞ্জস্য করে, বাজারের অস্থিরতা পরিবর্তনের সাথে খাপ খাইয়ে নেয়।

- পরিষ্কার ট্রেডিং নিয়ম: এন্ট্রি এবং এক্সিট শর্ত স্পষ্ট, যা বিষয়গত সিদ্ধান্তের হস্তক্ষেপ কমায়।

- অভিযোজন ক্ষমতা: কৌশলের প্যারামিটারগুলি বিভিন্ন বাজার পরিবেশ এবং ট্রেডিং পণ্যের জন্য অপটিমাইজ করা যেতে পারে।

কৌশলের ঝুঁকি

- মিথ্যা ব্রেকআউট ঝুঁকি: RSI ৬০ অতিক্রম করলে মিথ্যা সংকেত আসতে পারে, তাই অন্যান্য সূচক দিয়ে যাচাই করা প্রয়োজন।

- স্লিপেজ প্রভাব: ১ মিনিটের দ্রুত বাজারে বড় স্লিপেজ ঝুঁকি হতে পারে।

- বাজার পরিবেশ নির্ভরতা: কৌশলটি স্পষ্ট ট্রেন্ডে ভালো কাজ করে, কিন্তু রেঞ্জবাউন্ড বাজারে ঘন ঘন স্টপ-লস ট্রিগার হতে পারে।

- প্যারামিটার সংবেদনশীলতা: একাধিক সূচক প্যারামিটার সেটিংস ভারসাম্যপূর্ণ হতে হবে, অন্যথায় কৌশলের কর্মক্ষমতা প্রভাবিত হতে পারে।

কৌশল অপটিমাইজেশনের দিকনির্দেশনা

- এন্ট্রি অপটিমাইজেশন: ভলিউম নিশ্চিতকরণ পদ্ধতি যোগ করে সিগন্যালের নির্ভরযোগ্যতা বাড়ানো যেতে পারে।

- পজিশন ম্যানেজমেন্ট: বাজারের অস্থিরতা অনুযায়ী পজিশনের আকার সামঞ্জস্য করার জন্য গতিশীল পজিশন ম্যানেজমেন্ট সিস্টেম অন্তর্ভুক্ত করা।

- এক্সিট মেকানিজম: ট্রেলিং স্টপ-লস ফিচার যোগ করে লাভ আরও ভালোভাবে সুরক্ষিত করা যেতে পারে।

- সময় ফিল্টার: ট্রেডিং সময় উইন্ডো ফিল্টার যোগ করে অতিরিক্ত অস্থিরতা বা কম তারল্যের সময় এড়ানো যায়।

সারসংক্ষেপ

এই কৌশলটি একাধিক প্রযুক্তিগত সূচকের সমন্বিত ব্যবহারের মাধ্যমে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করে। এর সুবিধা হলো ট্রেন্ড এবং মোমেন্টাম বিশ্লেষণ একত্রিত করা এবং গতিশীল ঝুঁকি ব্যবস্থাপনা পদ্ধতি ব্যবহার করা। যদিও কিছু ঝুঁকি রয়েছে, যুক্তিসঙ্গত প্যারামিটার অপটিমাইজেশন এবং ঝুঁকি নিয়ন্ত্রণ ব্যবস্থার মাধ্যমে বাস্তব ট্রেডিংয়ে স্থিতিশীল ফলাফল অর্জন সম্ভব। ট্রেডারদের লাইভ ট্রেডিংয়ের আগে কৌশলটি যথাযথভাবে ব্যাকটেস্ট এবং প্যারামিটার অপটিমাইজ করা উচিত এবং নির্দিষ্ট ট্রেডিং পণ্যের বৈশিষ্ট্য অনুযায়ী প্রয়োজনীয় সমন্বয় করা উচিত।

- 1