সারসংক্ষেপ

এটি একটি উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং কৌশল পদ্ধতি যা বোলিঞ্জার ব্যান্ড, ম্যাকডি (MACD) এবং ভলিউম বিশ্লেষণকে একত্রিত করে। এই কৌশলটি বোলিঞ্জার ব্যান্ডের উপরের এবং নিচের সীমানা থেকে মূল্যের ভেঙে যাওয়া এবং ফিরে আসা শনাক্ত করে, ম্যাকডি মোমেন্টাম সূচক এবং ভলিউম নিশ্চিতকরণের সাথে মিলিয়ে বাজারের উল্টানোর সুযোগগুলি ধরা দেয়। সিস্টেমটি প্রতিদিনের সর্বোচ্চ ট্রেড সংখ্যার সীমা নির্ধারণ করে এবং একটি সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা প্রক্রিয়া দিয়ে সজ্জিত।

কৌশলের নীতি

কৌশলটি প্রধানত নিম্নলিখিত তিনটি মূল সূচকের সমন্বয়ে ভিত্তি করে:

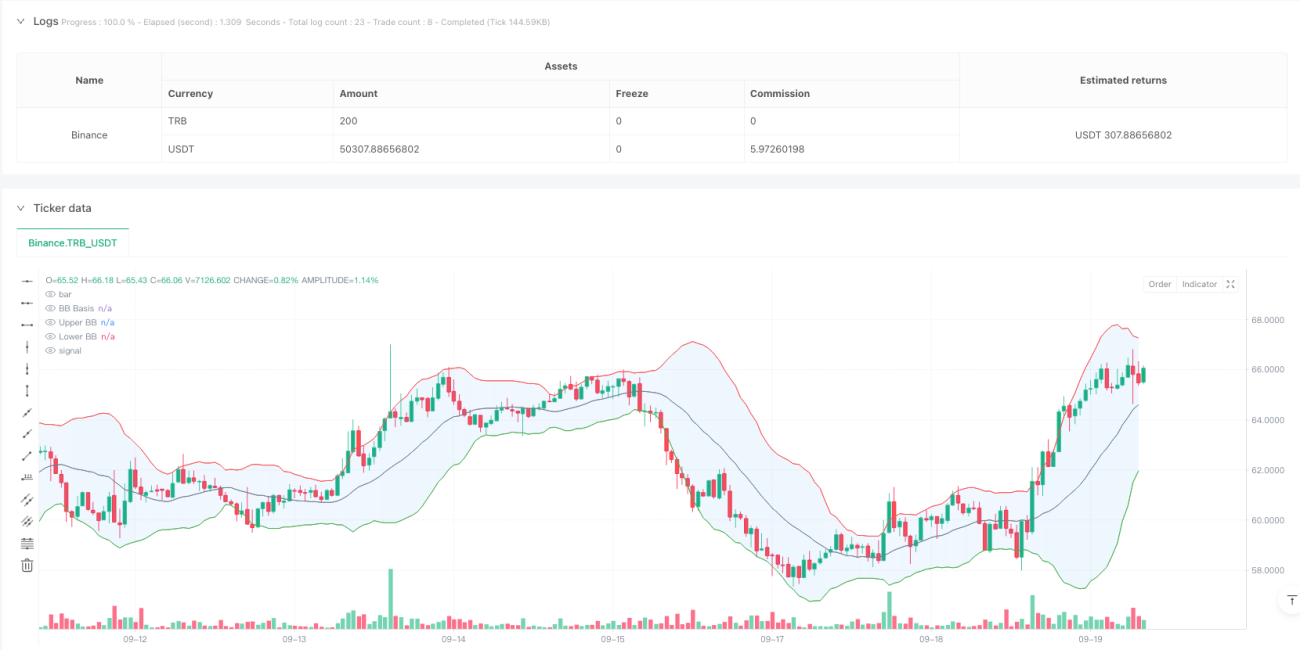

- বোলিঞ্জার ব্যান্ড সূচক: ২০ সময়কালের সরল গড় (SMA) মধ্যস্তর হিসেবে ব্যবহার করা হয়, স্ট্যান্ডার্ড বিচ্যুতি গুণক ২.০ দিয়ে উপরের এবং নিচের স্তর গণনা করা হয়। যখন মূল্য বোলিঞ্জার ব্যান্ড ভেঙে ফিরে আসে, সিস্টেম সম্ভাব্য ট্রেড সিগন্যাল জারি করে।

- ম্যাকডি সূচক: স্ট্যান্ডার্ড প্যারামিটার সেটিংস (১২, ২৬, ৯) ব্যবহার করা হয়, যা মূল্যের প্রবণতা মোমেন্টাম নিশ্চিত করে। যখন ম্যাকডি লাইন সিগন্যাল লাইনের উপরে থাকে তখন লং নিশ্চিত করা হয় এবং নিচে থাকলে শর্ট নিশ্চিত করা হয়।

- ভলিউম বিশ্লেষণ: ২০ সময়কালের গড় ব্যবহার করে ভলিউম নিশ্চিত করা হয়, সিগন্যাল উপস্থিত হওয়ার সময় ভলিউম কমপক্ষে গড় স্তরে থাকতে হবে, যাতে বাজারের অংশগ্রহণ নিশ্চিত হয়।

কৌশলের সুবিধা

- বহু-সিগন্যাল নিশ্চিতকরণ: বোলিঞ্জার ব্যান্ড, ম্যাকডি এবং ভলিউমের তিনটি যাচাইয়ের মাধ্যমে ট্রেড সিগন্যালের নির্ভরযোগ্যতা উল্লেখযোগ্যভাবে বৃদ্ধি পায়।

- দৃশ্যমান নকশা: সিস্টেমটি সমৃদ্ধ চার্ট নির্দেশক প্রদান করে, যার মধ্যে বোলিঞ্জার ব্যান্ড পূরণ, সিগন্যাল চিহ্নিতকরণ এবং পটভূমির রঙ পরিবর্তন অন্তর্ভুক্ত, যা ব্যবসায়ীদের দ্রুত ট্রেডিং সুযোগ শনাক্ত করতে সহায়তা করে।

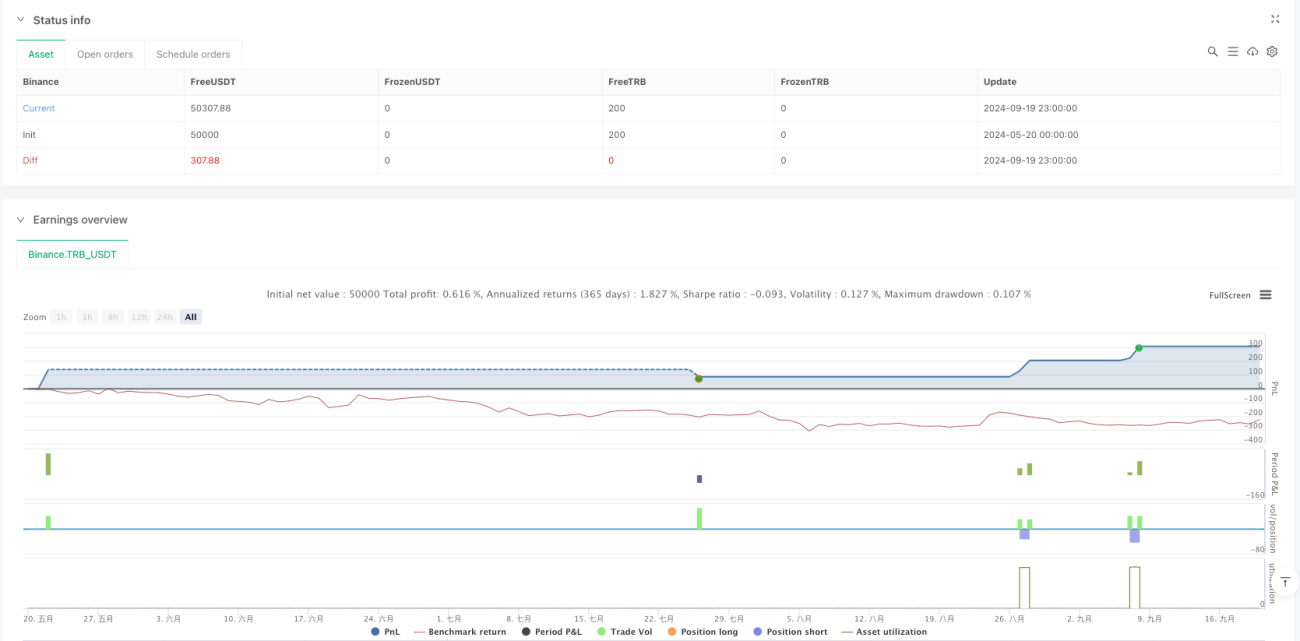

- সম্পূর্ণ ঝুঁকি নিয়ন্ত্রণ: নির্ধারিত স্টপ-লস এবং লাভ লক্ষ্য বাস্তবায়িত করা হয় এবং প্রতিদিনের সর্বোচ্চ ট্রেড সংখ্যা সীমাবদ্ধ করা হয়, কার্যকরভাবে ঝুঁকি এক্সপোজার নিয়ন্ত্রণ করে।

- সিস্টেমেটিক অপারেশন: কৌশলটি স্পষ্টভাবে প্রবেশ এবং প্রস্থানের শর্ত প্রদান করে, যা বিষয়ভিত্তিক সিদ্ধান্তের অনিশ্চয়তা হ্রাস করে।

কৌশলের ঝুঁকি

- বাজার ওঠানামার ঝুঁকি: উচ্চ-ওঠানামা বাজারে, ভুয়া ভেঙে যাওয়ার সিগন্যাল দেখা দিতে পারে, যা ট্রেড ক্ষতির কারণ হতে পারে।

- স্লিপেজ ঝুঁকি: উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং পরিবেশে, বড় স্লিপেজ খরচের সম্মুখীন হতে পারে, যা বাস্তব লাভকে প্রভাবিত করে।

- তারল্যের ঝুঁকি: ভলিউম শর্ত বাজারে পর্যাপ্ত তারল্য না থাকলে ট্রেডিং সুযোগ সীমাবদ্ধ করতে পারে।

- পদ্ধতিগত ঝুঁকি: নির্ধারিত প্যারামিটার সেটিংস বাজার অবস্থার তীব্র পরিবর্তনের সাথে খাপ খাইয়ে নিতে সক্ষম নাও হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশ

- প্যারামিটার গতিশীল অপ্টিমাইজেশন: স্বয়ংক্রিয় প্যারামিটার সমন্বয় প্রক্রিয়া চালু করা যেতে পারে, যাতে বোলিঞ্জার ব্যান্ড এবং ম্যাকডি প্যারামিটারগুলি বাজার অবস্থার ভিত্তিতে স্বয়ংক্রিয়ভাবে সামঞ্জস্য করতে পারে।

- বাজার চক্র শনাক্তকরণ: বাজার চক্র বিচার মডিউল যুক্ত করা, বিভিন্ন বাজার চক্রে ভিন্ন ট্রেডিং কৌশল গ্রহণ করা।

- ঝুঁকি ব্যবস্থাপনা অপ্টিমাইজেশন: গতিশীল স্টপ-লস প্রক্রিয়া চালু করার কথা বিবেচনা করা যেতে পারে, বাজার ওঠানামার ভিত্তিতে স্টপ-লস অবস্থান সমন্বয় করা।

- সিগন্যাল ফিল্টারিং বৃদ্ধি: প্রবণতা শক্তি ফিল্টার যুক্ত করা, যাতে পাশের বাজারে অতিরিক্ত ট্রেড সিগন্যাল তৈরি না হয়।

সারসংক্ষেপ

এই কৌশলটি বোলিঞ্জার ব্যান্ড রিভার্সাল সিগন্যাল, ম্যাকডি প্রবণতা নিশ্চিতকরণ এবং ভলিউম যাচাইয়ের সমন্বয়ে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করে। সিস্টেমের দৃশ্যমান নকশা এবং কঠোর ঝুঁকি নিয়ন্ত্রণ এটিকে বিশেষভাবে দৈনন্দিন ট্রেডিংয়ের জন্য উপযুক্ত করে তোলে। যদিও কিছু বাজার ঝুঁকি বিদ্যমান, ধারাবাহিক অপ্টিমাইজেশন এবং প্যারামিটার সমন্বয়ের মাধ্যমে কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল পারফরম্যান্স বজায় রাখতে সক্ষম হতে পারে।

- 1