সারসংক্ষেপ

এই কৌশলটি কাউফম্যান অ্যাডাপ্টিভ মুভিং এভারেজ (KAMA) এবং MACD-র উপর ভিত্তি করে একটি ট্রেন্ড ফলোয়িং সিস্টেম। এটি KAMA-কে প্রধান ট্রেন্ড সনাক্তকারী নির্দেশক হিসাবে ব্যবহার করে, এবং MACD-কে মুভমেন্টাম নিশ্চিতকারী নির্দেশক হিসাবে যুক্ত করে, বাজারের ট্রেন্ডের বুদ্ধিমান ট্র্যাকিং এবং ট্রেডিং সময়ের সঠিক সন্ধান নিশ্চিত করে। এই কৌশলটি ৪ ঘণ্টার টাইমফ্রেমে কাজ করে, এবং ঝুঁকি ব্যবস্থাপনার জন্য ডাইনামিক স্টপ-লস ও লাভের লক্ষ্য ব্যবহার করে।

কৌশলের মূলনীতি

কৌশলের মূল লজিক নিম্নলিখিত মূল উপাদানগুলির উপর ভিত্তি করে:

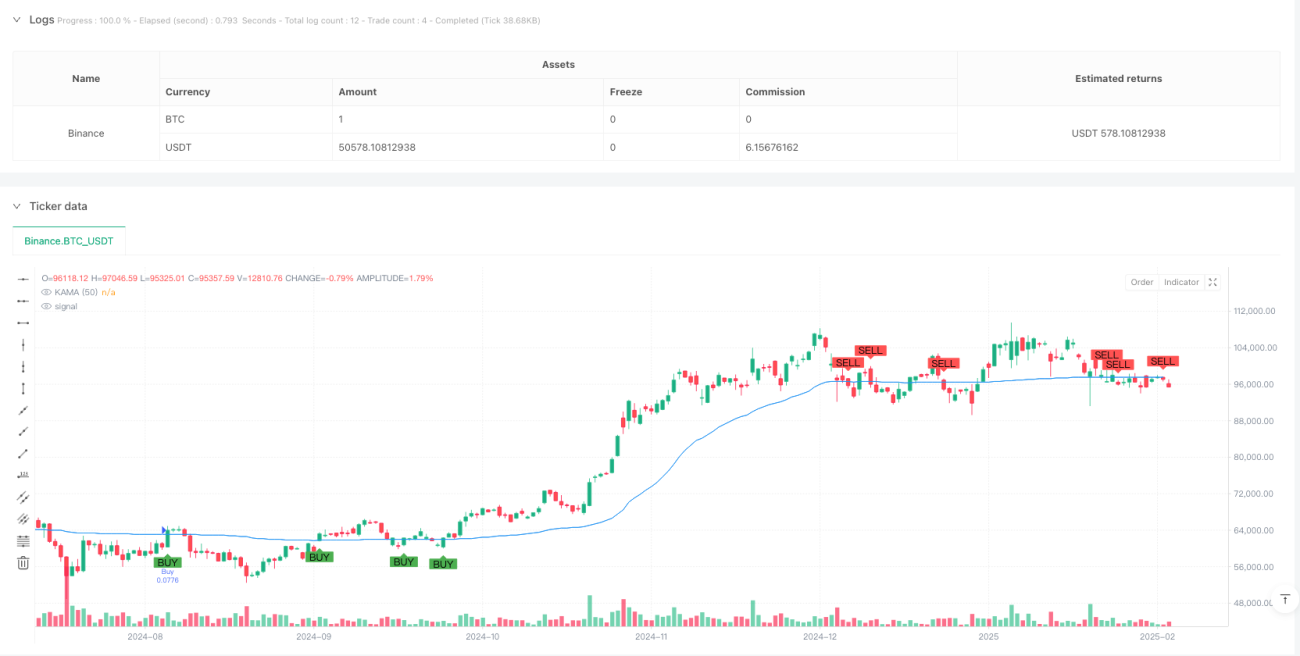

- KAMA গণনা: ৫০ পিরিয়ডের KAMA প্রধান ট্রেন্ড নির্দেশক হিসাবে ব্যবহৃত হয়, যা দক্ষতা অনুপাতের মাধ্যমে স্মুথিং কনস্ট্যান্ট ডাইনামিকভাবে সামঞ্জস্য করে, যাতে মুভিং এভারেজ বাজারের অবস্থার সাথে আরও ভালভাবে খাপ খাইয়ে নিতে পারে।

- MACD নিশ্চিতকরণ: ধীর সেটিংস (২৬, ৫২, ১৮) সহ MACD ট্রেন্ড নিশ্চিত করার সরঞ্জাম হিসাবে ব্যবহৃত হয়, যাতে ট্রেডের দিক সামগ্রিক মুভমেন্টামের সাথে সামঞ্জস্যপূর্ণ থাকে।

- ATR স্টপ-লস: ১৪ পিরিয়ডের ATR-এর ৩ গুণ ডাইনামিক স্টপ-লস এবং লাভের লক্ষ্য গণনার ভিত্তি হিসাবে ব্যবহৃত হয়।

- ট্রেডিং নিয়ম:

- লং করার শর্ত: মূল্য KAMA-কে উপরে ক্রস করে এবং MACD বুলিশ অবস্থায় থাকে

- বন্ধ করার শর্ত: মূল্য KAMA-কে নিচে ক্রস করে এবং MACD বিয়ারিশ অবস্থায় থাকে

- ঝুঁকি ব্যবস্থাপনা: ATR-এর ভিত্তিতে ডাইনামিক স্টপ-লস এবং লাভের লক্ষ্য নির্ধারণ

কৌশলের সুবিধা

- অভিযোজন ক্ষমতা: KAMA বাজারের দক্ষতার উপর ভিত্তি করে স্বয়ংক্রিয়ভাবে সংবেদনশীলতা সামঞ্জস্য করতে পারে, বিভিন্ন বাজার পরিবেশে ভাল পারফরম্যান্স বজায় রাখে।

- সংকেত নির্ভরযোগ্যতা: MACD নিশ্চিতকরণ মিথ্যা ব্রেকআউটের ঝুঁকি উল্লেখযোগ্যভাবে হ্রাস করে।

- ঝুঁকি ব্যবস্থাপনা সম্পূর্ণ: অস্থিরতার উপর ভিত্তি করে ডাইনামিক স্টপ-লস এবং লাভের লক্ষ্য ঝুঁকি ব্যবস্থাপনাকে আরও অভিযোজিত করে তোলে।

- প্যারামিটার অপ্টিমাইজেশনের সুযোগ: মূল প্যারামিটারগুলি বিভিন্ন বাজারের বৈশিষ্ট্য অনুসারে সামঞ্জস্য করা যেতে পারে।

কৌশলের ঝুঁকি

- ট্রেন্ড বিপরীতের ঝুঁকি: অত্যন্ত অস্থির বাজারে অনেক মিথ্যা সংকেত দেখা দিতে পারে।

- ল্যাগ ঝুঁকি: KAMA এবং MACD উভয়েরই কিছুটা ল্যাগ থাকে, ফলে সেরা প্রবেশের সময় মিস হতে পারে।

- প্যারামিটার সংবেদনশীলতা: বিভিন্ন বাজার অবস্থায় কৌশলের কার্যকারিতা বজায় রাখতে প্যারামিটার সমন্বয়ের প্রয়োজন হতে পারে।

- ট্রেডিং খরচের প্রভাব: ঘন ঘন ট্রেডিংয়ের ফলে উচ্চ ট্রেডিং খরচ হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- বাজারের অস্থিরতা ফিল্টার চালু করুন, উচ্চ অস্থিরতার পরিবেশে কৌশলের প্যারামিটার সমন্বয় করুন বা ট্রেডিং বন্ধ করুন।

- ভলিউম বিশ্লেষণ নির্দেশক যুক্ত করুন, ট্রেন্ড সনাক্তকরণের নির্ভুলতা বাড়ান।

- MACD প্যারামিটার সেটিংস অপ্টিমাইজ করুন, যাতে এটি ৪ ঘণ্টার টাইমফ্রেমের জন্য আরও উপযুক্ত হয়।

- অভিযোজিত স্টপ-লস গুণক বাস্তবায়ন করুন, বাজারের অস্থিরতার উপর ভিত্তি করে ATR গুণক ডাইনামিকভাবে সামঞ্জস্য করুন।

- সময় ফিল্টার যুক্ত করুন, কম তারল্যের সময় ট্রেডিং এড়িয়ে চলুন।

উপসংহার

এটি একটি ট্রেন্ড ফলোয়িং কৌশল যা ক্লাসিক টেকনিক্যাল ইন্ডিকেটর KAMA এবং MACD-কে উদ্ভাবনীভাবে একত্রিত করে। অভিযোজিত মুভিং এভারেজ এবং মুভমেন্টাম নিশ্চিতকরণের সমন্বয়, এবং সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা সিস্টেমের মাধ্যমে, এই কৌশলটি শক্তিশালী ব্যবহারিকতা এবং স্থিতিশীলতা প্রদর্শন করে। যদিও কিছুটা ল্যাগ এবং প্যারামিটার সংবেদনশীলতার ঝুঁকি রয়েছে, প্রস্তাবিত অপ্টিমাইজেশনের দিকনির্দেশনা অনুসরণ করে কৌশলটির দৃঢ়তা এবং লাভজনকতা আরও বাড়ানো যেতে পারে।

- 1