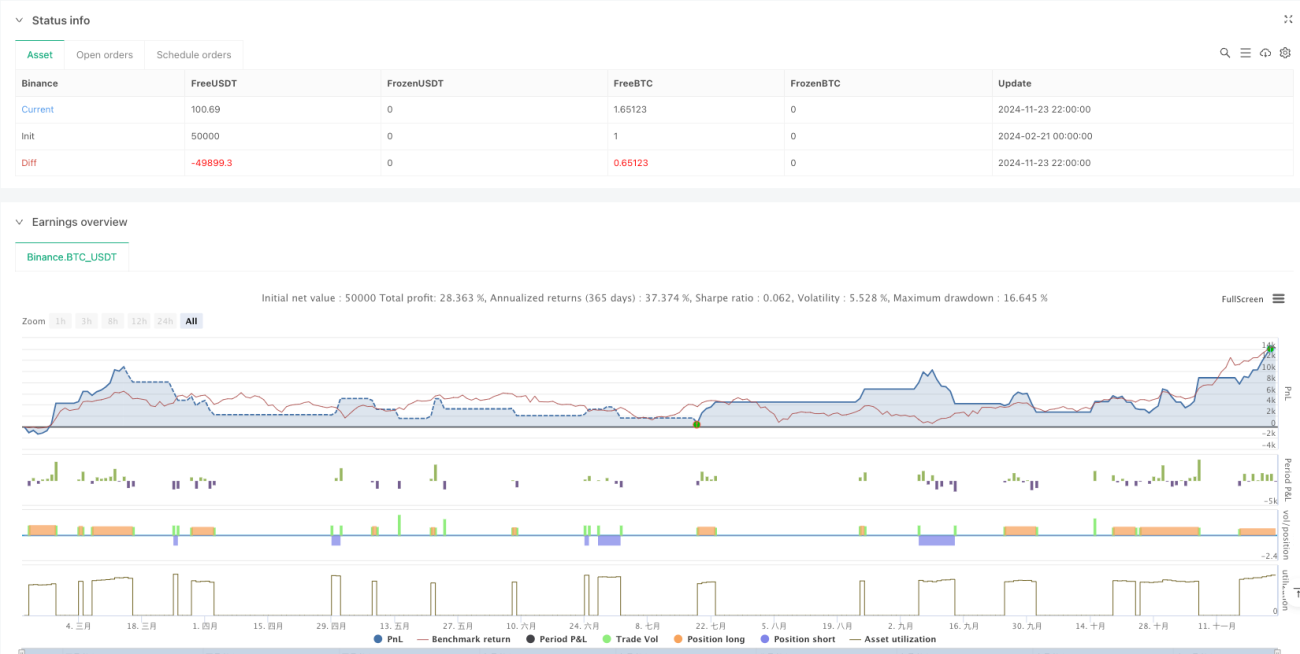

সংক্ষিপ্ত বিবরণ

এটি একটি ট্রেডিং কৌশল যা ভলিউম ওয়েটেড এভারেজ প্রাইস (VWAP) এবং মাল্টি-পিরিয়ড এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA) কে একত্রিত করে। কৌশলটি মূলত ইন্ট্রাডে ট্রেডিংয়ের জন্য ব্যবহৃত হয়, বিশেষ করে ১৫ মিনিটের টাইমফ্রেমের জন্য উপযুক্ত। কৌশলটি দাম এবং VWAP ও বিভিন্ন পিরিয়ডের EMA-এর মধ্যে সম্পর্ক বিশ্লেষণ করে, ভলিউম তথ্যের সাথে মিলিয়ে বাজারের ট্রেন্ড এবং ট্রেডিং সুযোগ নির্ধারণ করে।

কৌশলের নীতি

কৌশলটি ১০-পিরিয়ড, ২০-পিরিয়ড এবং ২০০-পিরিয়ডের EMA, এবং VWAP কে মূল সূচক হিসেবে ব্যবহার করে। ট্রেডিং সিগন্যাল নিম্নলিখিত শর্তের ভিত্তিতে তৈরি হয়:

- লং এন্ট্রি শর্ত: দাম একইসাথে VWAP, ২০০EMA, ১০EMA এবং ২০EMA-এর উপরে থাকতে হবে; বর্তমান ক্যান্ডেলের ক্লোজিং প্রাইস ওপেনিং প্রাইসের উপরে হতে হবে; VWAP ২০০EMA-এর উপরে অবস্থান করতে হবে; ১০EMA ২০EMA-এর উপরে এবং ২০EMA VWAP-এর উপরে অবস্থান করতে হবে।

- শর্ট এন্ট্রি শর্ত: লং-এর বিপরীত শর্তের সমন্বয়।

- স্টপ-লস সেটিং: আগের ১০টি ক্যান্ডেলের সর্বনিম্ন পয়েন্ট (লং-এর জন্য) বা সর্বোচ্চ পয়েন্ট (শর্ট-এর জন্য) সাথে ATR মান যোগ/বিয়োগ করে নির্ধারণ করা হয়।

- লাভের লক্ষ্য: ১:২ এবং ১:৩ রিস্ক-রিওয়ার্ড রেশিও ব্যবহার করে দুটি টার্গেট পয়েন্ট নির্ধারণ করা হয়।

কৌশলের সুবিধা

- একাধিক নিশ্চিতকরণ প্রক্রিয়া: একাধিক প্রযুক্তিগত সূচকের সমন্বিত ব্যবহার ট্রেডিং সিগন্যালের নির্ভরযোগ্যতা বৃদ্ধি করে।

- গতিশীল ঝুঁকি ব্যবস্থাপনা: ATR-ভিত্তিক গতিশীল স্টপ-লস বাজারের অস্থিরতার পরিবর্তনের সাথে খাপ খাইয়ে নিতে সক্ষম।

- স্পষ্ট লাভের লক্ষ্য: নির্দিষ্ট রিস্ক-রিওয়ার্ড রেশিও ব্যবহার করে ট্রেডারদের ঝুঁকি নিয়ন্ত্রণ সহজ হয়।

- ট্রেন্ড ট্র্যাকিং এবং মোমেন্টামের সংমিশ্রণ: বিভিন্ন পিরিয়ডের মুভিং এভারেজের সমন্বয় দীর্ঘমেয়াদী ট্রেন্ড ধরতে এবং স্বল্পমেয়াদী সুযোগগুলি মিস না করতে সাহায্য করে।

কৌশলের ঝুঁকি

- ল্যাগিং ঝুঁকি: EMA এবং VWAP উভয়ই ল্যাগিং সূচক, বাজারের দ্রুত পরিবর্তনের সময় সময়মতো প্রতিক্রিয়া জানাতে পারে না।

- রেঞ্জবাউন্ড বাজারের ঝুঁকি: সমতলীকরণের পর্যায়ে অত্যধিক মিথ্যা ব্রেকআউট সিগন্যাল তৈরি হতে পারে।

- মূলধন ব্যবস্থাপনার ঝুঁকি: নির্দিষ্ট রিস্ক-রিওয়ার্ড রেশিও সব বাজারের পরিবেশের জন্য উপযুক্ত নাও হতে পারে।

- ট্রেডিং খরচের প্রভাব: ঘন ঘন ট্রেডিংয়ের ফলে উচ্চ ট্রেডিং খরচ হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- অস্থিরতা ফিল্টার সংযোজন: কম অস্থিরতার পরিবেশে ট্রেডিং এড়াতে ATR শতাংশ থ্রেশহোল্ড যুক্ত করা যেতে পারে।

- সময় ফিল্টার অপ্টিমাইজেশন: বিভিন্ন বাজারের বৈশিষ্ট্য অনুযায়ী সর্বোত্তম ট্রেডিং সময় নির্ধারণ করা যেতে পারে।

- গতিশীল রিস্ক-রিওয়ার্ড রেশিও: বাজারের অস্থিরতার ভিত্তিতে লাভের লক্ষ্য গতিশীলভাবে সমন্বয় করা।

- ভলিউম নিশ্চিতকরণ যোগ করা: ব্রেকআউটের নির্ভরযোগ্যতা বাড়াতে সর্বনিম্ন ভলিউম থ্রেশহোল্ড নির্ধারণ করা যেতে পারে।

উপসংহার

কৌশলটি একাধিক প্রযুক্তিগত সূচক একত্রিত করে একটি সম্পূর্ণ ট্রেডিং সিস্টেম তৈরি করে। কৌশলের প্রধান সুবিধা হল একাধিক নিশ্চিতকরণ প্রক্রিয়া এবং একটি সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা ব্যবস্থা। কিছু ল্যাগিং ঝুঁকি থাকলেও, প্রস্তাবিত অপ্টিমাইজেশন দিকনির্দেশনার মাধ্যমে কৌশলের স্থিতিশীলতা এবং লাভজনকতা আরও বাড়ানো যেতে পারে। কৌশলটি বিশেষ করে ইন্ট্রাডে ট্রেডারদের জন্য উপযুক্ত, তবে নির্দিষ্ট বাজারের বৈশিষ্ট্য অনুযায়ী প্যারামিটার অপ্টিমাইজেশন প্রয়োজন।

- 1