সংক্ষিপ্ত বিবরণ

কৌশলটি একটি ট্রেডিং সিস্টেম যা কোয়ান্টাম নির্ভুলতা এবং একাধিক প্রযুক্তিগত সূচককে একত্রিত করে, বহুস্তরীয় ট্রেন্ড নিশ্চিতকরণ এবং ঝুঁকি ব্যবস্থাপনার মাধ্যমে শক্তিশালী ট্রেডিং নিশ্চিত করে। কৌশলটি মোমেন্টাম সূচক, অস্থিরতা বিশ্লেষণ, ট্রেন্ড শক্তি এবং বাজার মনোভাবের মতো বহুমাত্রিক বিশ্লেষণকে একীভূত করে, যা একটি সম্পূর্ণ ট্রেডিং সিদ্ধান্ত গ্রহণ ব্যবস্থা গঠন করে।

কৌশল নীতি

কৌশলটি বহুস্তরীয় ট্রেড সিগন্যাল নিশ্চিতকরণ পদ্ধতি ব্যবহার করে:

- ATR (গড় সত্যিকারের পরিসর) ব্যবহার করে গতিশীল স্টপ-লস এবং লাভের লক্ষ্য নির্ধারণ

- মোমেন্টাম সূচক, অস্থিরতা এবং ট্রেন্ড শক্তির ত্রি-স্তরীয় যাচাই করে নিশ্চিতকরণ সংকেত তৈরি

- ১০ এবং ৩০ পিরিয়ডের EMA ক্রসপয়েন্টে ট্রেড করা

- নিউরাল অ্যাডাপটিভ ট্রেন্ড লাইন এবং AI বাজার মনোভাব সূচক ব্যবহার করে ট্রেন্ড অনুসরণ

- ৩:১ ঝুঁকি-পুরস্কার অনুপাত ব্যবহার করে মূলধন ব্যবস্থাপনা অপ্টিমাইজ করা

কৌশলের সুবিধা

- বহুমাত্রিক সিগন্যাল যাচাইকরণ ব্যবস্থা মিথ্যা ব্রেকআউটের ঝুঁকি ব্যাপকভাবে হ্রাস করে

- গতিশীল স্টপ-লস সেটিং বিভিন্ন বাজার পরিবেশের সাথে খাপ খায়

- নিউরাল অ্যাডাপটিভ ট্রেন্ড লাইন আরও নির্ভুল ট্রেন্ড দিকনির্দেশনা প্রদান করে

- AI বাজার মনোভাব সূচক বাজারবোধ বৃদ্ধি করে

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা ব্যবস্থা মূলধনের নিরাপত্তা নিশ্চিত করে

- কৌশলের যুক্তি পরিষ্কার, রক্ষণাবেক্ষণ ও অপ্টিমাইজেশন সহজ

কৌশলের ঝুঁকি

- একাধিক নিশ্চিতকরণ পদ্ধতি এন্ট্রি সিগন্যালে পিছিয়ে যাওয়ার কারণ হতে পারে

- উচ্চ অস্থিরতার বাজারে ঘন ঘন স্টপ-লস ট্রিগার হতে পারে

- বাজারের আকস্মিক পরিবর্তনের সময় গতিশীল স্টপ-লস যথেষ্ট দ্রুত নাও হতে পারে

- প্যারামিটার অপ্টিমাইজেশনের জন্য বড় নমুনা ডেটা প্রয়োজন

- গণনাগত জটিলতা বেশি, যা সম্পাদনের গতিকে প্রভাবিত করতে পারে

কৌশল অপ্টিমাইজেশনের দিকনির্দেশ

- অভিযোজিত প্যারামিটার অপ্টিমাইজেশন সিস্টেম চালু করা, বাজার অবস্থা অনুযায়ী সূচক প্যারামিটার গতিশীলভাবে সামঞ্জস্য করা

- বাজারের অস্থিরতা ফিল্টার যুক্ত করা, চরম বাজার পরিবেশে স্বয়ংক্রিয়ভাবে পজিশন সামঞ্জস্য করা

- নিশ্চিতকরণ সিগন্যাল উৎপাদনের যুক্তি অপ্টিমাইজ করে সিগন্যাল ল্যাগ কমানো

- মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে বাজার মনোভাব সূচক অপ্টিমাইজ করা

- ট্রেডিং খরচ বিবেচনায় নিয়ে ট্রেডিং ফ্রিকোয়েন্সি অপ্টিমাইজ করা

সারসংক্ষেপ

এটি একটি সম্পূর্ণ ট্রেডিং সিস্টেম যা ঐতিহ্যবাহী প্রযুক্তিগত বিশ্লেষণ এবং আধুনিক কোয়ান্টাম পদ্ধতির সমন্বয়। বহুস্তরীয় সিগন্যাল নিশ্চিতকরণ এবং ঝুঁকি ব্যবস্থাপনার মাধ্যমে কৌশলটি স্থিতিশীলতা বজায় রাখার পাশাপাশি ভালো অভিযোজন ক্ষমতা প্রদর্শন করে। যদিও অপ্টিমাইজেশনের সুযোগ রয়েছে, সামগ্রিক কাঠামোটি যুক্তিসঙ্গত এবং দীর্ঘমেয়াদী বাস্তব ট্রেডিংয়ের জন্য উপযুক্ত। ক্রমাগত অপ্টিমাইজেশন ও উন্নতির মাধ্যমে এই কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল পারফরম্যান্স বজায় রাখার সম্ভাবনা রাখে।

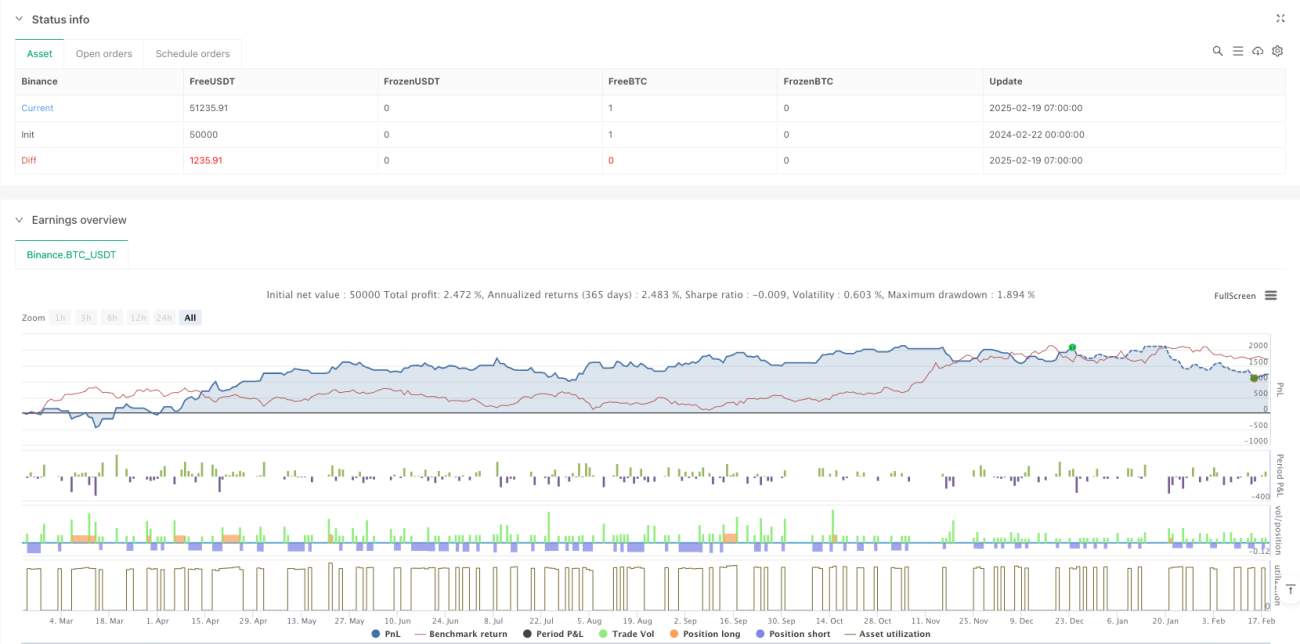

/*backtest

start: 2024-02-22 00:00:00

end: 2025-02-19 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Quantum Precision Forex Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input parameters- 1