সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি ট্রেন্ড ফলোয়িং সিস্টেম, যা একাধিক মুভিং এভারেজ, মোমেন্টাম ইন্ডিকেটর এবং ডায়নামিক রিস্ক কন্ট্রোলকে একত্রিত করে। কৌশলটি মূল্য প্রবণতা, বাজার মোমেন্টাম এবং অস্থিরতা বিশ্লেষণের মাধ্যমে ট্রেডিং সুযোগ চিহ্নিত করে, এবং কঠোর পজিশন ম্যানেজমেন্ট ও স্টপ-লস মেকানিজম প্রয়োগ করে ঝুঁকি নিয়ন্ত্রণ করে। মূল যুক্তিটি স্বল্প ও দীর্ঘমেয়াদী এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA) এর ক্রসওভার এবং রিলেটিভ স্ট্রেংথ ইনডেক্স (RSI) এর সমন্বয়ে কাজ করে, যেখানে অ্যাভারেজ ট্রু রেঞ্জ (ATR) ব্যবহার করে স্টপ-লস অবস্থান গতিশীলভাবে নির্ধারণ করা হয়।

কৌশল পদ্ধতি

কৌশলটি ট্রেডিং সংকেত নিশ্চিত করতে একটি বহু-স্তর যাচাই প্রক্রিয়া ব্যবহার করে:

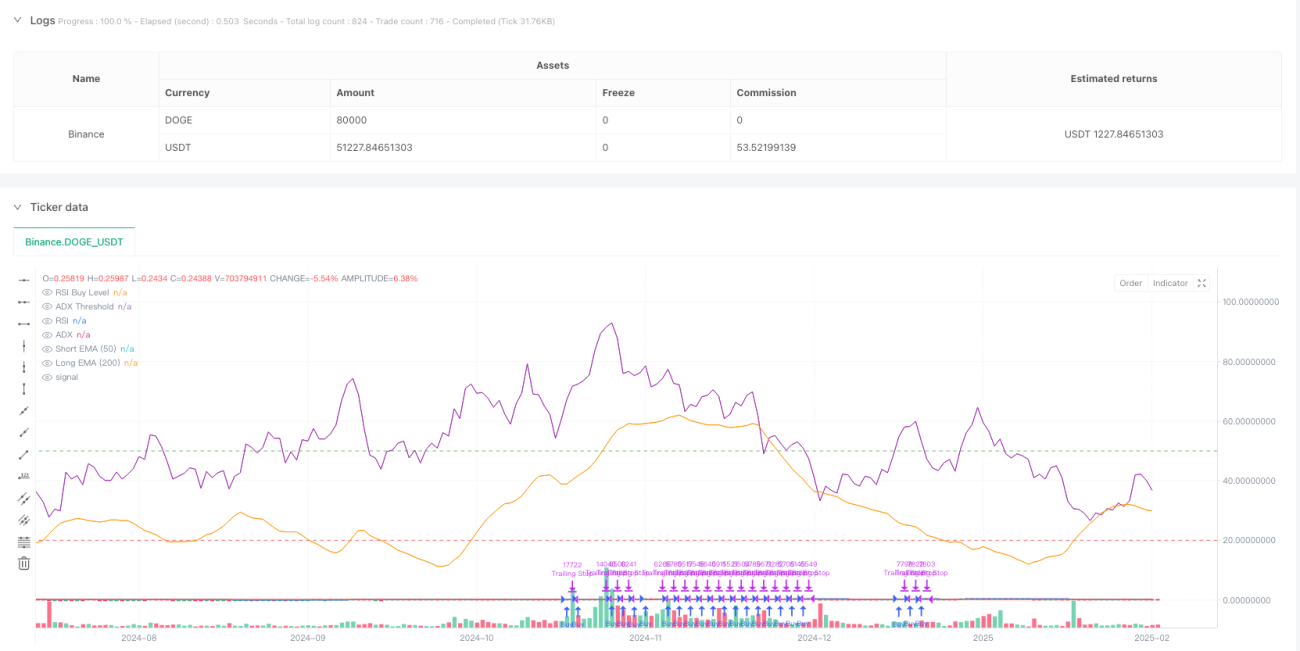

- ট্রেন্ড নিশ্চিতকরণ: মাঝারি ও দীর্ঘমেয়াদী ট্রেন্ড বিচারের জন্য ৫০ দিন ও ২০০ দিনের EMA ব্যবহার করা হয়, যেখানে স্বল্পমেয়াদী গড়কে দীর্ঘমেয়াদী গড়ের উপরে ১০ টিরও বেশি সময় ধরে থাকতে হবে।

- মোমেন্টাম যাচাই: RSI দিয়ে মূল্য মোমেন্টাম যাচাই করা হয়; যখন RSI নির্ধারিত থ্রেশহোল্ড (ডিফল্ট ৫০) অতিক্রম করে, তখন ঊর্ধ্বমুখী মোমেন্টাম নিশ্চিত হয়।

- ট্রেন্ড শক্তি: অ্যাভারেজ ডাইরেকশনাল ইনডেক্স (ADX) ট্রেন্ড শক্তি পরিমাপের জন্য অন্তর্ভুক্ত করা হয়; ADX ২০ এর উপরে থাকলে তা উল্লেখযোগ্য ট্রেন্ড নির্দেশ করে।

- ডায়নামিক রিস্ক কন্ট্রোল: ATR-এর ভিত্তিতে ডায়নামিক স্টপ-লস ডিজাইন করা হয়; স্টপ-লস দূরত্ব ATR-এর ২.৫ গুণ নির্ধারণ করা হয় এবং ট্রেলিং স্টপ মেকানিজমও অন্তর্ভুক্ত থাকে।

- বুদ্ধিমান পজিশন ম্যানেজমেন্ট: অ্যাকাউন্ট ইক্যুইটি এবং পূর্বনির্ধারিত ঝুঁকি অনুপাতের ভিত্তিতে ATR-এর সাথে সমন্বয় করে গতিশীলভাবে খোলা অবস্থানের সংখ্যা গণনা করা হয়।

কৌশলের সুবিধা

- বহু-সংকেত যাচাই: মুভিং এভারেজ, মোমেন্টাম এবং ট্রেন্ড শক্তি-সহ একাধিক মাত্রার সংকেত যাচাইয়ের মাধ্যমে নির্ভরযোগ্যতা বৃদ্ধি পায়।

- ডায়নামিক রিস্ক ম্যানেজমেন্ট: অস্থিরতার উপর ভিত্তি করে গতিশীল এবং ট্রেলিং স্টপ ব্যবহার করা হয়, যা বাজার পরিস্থিতি অনুযায়ী নিজেকে খাপ খাইয়ে নেয়।

- বুদ্ধিমান পজিশন কন্ট্রোল: অ্যাকাউন্টের আকার এবং বাজার অস্থিরতার ভিত্তিতে গতিশীলভাবে পজিশন সমন্বয় করে, একক ট্রেডের ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করে।

- ট্রেন্ড স্থায়িত্বের প্রয়োজনীয়তা: ট্রেন্ড সময়কালের প্রয়োজনীয়তা নির্ধারণ করে মিথ্যা ব্রেকআউট এড়ানো যায়।

- পদ্ধতিগত ট্রেডিং সতর্কতা: রিয়েল-টাইম অপারেশনের জন্য ট্রেডিং সিগন্যাল নোটিফিকেশন একীভূত করা হয়েছে।

কৌশলের ঝুঁকি

- ট্রেন্ড রিভার্সাল ঝুঁকি: শক্তিশালী ট্রেন্ড শেষে বড় ড্রডাউন হতে পারে; বাজার ম্যাক্রো পরিস্থিতির সাথে সমন্বয় করার পরামর্শ দেওয়া হয়।

- পার্শ্ববর্তী বাজারে পারফরম্যান্স: রেঞ্জবাউন্ড বাজারে ঘন ঘন ট্রেড তৈরি হতে পারে, যা ট্রেডিং খরচ বাড়ায়।

- প্যারামিটার সংবেদনশীলতা: একাধিক ইন্ডিকেটর প্যারামিটারের সেটিং কৌশল কর্মক্ষমতাকে প্রভাবিত করে; ব্যাকটেস্ট অপ্টিমাইজেশন প্রয়োজন।

- স্লিপেজ প্রভাব: কম তারল্যের বাজারে বড় স্লিপেজের সম্মুখীন হতে পারে, যা কৌশলের রিটার্নকে প্রভাবিত করে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- বাজার পরিবেশ অভিযোজন: বিভিন্ন বাজার পরিবেশে অভিযোজন ক্ষমতা বাড়ানোর জন্য অস্থিরতা সূচক (যেমন VIX) অন্তর্ভুক্ত করে কৌশল প্যারামিটার গতিশীলভাবে সমন্বয় করা যেতে পারে।

- সংকেত ফিল্টারিং: সংকেত মান উন্নত করার জন্য ভলিউম ইন্ডিকেটর যাচাই যোগ করা যেতে পারে।

- লাভ গ্রহণ প্রক্রিয়া: বাজার ওঠানামার উপর ভিত্তি করে গতিশীল লাভ গ্রহণ প্রক্রিয়া ডিজাইন করে রিটার্ন-ড্রডাউন অনুপাত অপ্টিমাইজ করা যেতে পারে।

- সময় চক্র অপ্টিমাইজেশন: বিভিন্ন সময় চক্রে সংকেত ধারাবাহিকতা যাচাই করে ট্রেডিং স্থিতিশীলতা বৃদ্ধি করা যেতে পারে।

- মেশিন লার্নিং অপ্টিমাইজেশন: অভিযোজন ক্ষমতা বাড়ানোর জন্য মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে প্যারামিটার গতিশীলভাবে অপ্টিমাইজ করা যেতে পারে।

সারাংশ

এই কৌশলটি একাধিক প্রযুক্তিগত সূচকের সমন্বিত ব্যবহারের মাধ্যমে একটি সম্পূর্ণ ট্রেন্ড ফলোয়িং ট্রেডিং সিস্টেম তৈরি করেছে। কৌশলটি ঝুঁকি নিয়ন্ত্রণে উৎকর্ষ প্রদর্শন করে; গতিশীল স্টপ-লস এবং পজিশন ম্যানেজমেন্টের মাধ্যমে ড্রডাউন কার্যকরভাবে নিয়ন্ত্রণ করা হয়। কৌশলটির সম্প্রসারণযোগ্যতা বেশি এবং একাধিক অপ্টিমাইজেশনের দিকনির্দেশনা রয়েছে। বাস্তব ট্রেডিংয়ে ব্যবহারের সময়, নির্দিষ্ট বাজার বৈশিষ্ট্য এবং নিজের ঝুঁকি সহনশীলতা অনুযায়ী প্যারামিটার সামঞ্জস্য করার পরামর্শ দেওয়া হয়।

অপ্টিমাইজেশন নির্দেশনা

- বাজার পরিবেশের সাথে মানিয়ে নেওয়া: গতিশীল প্যারামিটার সামঞ্জস্যের জন্য ভোলাটিলিটি সূচক (যেমন VIX) ব্যবহারের কথা বিবেচনা করুন, যাতে বিভিন্ন বাজার অবস্থায় অভিযোজন ক্ষমতা বৃদ্ধি পায়।

- সিগন্যাল ফিল্টারিং: সিগন্যালের গুণমান উন্নত করতে ভলিউম সূচক যাচাই যোগ করার কথা বিবেচনা করুন।

- মুনাফা তোলার পদ্ধতি: রিটার্ন-টু-ড্রডাউন অনুপাত অপ্টিমাইজ করতে বাজার ভোলাটিলিটির ভিত্তিতে গতিশীল মুনাফা তোলার পদ্ধতি ডিজাইন করুন।

- টাইমফ্রেম অপ্টিমাইজেশন: ট্রেডিং স্থিতিশীলতা উন্নত করতে বিভিন্ন টাইমফ্রেমে সিগন্যালের ধারাবাহিকতা যাচাই করার কথা বিবেচনা করুন।

- মেশিন লার্নিং অপ্টিমাইজেশন: কৌশলের অভিযোজন ক্ষমতা বাড়াতে গতিশীল প্যারামিটার অপ্টিমাইজেশনের জন্য মেশিন লার্নিং অ্যালগরিদম প্রবর্তনের কথা বিবেচনা করুন।

সারসংক্ষেপ

এই কৌশলটি একাধিক টেকনিক্যাল সূচকের ব্যাপক ব্যবহারের মাধ্যমে একটি সম্পূর্ণ ট্রেন্ড ফলোয়িং ট্রেডিং সিস্টেম তৈরি করে। গতিশীল স্টপ-লস এবং পজিশন ম্যানেজমেন্টের মাধ্যমে এটি ঝুঁকি নিয়ন্ত্রণে চমৎকার পারফরম্যান্স প্রদর্শন করে। কৌশলটিতে শক্তিশালী সম্প্রসারণযোগ্যতা রয়েছে এবং একাধিক অপ্টিমাইজেশন দিকনির্দেশনা সংরক্ষিত আছে। বাস্তব ট্রেডিংয়ে বাস্তবায়নের সময় ব্যবসায়ীদেরকে নির্দিষ্ট বাজার বৈশিষ্ট্য ও নিজস্ব ঝুঁকির পছন্দ অনুযায়ী প্যারামিটার সমন্বয় করার পরামর্শ দেওয়া হচ্ছে।

- 1