সারসংক্ষেপ

মাল্টি-ইন্ডিকেটর ওয়েটেড স্মার্ট ট্রেডিং স্ট্র্যাটেজি একটি ব্যাপক পরিমাণগত ট্রেডিং ব্যবস্থা যা একাধিক টেকনিক্যাল ইন্ডিকেটর থেকে সংকেত গ্রহণ করে এবং বিভিন্ন ওজন দিয়ে ট্রেডিং সিদ্ধান্ত তৈরি করে। এই স্ট্র্যাটেজিটি MACD, স্টোকাস্টিক RSI, EMA, সুপার ট্রেন্ড এবং মুভিং এভারেজ ক্রসওভারের মতো বিভিন্ন টেকনিক্যাল অ্যানালাইসিস টুলকে একত্রিত করে একটি সম্পূর্ণ ট্রেডিং ফ্রেমওয়ার্ক গঠন করে। সিস্টেমটি শুধু মাল্টি-লেভেল টেক প্রফিট এবং ডায়নামিক স্টপ লস মেকানিজমই সমর্থন করে না, বরং বাজারের অবস্থা অনুযায়ী স্বয়ংক্রিয়ভাবে ট্রেডিং প্যারামিটারও সমন্বয় করে, যা একে বিভিন্ন বাজার পরিবেশে উচ্চ অভিযোজিত করে তোলে। এই স্ট্র্যাটেজিটি বিশেষ করে মধ্যম ও দীর্ঘমেয়াদী ট্রেডারদের জন্য উপযোগী, যেখানে ওজন বণ্টন পদ্ধতি ট্রেডিং সিদ্ধান্তকে আরও স্থিতিশীল ও নির্ভরযোগ্য করে তোলে।

কৌশলের নীতি

এই স্ট্র্যাটেজির মূল হলো এর ওজনযুক্ত সংকেত ব্যবস্থা, যা পাঁচটি ভিন্ন উপ-কৌশলের মাধ্যমে ট্রেডিং সংকেত তৈরি করে:

-

MACD কৌশল: ম্যাকডি লাইন এবং সিগন্যাল লাইনের ক্রসওভারের মাধ্যমে বাজারের ট্রেন্ডের দিক নির্ধারণ করে। MACD লাইন যখন সিগন্যাল লাইনের উপরে যায় তখন ক্রয় সংকেত, নিচে গেলে বিক্রয় সংকেত তৈরি হয়।

-

স্টোকাস্টিক RSI কৌশল: RSI এবং স্টোকাস্টিক ইন্ডিকেটরের সুবিধা একত্রিত করে বাজারের অতিরিক্ত ক্রয়/বিক্রয় অবস্থা পর্যবেক্ষণ করে। স্টোকাস্টিক RSI যখন নির্ধারিত ওভারসল্ড থ্রেশহোল্ডের নিচে যায় তখন ক্রয় সংকেত, ওভারবট থ্রেশহোল্ডের উপরে গেলে বিক্রয় সংকেত তৈরি হয়।

-

EMA ওভারবট/ওভারসল্ড কৌশল: EMA ব্যবহার করে দামের গড় মান থেকে বিচ্যুতির মাত্রা চিহ্নিত করে। যখন RSI নির্ধারিত ওভারসল্ড থ্রেশহোল্ডের নিচে থাকে তখন ক্রয় সংকেত, ওভারবট থ্রেশহোল্ডের উপরে থাকলে বিক্রয় সংকেত তৈরি হয়।

-

সুপার ট্রেন্ড কৌশল: ATR গুণকের ভিত্তিতে মূল্য চ্যানেল সেট করে এবং ট্রেন্ড পরিবর্তনের মাধ্যমে ট্রেডিং দিক নির্ধারণ করে। সুপার ট্রেন্ড ইন্ডিকেটর নেতিবাচক থেকে ধনাত্মক হলে ক্রয় সংকেত, ধনাত্মক থেকে নেতিবাচক হলে বিক্রয় সংকেত তৈরি হয়।

-

মুভিং এভারেজ ক্রসওভার কৌশল: দুটি ভিন্ন পিরিয়ডের মুভিং এভারেজের ক্রসওভার ব্যবহার করে বাজারের ট্রেন্ড নির্ধারণ করে। স্বল্পমেয়াদী মুভিং এভারেজ দীর্ঘমেয়াদী মুভিং এভারেজের উপরে গেলে ক্রয় সংকেত, নিচে গেলে বিক্রয় সংকেত তৈরি হয়।

স্ট্র্যাটেজিটি কাস্টমাইজযোগ্য ওজন ব্যবস্থার মাধ্যমে প্রতিটি উপ-কৌশলের সংকেতকে ওজনযুক্ত করে গণনা করে, এবং শুধুমাত্র ওজনযুক্ত যোগফল নির্ধারিত থ্রেশহোল্ড অতিক্রম করলে ট্রেড শুরু করে। এছাড়াও স্ট্র্যাটেজিতে সম্ভাব্য টপ-বটম চিহ্নিতকরণ ব্যবস্থা রয়েছে, যা বাজার উল্টানোর সম্ভাবনা থাকলে পজিশন সমন্বয় করতে পারে।

এই বহুস্তর বিশিষ্ট সংকেত নিশ্চিতকরণ ব্যবস্থা কার্যকরভাবে ভুয়া সংকেত কমায়, ট্রেডিং ব্যবস্থার নির্ভরযোগ্যতা বাড়ায় এবং নমনীয় প্যারামিটার সেটিংস স্ট্র্যাটেজিটিকে বিভিন্ন ট্রেডিং ইন্সট্রুমেন্ট এবং টাইম ফ্রেমে খাপ খাইয়ে নিতে সক্ষম করে।

কৌশলের সুবিধা

-

সংকেতের বহু নিশ্চিতকরণ: পাঁচটি পৃথক টেকনিক্যাল ইন্ডিকেটর থেকে তৈরি সংকেতের ওজনযুক্ত গণনা একক ইন্ডিকেটরের সম্ভাব্য বিভ্রান্তি কমায় এবং ট্রেডিং সংকেতের গুণগত মান ও নির্ভরযোগ্যতা বাড়ায়।

-

অভিযোজিত ওজন ব্যবস্থা: প্রতিটি উপ-কৌশলকে ভিন্ন ওজন দেওয়া যায়, যা ট্রেডারকে তাদের বিভিন্ন ইন্ডিকেটরের প্রতি আস্থা এবং ঐতিহাসিক পারফরম্যান্সের ভিত্তিতে কৌশলের গুরুত্ব সমন্বয় করতে দেয়, ফলে কৌশলের নমনীয়তা বাড়ে।

-

সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: স্ট্র্যাটেজিতে স্টপ লস, মাল্টি-লেভেল টেক প্রফিট এবং ডায়নামিক স্টপ লস অ্যাডজাস্টমেন্ট সহ বহুস্তর বিশিষ্ট ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা রয়েছে, যা বাজারের প্রতিকূল পরিবর্তনের সময় দ্রুত ঝুঁকি নিয়ন্ত্রণ নিশ্চিত করে।

-

স্বয়ংক্রিয় সম্ভাব্য টপ-বটম চিহ্নিতকরণ: RSI, ট্রেডিং ভলিউম এবং মূল্য প্রবণতার সমন্বিত বিশ্লেষণের মাধ্যমে স্ট্র্যাটেজি বাজারের সম্ভাব্য টপ ও বটম চিহ্নিত করতে পারে এবং উপযুক্ত সময়ে আংশিক পজিশন বন্ধ করে লাভ লক বা লোকসান কমাতে পারে।

-

উচ্চ কাস্টমাইজযোগ্যতা: প্রায় সব প্যারামিটার সমন্বয়যোগ্য, যার মধ্যে ইন্ডিকেটরের গণনা পিরিয়ড, ওজন মান, টেক প্রফিট/স্টপ লস শতাংশ ইত্যাদি থাকে, যা ট্রেডারকে তাদের ব্যক্তিগত শৈলী এবং বিভিন্ন বাজার অবস্থার জন্য কৌশল অপ্টিমাইজ করতে দেয়।

-

অন্তর্নির্মিত বিলম্ব প্রক্রিয়া: অকালে ট্রেডে প্রবেশ বা নয়েজ সংকেতের ভিত্তিতে ট্রেড এড়াতে, স্ট্র্যাটেজি বিলম্ব নিশ্চিতকরণ ব্যবস্থা ব্যবহার করে, যা নিশ্চিত করে যে শুধুমাত্র ধারাবাহিক সংকেত ট্রেড ট্রিগার করে, স্বল্পমেয়াদী ওঠানামার প্রভাব কমায়।

-

সময় ফিল্টারিং ফাংশন: স্ট্র্যাটেজি ট্রেডিং শুরুর এবং শেষের তারিখ নির্ধারণের অনুমতি দেয়, যা ট্রেডারকে নির্দিষ্ট সময় ধরে ঐতিহাসিক ডেটার উপর ব্যাকটেস্ট করতে বা পরিচিত বাজার অস্বাভাবিকতার সময়কাল এড়াতে সাহায্য করে।

কৌশলের ঝুঁকি

-

প্যারামিটার অত্যধিক অপ্টিমাইজেশন ঝুঁকি: অনেক প্যারামিটার থাকায়, ঐতিহাসিক ডেটার সাথে অতিরিক্ত ফিটিংয়ের ঝুঁকি থাকে, যা রিয়েল ট্রেডিংয়ে কৌশলের দুর্বল পারফরম্যান্সের কারণ হতে পারে। সমাধান: একাধিক টাইম ফ্রেম এবং ইন্সট্রুমেন্টে ব্যাকটেস্ট করুন, তুলনামূলকভাবে স্থিতিশীল প্যারামিটার সেটিংস ব্যবহার করুন এবং নির্দিষ্ট ঐতিহাসিক ডেটার জন্য অতিরিক্ত অপ্টিমাইজেশন এড়িয়ে চলুন।

-

বাজার অবস্থার পরিবর্তনের ঝুঁকি: ট্রেন্ডিং বাজার এবং রেঞ্জিং বাজারে কৌশলের পারফরম্যান্স ভিন্ন হতে পারে, বাজার অবস্থার হঠাৎ পরিবর্তন কৌশলের কার্যকারিতা কমাতে পারে। সমাধান: বাজার পরিবেশ চিহ্নিতকরণ ব্যবস্থা চালু করুন, বিভিন্ন বাজার অবস্থায় প্যারামিটার সমন্বয় করুন বা ট্রেডিং স্থগিত করুন।

-

সংকেত বিরোধের ঝুঁকি: একাধিক ইন্ডিকেটর একসাথে ব্যবহার করলে পরস্পরবিরোধী সংকেত তৈরি হতে পারে, যা সিদ্ধান্ত গ্রহণে বিভ্রান্তি সৃষ্টি করে। সমাধান: প্রতিটি ইন্ডিকেটরের ওজন যুক্তিসঙ্গতভাবে সেট করুন, আরও নির্ভরযোগ্য ইন্ডিকেটরকে অগ্রাধিকার দিন এবং সংকেত থ্রেশহোল্ড এমনভাবে সেট করুন যাতে বিরোধের সম্ভাবনা কমে।

-

অপ্রতুল মূলধন ব্যবস্থাপনার ঝুঁকি: কৌশলে স্টপ লস থাকলেও অযৌক্তিক মূলধন ব্যবস্থাপনা দ্রুত মূলধন শেষ করতে পারে। সমাধান: প্রতিটি ট্রেডের জন্য মূলধনের অনুপাত কঠোরভাবে নিয়ন্ত্রণ করুন, নিশ্চিত করুন যে একক ট্রেডের সর্বোচ্চ ঝুঁকি সহনীয় সীমার মধ্যে থাকে।

-

প্রযুক্তিগত ত্রুটির ঝুঁকি: স্বয়ংক্রিয় ট্রেডিং ব্যবস্থা নেটওয়ার্ক বিচ্ছিন্নতা, ডেটা বিলম্ব ইত্যাদির মতো প্রযুক্তিগত সমস্যার সম্মুখীন হতে পারে। সমাধান: ম্যানুয়াল হস্তক্ষেপ ব্যবস্থা সেট করুন, নিয়মিত সিস্টেমের কার্যকারিতা পর্যবেক্ষণ করুন এবং অস্বাভাবিকতা দ্রুত মোকাবিলা করুন।

কৌশল অপ্টিমাইজেশন দিকনির্দেশনা

-

বাজার পরিবেশ ফিল্টার যুক্ত করা: একটি ইন্ডিকেটর তৈরি করুন যা বর্তমান বাজার ট্রেন্ডিং নাকি রেঞ্জিং তা চিহ্নিত করতে পারে এবং বাজার অবস্থার উপর ভিত্তি করে প্রতিটি উপ-কৌশলের ওজন গতিশীলভাবে সমন্বয় করুন। ট্রেন্ডিং বাজারে ট্রেন্ড ফলোয়িং কৌশলকে শক্তিশালী করুন, রেঞ্জিং বাজারে সুইং কৌশলকে শক্তিশালী করুন।

-

মেশিন লার্নিং অপ্টিমাইজেশন চালু করা: প্রতিটি ইন্ডিকেটরের প্যারামিটার এবং ওজন স্বয়ংক্রিয়ভাবে সমন্বয় করতে মেশিন লার্নিং প্রযুক্তি ব্যবহার করুন, যাতে কৌশলটি সর্বশেষ বাজার ডেটা অনুযায়ী ক্রমাগত শিখতে এবং খাপ খাইয়ে নিতে পারে, কৌশলের গতিশীল অভিযোজন ক্ষমতা বাড়ায়।

-

ট্রেডিং ভলিউম বিশ্লেষণ যোগ করা: অতিরিক্ত নিশ্চিতকরণ সংকেত হিসাবে ট্রেডিং ভলিউমের পরিবর্তন ব্যবহার করুন, শুধুমাত্র তখনই ট্রেড কার্যকর করুন যখন প্রত্যাশিত ভলিউম সমর্থন থাকে, সংকেতের বিশ্বাসযোগ্যতা বাড়ান।

-

সম্ভাব্য টপ-বটম চিহ্নিতকরণ অ্যালগরিদম অপ্টিমাইজ করা: বিদ্যমান টপ-বটম চিহ্নিতকরণ লজিক উন্নত করুন, মূল্য প্যাটার্ন, মাল্টি-টাইমফ্রেম নিশ্চিতকরণ ইত্যাদির মতো আরও নিশ্চিতকরণ ফ্যাক্টর যোগ করুন, চিহ্নিতকরণের নির্ভুলতা বাড়ান।

-

আবেগ সূচক যোগ করা: বাজারের আবেগ সূচক যেমন ভীতি সূচক (VIX), কল-পুট অনুপাত ইত্যাদি একীভূত করুন। চরম বাজার আবেগের সময় ট্রেডিং কৌশল সমন্বয় করুন বা ট্রেডিং স্থগিত করুন, উচ্চ অস্থিরতার সময় অতিরিক্ত ট্রেডিং এড়িয়ে চলুন।

-

গতিশীল টেক প্রফিট/স্টপ লস মেকানিজম তৈরি করা: বাজারের অস্থিরতা অনুযায়ী স্বয়ংক্রিয়ভাবে টেক প্রফিট এবং স্টপ লস স্তর সমন্বয় করুন। উচ্চ অস্থিরতার বাজারে স্টপ লস পরিসর প্রশস্ত করুন, কম অস্থিরতার বাজারে সংকীর্ণ করুন, যাতে ঝুঁকি ব্যবস্থাপনা আরও নমনীয় এবং কার্যকর হয়।

-

টাইম ফ্রেম অপ্টিমাইজেশন: মাল্টি-টাইমফ্রেম বিশ্লেষণের কার্যকারিতা যোগ করুন, যাতে উচ্চ স্তরের এবং নিম্ন স্তরের টাইম ফ্রেম একসাথে সংকেত নিশ্চিত করে। এটি মিথ্যা ব্রেকআউট এবং মিথ্যা সংকেত কমায়।

উপসংহার

মাল্টি-ইন্ডিকেটর ওয়েটেড স্মার্ট ট্রেডিং স্ট্র্যাটেজি একাধিক টেকনিক্যাল অ্যানালাইসিস টুল একীভূত করে এবং বিভিন্ন ওজন আরোপ করে একটি সম্পূর্ণ ও নমনীয় ট্রেডিং ব্যবস্থা গঠন করে। এই কৌশলটিতে সংকেতের বহু নিশ্চিতকরণ, অভিযোজিত ওজন ব্যবস্থা এবং সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা বৈশিষ্ট্য সহ স্বয়ংক্রিয় সম্ভাব্য টপ-বটম চিহ্নিতকরণ ব্যবস্থা রয়েছে, যা একে জটিল ও পরিবর্তনশীল বাজার পরিবেশে শক্তিশালী অভিযোজন ক্ষমতা প্রদর্শন করতে সহায়তা করে।

প্যারামিটার অত্যধিক অপ্টিমাইজেশন, বাজার অবস্থার পরিবর্তন এবং সংকেত বিরোধের মতো সম্ভাব্য ঝুঁকি থাকলেও, যুক্তিসঙ্গত প্যারামিটার সেটিংস, বাজার পরিবেশ চিহ্নিতকরণ এবং কঠোর মূলধন ব্যবস্থাপনার মাধ্যমে এই ঝুঁকিগুলি কার্যকরভাবে নিয়ন্ত্রণ করা যায়। ভবিষ্যতের অপ্টিমাইজেশন দিকনির্দেশনার মধ্যে বাজার পরিবেশ ফিল্টার যুক্ত করা, মেশিন লার্নিং প্রযুক্তি চালু করা, ট্রেডিং ভলিউম বিশ্লেষণ জোরদার করা এবং সম্ভাব্য টপ-বটম চিহ্নিতকরণ অ্যালগরিদম অপ্টিমাইজ করা অন্তর্ভুক্ত, যা কৌশলের স্থিতিশীলতা ও লাভজনক ক্ষমতা আরও উন্নত করবে।

যেসব বিনিয়োগকারী পদ্ধতিগত ট্রেডিং পদ্ধতি খুঁজছেন তাদের জন্য, এই মাল্টি-ইন্ডিকেটর ওয়েটেড স্মার্ট ট্রেডিং স্ট্র্যাটেজি একটি বিবেচনাযোগ্য কাঠামো সরবরাহ করে যা শুধু আবেগের প্রভাব কমায় না বরং ডেটা-চালিত উপায়ে ট্রেডিং পারফরম্যান্সকে ক্রমাগত অপ্টিমাইজ করতে পারে। এই কৌশল বাস্তবায়নের সময়, রক্ষণশীল প্যারামিটার সেটিংস থেকে শুরু করে ধীরে ধীরে সমন্বয় এবং কৌশলের পারফরম্যান্স নিবিড়ভাবে পর্যবেক্ষণ করার পরামর্শ দেওয়া হয়, যাতে ব্যক্তিগত ঝুঁকি সহনশীলতা এবং বাজার অবস্থার জন্য সবচেয়ে উপযুক্ত কনফিগারেশন খুঁজে পাওয়া যায়।

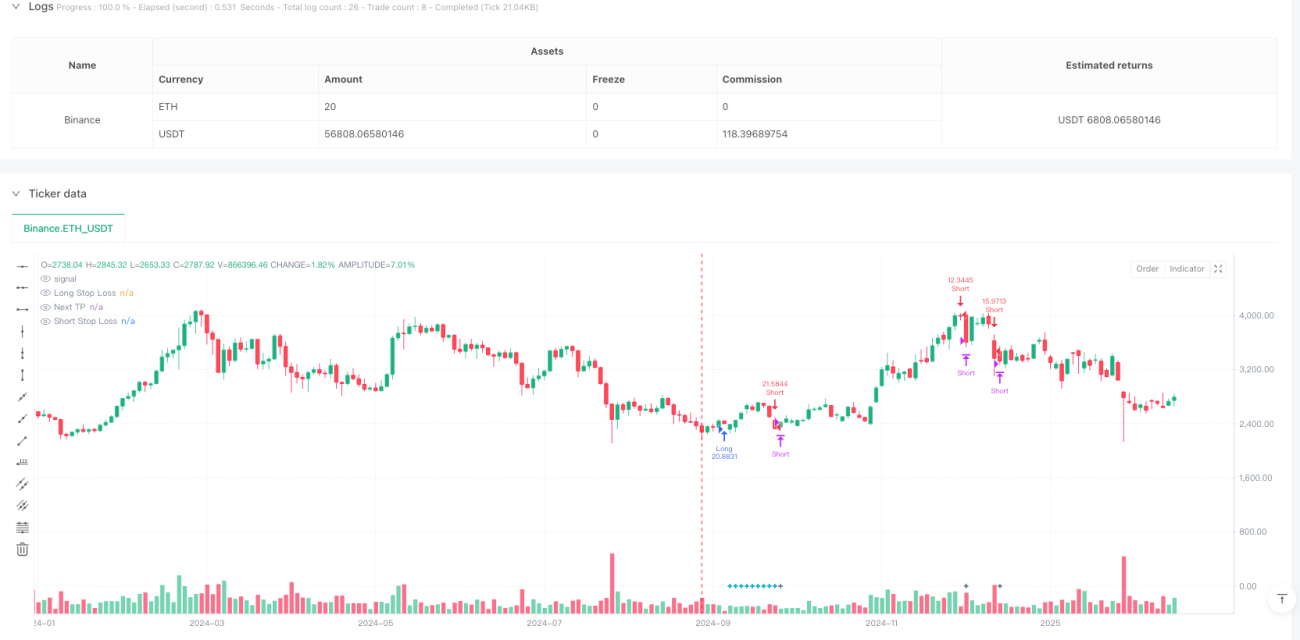

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1