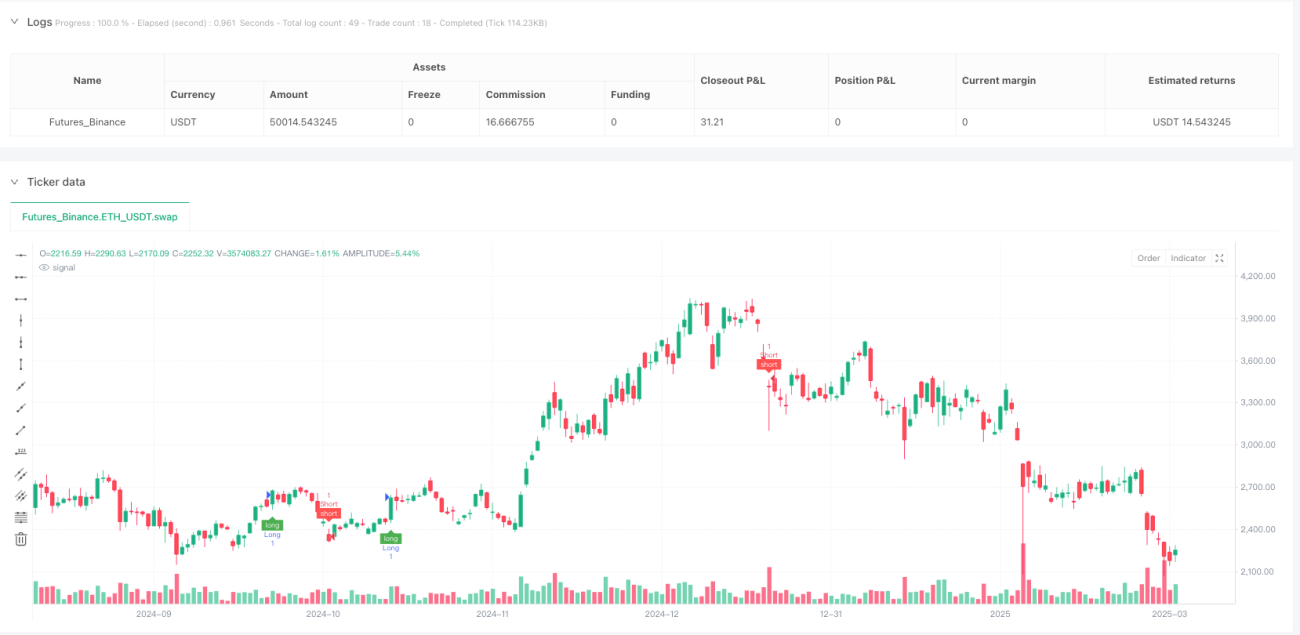

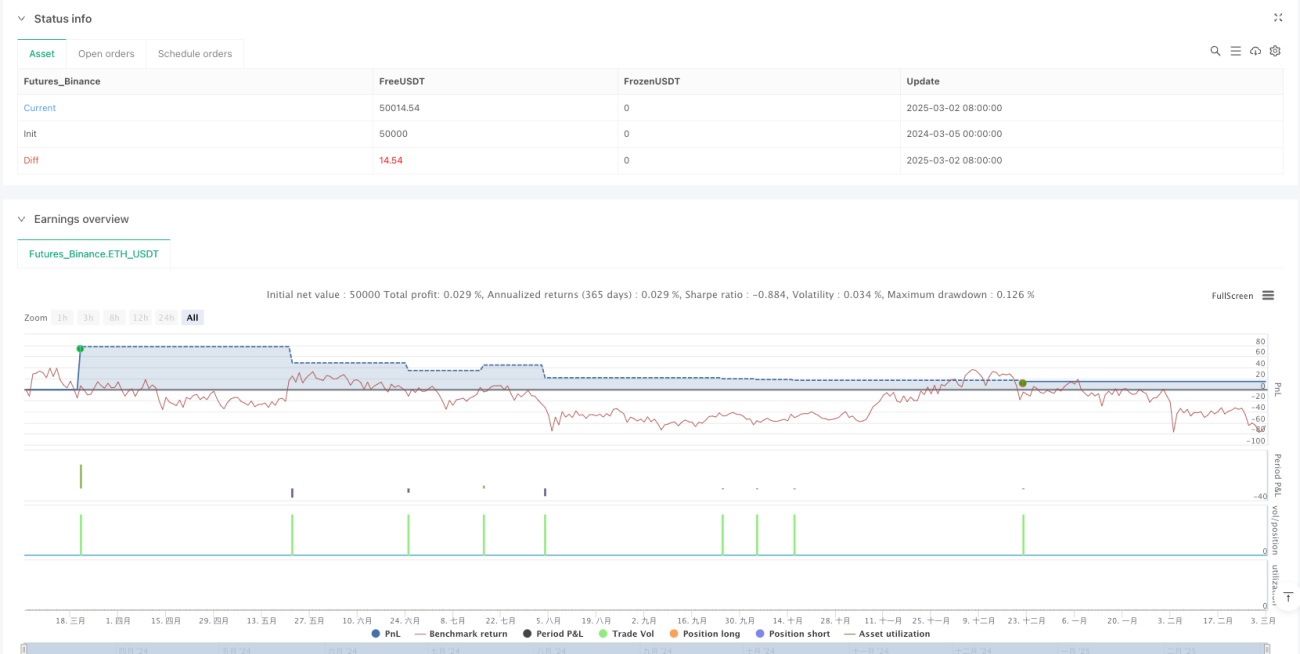

একাধিক প্রযুক্তিগত সূচক সহ স্বর্ণের তাৎক্ষণিক পরিবর্তন সনাক্তকরণ ও ঝুঁকি ব্যবস্থাপনা কৌশল

কৌশল সংক্ষিপ্ত বিবরণ

মাল্টিপল টেকনিক্যাল ইন্ডিকেটর গোল্ড রিয়েল-টাইম মুভমেন্ট ডিটেকশন অ্যান্ড রিস্ক ম্যানেজমেন্ট স্ট্র্যাটেজি হলো একটি 1 মিনিটের হেইকিন আশি চার্টের উপর ভিত্তি করে সোনার ট্রেডিং সিস্টেম, যা ট্রেডিং সিগন্যাল এবং নিশ্চিতকরণ টুল হিসেবে বিভিন্ন টেকনিক্যাল ইন্ডিকেটরকে একত্রিত করে। এই কৌশলটি প্রধানত চান্ডেলিয়ার এক্সিট (Chandelier Exit) কে প্রধান নির্দেশক হিসেবে ব্যবহার করে, এবং ঐচ্ছিকভাবে EMA ফিল্টার, সুপারট্রেন্ড (SuperTrend) এবং শ্যাফ ট্রেন্ড সাইকেল (Schaff Trend Cycle) এর মতো সূচকগুলিকে নিশ্চিতকরণ টুল হিসেবে যুক্ত করা যায়। কৌশলটিতে একটি নমনীয় লাভ-লোকসান ব্যবস্থা এবং একটি স্বজ্ঞাত ট্রেডিং ড্যাশবোর্ড রয়েছে, যা ট্রেডারদের রিয়েল-টাইমে ট্রেডিং অবস্থা পর্যবেক্ষণ করতে সক্ষম করে। এই বহুমাত্রিক টেকনিক্যাল বিশ্লেষণ পদ্ধতির লক্ষ্য হলো সোনার দামের স্বল্পমেয়াদী ওঠানামা দ্রুত শনাক্ত করা, পাশাপাশি সূচক নিশ্চিতকরণ ব্যবস্থার মাধ্যমে মিথ্যা সিগন্যালের ঝুঁকি কমানো।

কৌশল নীতি

এই কৌশলটি বহুস্তরীয় সংকেত নিশ্চিতকরণ ব্যবস্থার উপর ভিত্তি করে তৈরি, যার মূল যুক্তি নিম্নরূপ:

-

প্রধান নির্দেশক সংকেত তৈরি: কৌশলটি চান্ডেলিয়ার এক্সিট (Chandelier Exit) কে প্রধান নির্দেশক হিসেবে ব্যবহার করে। চান্ডেলিয়ার এক্সিট হলো একটি ট্রেন্ড ফলোয়িং ইন্ডিকেটর, যা স্টপ-লস অবস্থান নির্ধারণ করতে ATR (গড় প্রকৃত পরিসর) গুণক ব্যবহার করে এবং লং ও শর্ট সিগন্যাল তৈরি করে।

-

নিশ্চিতকরণ সূচক ফিল্টারিং: কৌশলটি ট্রেডারদের ঐচ্ছিকভাবে একাধিক নিশ্চিতকরণ সূচক সক্রিয় করার সুযোগ দেয়:

- EMA ফিল্টার: লং অবস্থানের জন্য দাম নির্দিষ্ট EMA রেখার উপরে এবং শর্ট অবস্থানের জন্য নিচে থাকতে হবে।

- সুপারট্রেন্ড (SuperTrend): প্রধান সংকেতের দিকের সাথে সামঞ্জস্যপূর্ণ হতে হবে।

- শ্যাফ ট্রেন্ড সাইকেল (STC): লং অবস্থানের জন্য উপরের সীমার (আপার বাউন্ড) উপরে এবং শর্ট অবস্থানের জন্য নিচের সীমার (লোয়ার বাউন্ড) নিচে হতে হবে।

-

সংকেত মেয়াদোত্তীর্ণ প্রক্রিয়া: কৌশলটিতে সংকেতের মেয়াদ শেষ হওয়ার একটি বৈশিষ্ট্য রয়েছে, যেখানে সংকেত বৈধ থাকার জন্য ক্যান্ডেলের সংখ্যা নির্ধারণ করা যায়। এটি পুরানো সিগন্যালে ট্রেড করার ঝুঁকি কমায়।

-

ট্রেড এক্সিকিউশন লজিক: যখন সমস্ত নির্বাচিত শর্ত পূরণ হয়, তখন কৌশলটি এন্ট্রি সিগন্যাল তৈরি করে এবং স্বয়ংক্রিয়ভাবে নির্দিষ্ট পয়েন্টে লাভ-লোকসান সেট করে।

-

ডেটা প্রসেসিং অপটিমাইজেশন: কৌশলটি কন্ডিশনাল স্যাম্পলিং EMA এবং SMA ফাংশন এবং একটি ডেডিকেটেড রেঞ্জ ফিল্টার ব্যবহার করে, যা টেকনিক্যাল ইন্ডিকেটরের গণনায় দক্ষতা বাড়ায়।

-

ভিজুয়ালাইজেশন সিস্টেম: একটি ট্রেডিং ড্যাশবোর্ড প্রদান করে যা প্রতিটি সূচকের অবস্থা দেখায় এবং চার্টে ট্রেড সিগন্যাল ও লাভ-লোকসানের অবস্থান চিহ্নিত করে।

কৌশলের সুবিধা

-

একাধিক নিশ্চিতকরণ ব্যবস্থা: একাধিক সূচকের মাধ্যমে নিশ্চিতকরণ মিথ্যা সংকেত উল্লেখযোগ্যভাবে হ্রাস করে এবং ট্রেডের নির্ভুলতা বাড়ায়। যখন একাধিক সূচক একই দিক নিশ্চিত করে, তখন ট্রেড সিগন্যাল আরও নির্ভরযোগ্য হয়।

-

নমনীয় সূচক সমন্বয়: ব্যবহারকারীরা বিভিন্ন বাজার পরিস্থিতির সাথে কৌশলের পারফরম্যান্স কাস্টমাইজ করতে বিভিন্ন নিশ্চিতকরণ সূচক সক্রিয় বা নিষ্ক্রিয় করতে পারেন।

-

সঠিক ঝুঁকি ব্যবস্থাপনা: কৌশলটি ব্যবহারকারীদের নির্দিষ্ট পয়েন্টে লাভ ও স্টপ-লস সেট করতে দেয়, যা প্রতি ট্রেডের ঝুঁকি-পুরস্কার অনুপাত সঠিকভাবে নিয়ন্ত্রণ করতে সাহায্য করে।

-

সংকেত মেয়াদ নিয়ন্ত্রণ: সংকেতের বৈধতা সময় নির্ধারণের মাধ্যমে, কৌশলটি পুরানো সিগন্যালে ট্রেড করা এড়িয়ে যায় এবং ল্যাগ ঝুঁকি হ্রাস করে।

-

উচ্চ দৃশ্যমান ট্রেডিং ইন্টারফেস: ট্রেডিং ড্যাশবোর্ড স্পষ্টভাবে সমস্ত সূচকের অবস্থা দেখায়, যা ট্রেডারদের বাজার পরিস্থিতি দ্রুত মূল্যায়ন করতে সহায়তা করে।

-

সোনার বাজারের জন্য অপটিমাইজড: কৌশলটি সোনার বাজারের বৈশিষ্ট্যের জন্য প্যারামিটার অপটিমাইজ করা হয়েছে, বিশেষ করে পয়েন্ট মান রূপান্তর (1 পয়েন্ট = 0.1 ডলার) বিবেচনায় নিয়ে।

-

উচ্চ ফ্রিকোয়েন্সি ট্রেডিংয়ের উপযোগিতা: 1 মিনিটের সময়সীমা কৌশলটিকে স্বল্পমেয়াদী দামের ওঠানামা ধরতে সক্ষম করে, যা ডে ট্রেডারদের জন্য উপযুক্ত।

কৌশলের ঝুঁকি

-

অতিরিক্ত ট্রেডিংয়ের ঝুঁকি: 1 মিনিটের সময়সীমা অনেক ট্রেড সিগন্যাল তৈরি করতে পারে, যার ফলে ট্রেডিং খরচ বেড়ে যেতে পারে এবং অতিরিক্ত ট্রেডিং হতে পারে। সমাধান হলো নিশ্চিতকরণ সূচকের সংখ্যা সামঞ্জস্য করা বা সিগন্যাল ফিল্টার শর্ত বাড়ানো।

-

বাজারের শব্দের প্রভাব: নিম্ন সময়সীমা বাজারের শব্দ (নয়েজ) দ্বারা বেশি প্রভাবিত হয়, যা মিথ্যা সিগন্যাল তৈরি করতে পারে। উচ্চ অস্থিরতার সময় সতর্কতার সাথে ব্যবহার করা বা দীর্ঘমেয়াদী সময়সীমার ট্রেন্ড নিশ্চিতকরণ যুক্ত করার পরামর্শ দেওয়া হয়।

-

সূচক স্ট্যাকিংয়ের পিছিয়ে পড়া: একাধিক সূচক নিশ্চিতকরণ মিথ্যা সিগন্যাল কমালেও, এটি সিস্টেমের পিছিয়ে পড়া (ল্যাগ) বাড়িয়ে দেয়, যার ফলে কিছু লাভের সুযোগ হাতছাড়া হতে পারে। প্রতিক্রিয়ার গতি বাড়ানোর জন্য নিশ্চিতকরণ সূচকের সংখ্যা কমানো যেতে পারে।

-

স্থির লাভ-লোকসানের সীমাবদ্ধতা: নির্দিষ্ট পয়েন্টে লাভ-লোকসান বাজারের অস্থিরতার পরিবর্তন বিবেচনা করে না। উচ্চ অস্থিরতার সময় স্টপ-লস খুব কাছাকাছি হতে পারে এবং কম অস্থিরতার সময় লাভের লক্ষ্য অনেক দূরে হতে পারে। বর্তমান ATR-এর ভিত্তিতে গতিশীল লাভ-লোকসান মান ব্যবহার করার পরামর্শ দেওয়া হয়।

-

সোনার বাজারের বিশেষ ঝুঁকি: সোনার বাজার অনেকগুলি সামষ্টিক অর্থনৈতিক কারণ যেমন মুদ্রাস্ফীতি তথ্য, কেন্দ্রীয় ব্যাংকের নীতি, ভূরাজনীতি ইত্যাদি দ্বারা প্রভাবিত হয়। বিশুদ্ধ প্রযুক্তিগত বিশ্লেষণ এই প্রভাবগুলি উপেক্ষা করতে পারে। মৌলিক বিশ্লেষণের সাথে একত্রে ব্যবহার করার পরামর্শ দেওয়া হয়।

-

প্রধান নির্দেশকের উপর নির্ভরশীলতা: কৌশলটি চান্ডেলিয়ার এক্সিটের উপর অত্যধিক নির্ভরশীল, যা রেঞ্জ বাজারে খারাপ পারফর্ম করতে পারে। একাধিক প্রধান নির্দেশক নির্বাচনের বিকল্প যুক্ত করার পরামর্শ দেওয়া হয়।

কৌশল অপটিমাইজেশনের দিকনির্দেশনা

-

প্রধান নির্দেশকের বৈচিত্র্যকরণ: বর্তমানে কৌশলটি শুধুমাত্র চান্ডেলিয়ার এক্সিটকে প্রধান নির্দেশক হিসেবে সমর্থন করে। বিভিন্ন বাজার পরিবেশের সাথে মানিয়ে নিতে বোলিঞ্জার ব্যান্ড, MACD বা অ্যাডাপটিভ মুভিং এভারেজের মতো অন্যান্য প্রধান নির্দেশক নির্বাচনের জন্য প্রসারিত করা যেতে পারে।

-

গতিশীল লাভ-লোকসান: নির্দিষ্ট পয়েন্টের পরিবর্তে ATR-ভিত্তিক গতিশীল লাভ-লোকসান ব্যবহার করলে বাজারের অস্থিরতা পরিবর্তনের সাথে মানিয়ে নেওয়া যায়। উদাহরণস্বরূপ,

sl_value = atr(14) * 1.5ব্যবহার করা যেতে পারে। -

সময় ফিল্টার সংযোজন: কম তারল্য সময় বা গুরুত্বপূর্ণ সংবাদ প্রকাশের সময় এড়াতে ট্রেডিং সময় ফিল্টার যুক্ত করলে স্লিপেজ এবং অপ্রত্যাশিত দামের ওঠানামার ঝুঁকি কমানো যায়।

-

ভলিউম বিশ্লেষণ অন্তর্ভুক্তি: ভলিউম সূচক সংযুক্ত করলে দামের চলাচলের শক্তি যাচাই করা যায় এবং সিগন্যালের গুণমান উন্নত হয়। উদাহরণস্বরূপ, শুধুমাত্র যখন ভলিউম বাড়ে তখনই ব্রেকআউট সিগন্যাল নিশ্চিত করা।

-

মেশিন লার্নিং অপটিমাইজেশন: মেশিন লার্নিং অ্যালগরিদম ব্যবহার করে প্রতিটি সূচকের ওজন গতিশীলভাবে সামঞ্জস্য করা যায় এবং সাম্প্রতিক বাজার পারফরম্যান্সের উপর ভিত্তি করে কৌশলের প্যারামিটারগুলিকে অভিযোজিত করা যায়।

-

পার্টিশন এন্ট্রি/এক্সিট মেকানিজম: একক এন্ট্রি/এক্সিট পয়েন্টের সময় ঝুঁকি কমাতে ধাপে ধাপে এন্ট্রি এবং এক্সিট বাস্তবায়ন করা, যেমন তিনটি ধাপে পজিশন খোলা এবং তিনটি ধাপে বন্ধ করা।

-

একাধিক সময়সীমার নিশ্চিতকরণ: উচ্চতর সময়সীমার ট্রেন্ড নিশ্চিতকরণ যোগ করা, শুধুমাত্র উচ্চ সময়সীমার ট্রেন্ডের দিকে পজিশন খোলা, যা প্রতিকূল ট্রেন্ডে ট্রেড করার ঝুঁকি হ্রাস করে।

-

সূচকের সম্পর্ক বিশ্লেষণ: নির্বাচিত সূচকগুলির মধ্যে সম্পর্ক বিশ্লেষণ করা এবং অত্যন্ত সম্পর্কিত সূচকগুলিকে পরিহার করা। এটি বিভ্রান্তিকর একাধিক নিশ্চিতকরণের কারণ হতে পারে।

সারসংক্ষেপ

মাল্টিপল টেকনিক্যাল ইন্ডিকেটর গোল্ড রিয়েল-টাইম মুভমেন্ট ডিটেকশন অ্যান্ড রিস্ক ম্যানেজমেন্ট স্ট্র্যাটেজি হলো স্বল্পমেয়াদী ট্রেডারদের জন্য একটি যৌগিক ট্রেডিং সিস্টেম, যা একাধিক টেকনিক্যাল ইন্ডিকেটরকে একীভূত করে আরও নির্ভরযোগ্য ট্রেড সিগন্যাল প্রদান করে। এই কৌশলটির মূল শক্তি হলো এর নমনীয় সূচক নিশ্চিতকরণ ব্যবস্থা এবং স্বজ্ঞাত ভিজুয়াল ইন্টারফেস, যা ট্রেডারদের বাজার পরিস্থিতি অনুযায়ী কৌশলের প্যারামিটারগুলি সামঞ্জস্য করতে দেয়। তবে ব্যবহারকারীদের নিম্ন সময়সীমার ট্রেডিংয়ের সহজাত ঝুঁকি সম্পর্কে সতর্ক থাকা উচিত, যার মধ্যে অতিরিক্ত ট্রেডিং এবং বাজারের শব্দের প্রভাব অন্তর্ভুক্ত।

প্রস্তাবিত অপটিমাইজেশন ব্যবস্থাগুলি বাস্তবায়নের মাধ্যমে, বিশেষ করে গতিশীল লাভ-লোকসান, একাধিক সময়সীমার নিশ্চিতকরণ এবং প্রধান নির্দেশকের বৈচিত্র্যকরণ, এই কৌশলটির অভিযোজন ক্ষমতা এবং দৃঢ়তা আরও উন্নত করা যেতে পারে। ডে ট্রেডার এবং স্বল্পমেয়াদী সোনার ট্রেডিং উত্সাহীদের জন্য, এই কৌশলটি একটি প্রযুক্তিগত বিশ্লেষণ কাঠামো প্রদান করে, তবে সর্বোত্তম ফলাফলের জন্য মূলধন ব্যবস্থাপনার নীতি এবং বাজারের মৌলিক বিষয়গুলির সাথে একত্রে ব্যবহার করা উচিত।

শেষ পর্যন্ত, ট্রেডিং সাফল্য শুধুমাত্র কৌশলের উপর নয়, বরং ট্রেডারের কৌশলটি বোঝা এবং সঠিকভাবে বাস্তবায়নের উপরও নির্ভর করে। ধারাবাহিক কৌশল ব্যাকটেস্টিং, অপটিমাইজেশন এবং অভিযোজন দীর্ঘমেয়াদী স্থিতিশীল ট্রেডিং ফলাফল অর্জনের চাবিকাঠি।

- 1