সংক্ষিপ্ত বিবরণ

এটি একটি উদ্ভাবনী পরিমাণগত ট্রেডিং কৌশল, যা লিকুইডিটি জোন এন্ট্রি, ATR অস্থিরতা থ্রেশহোল্ড এবং গতিশীল ঝুঁকি ব্যবস্থাপনাকে একীভূত করে, ব্যবসায়ীদের জন্য একটি কাঠামোবদ্ধ ট্রেডিং পদ্ধতি প্রদান করে। এই কৌশলটি একাধিক প্রযুক্তিগত বিশ্লেষণ সূচককে একত্রিত করে, যাতে উচ্চ সম্ভাবনার ট্রেডিং সুযোগ চিহ্নিত করা যায় এবং স্বয়ংক্রিয়ভাবে লাভের লক্ষ্য ও স্টপ-লস স্তর গণনা করা যায়।

কৌশলের মূলনীতি

কৌশলটির মূল নীতি নিম্নলিখিত মূল উপাদানের উপর ভিত্তি করে তৈরি:

- লিকুইডিটি জোন বিশ্লেষণ: নির্দিষ্ট সময়সীমার মধ্যে সর্বনিম্ন ও সর্বোচ্চ পয়েন্ট গণনা করে সম্ভাব্য সমর্থন ও প্রতিরোধ অঞ্চল চিহ্নিত করা।

- ATR অস্থিরতা ফিল্টার: গড় ট্রু রেঞ্জ (ATR) ব্যবহার করে এন্ট্রি এবং ঝুঁকি ব্যবস্থাপনার জন্য গতিশীল থ্রেশহোল্ড নির্ধারণ।

- ট্রেন্ড ফিল্টার: বাজারের ট্রেন্ড এবং মুভমেন্ট নিশ্চিত করতে ৫০-পিরিয়ড এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA) এবং রিলেটিভ স্ট্রেংথ ইনডেক্স (RSI) যুক্ত করা।

- গতিশীল ঝুঁকি ব্যবস্থাপনা: ATR-এর ভিত্তিতে স্বয়ংক্রিয়ভাবে লাভের লক্ষ্য ও স্টপ-লস স্তর গণনা করে এবং ঝুঁকি/রিটার্ন অনুপাত নমনীয়ভাবে সামঞ্জস্য করার অনুমতি দেয়।

কৌশলের সুবিধা

- বহু-মাত্রিক সংকেত উৎপাদন: লিকুইডিটি, অস্থিরতা এবং ট্রেন্ড ফিল্টার একত্রিত করে সংকেতের গুণগত মান বৃদ্ধি করে।

- অভিযোজিত ঝুঁকি ব্যবস্থাপনা: গতিশীলভাবে স্টপ-লস ও টেক-প্রফিট সামঞ্জস্য করে, যা ট্রেডিং ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করে।

- নমনীয় প্যারামিটার কনফিগারেশন: ATR দৈর্ঘ্য, লিকুইডিটি পিরিয়ড এবং ট্রেডিং সেশন কাস্টমাইজ করা যায়।

- ভিজুয়াল সাপোর্ট: লিকুইডিটি লাইন এবং প্রথম ক্যান্ডেল স্তরের ভিজুয়াল ডিসপ্লে প্রদান করে।

- কর্মক্ষমতা ট্র্যাকিং: অন্তর্নির্মিত ট্রেডিং স্ট্যাটিস্টিক্স টেবিল সরাসরি চার্টে জয় রেট এবং জয়-লস পরিস্থিতি প্রদর্শন করে।

কৌশলের ঝুঁকি

- প্যারামিটার সংবেদনশীলতা: কৌশলের কর্মক্ষমতা প্যারামিটার নির্বাচনের উপর অত্যন্ত নির্ভরশীল, তাই ক্রমাগত ব্যাকটেস্টিং এবং অপ্টিমাইজেশন প্রয়োজন।

- বাজার অভিযোজন: স্পষ্ট ট্রেন্ডবিহীন বা অত্যন্ত অস্থির বাজারে কর্মক্ষমতা অস্থির হতে পারে।

- ভুল ব্রেকআউটের ঝুঁকি: লিকুইডিটি জোন ব্রেকআউটের ক্ষেত্রে ভুয়া সংকেতের সম্ভাবনা থাকে।

- ট্রেডিং ফ্রিকোয়েন্সি: সেশন ফিল্টার এবং একাধিক শর্তের কারণে ট্রেডিং সুযোগ কমে যেতে পারে।

- ব্যাকটেস্টিং বায়াস: ঐতিহাসিক তথ্যে ৬৪% জয় রেট ভবিষ্যতের কর্মক্ষমতার সম্পূর্ণ প্রতিনিধিত্ব নাও করতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- মেশিন লার্নিং ইন্টিগ্রেশন: প্যারামিটার এবং সংকেত উৎপাদন গতিশীলভাবে সামঞ্জস্য করতে মেশিন লার্নিং অ্যালগরিদম ব্যবহার।

- বহু-বাজার অভিযোজন: বিভিন্ন বাজার এবং সম্পদের জন্য উপযুক্ত আরও সাধারণ প্যারামিটার সেটিং তৈরি করা।

- গভীর ঝুঁকি ব্যবস্থাপনা: আরও জটিল পজিশন সাইজিং এবং ঝুঁকি বরাদ্দ অ্যালগরিদম অন্তর্ভুক্ত করা।

- সংকেত নিশ্চিতকরণ প্রক্রিয়া: অতিরিক্ত নিশ্চিতকরণ সূচক যেমন ভলিউম বা অন্যান্য প্রযুক্তিগত সূচক যুক্ত করা।

- রিয়েল-টাইম কর্মক্ষমতা পর্যবেক্ষণ: রিয়েল-টাইম কর্মক্ষমতা মূল্যায়ন এবং অভিযোজিত সামঞ্জস্য মডিউল তৈরি করা।

সারসংক্ষেপ

থিঙ্কটেক এআই ট্রেডিং কৌশল একটি উদ্ভাবনী মাল্টি-ফ্যাক্টর পদ্ধতির মাধ্যমে ব্যবসায়ীদের জন্য একটি শক্তিশালী পরিমাণগত ট্রেডিং টুল সরবরাহ করে। লিকুইডিটি বিশ্লেষণ, অস্থিরতা ফিল্টারিং এবং গতিশীল ঝুঁকি ব্যবস্থাপনার মাধ্যমে, এই কৌশলটি উচ্চ-মানের ট্রেডিং সুযোগ চিহ্নিত করার লক্ষ্য রাখে। তবে, কৌশলের সম্ভাবনা সম্পূর্ণরূপে কাজে লাগাতে ব্যবসায়ীদের ক্রমাগত ব্যাকটেস্টিং, অপ্টিমাইজেশন এবং সতর্কতার সাথে প্রয়োগ করতে হবে।

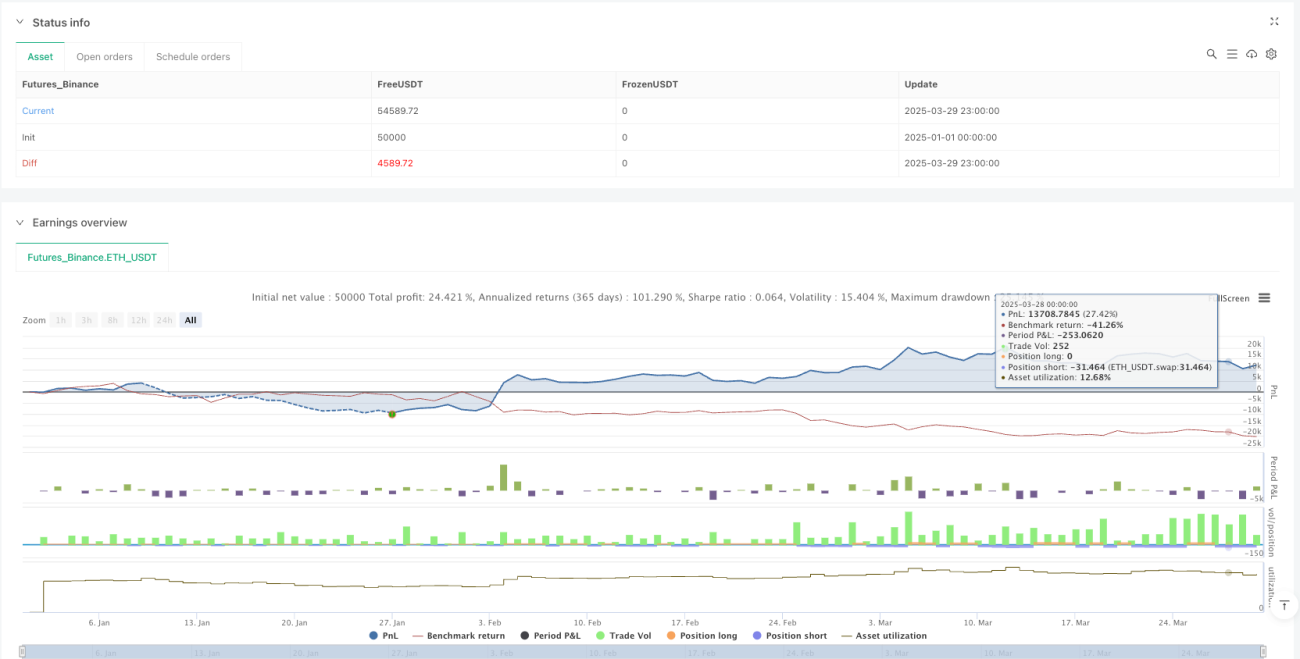

/*backtest

start: 2025-01-01 00:00:00

end: 2025-03-30 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

if high > ta.highest(high[1], 5)

strategy.entry("Enter Long", strategy.long)

else if low < ta.lowest(low[1], 5)

strategy.entry("Enter Short", strategy.short)//@version=6- 1