পিভট পয়েন্টের উপর ভিত্তি করে ভলিউম-ওয়েটেড ব্রেকআউট/রিভার্সাল কৌশল

সংক্ষিপ্ত বিবরণ

এই কৌশলটি সাপোর্ট/রেজিস্ট্যান্স (S/R) ব্রেকআউট/রিভার্সাল, ভলিউম ফিল্টার এবং অ্যালার্ম সিস্টেমকে একত্রিত করে, যার লক্ষ্য বাজারের গুরুত্বপূর্ণ মোড় পয়েন্টগুলো ধরা। কৌশলটি মূল্য ব্রেকআউট বা রিভার্সাল সিগন্যাল শনাক্ত করে এবং অস্বাভাবিক ভলিউম নিশ্চিতকরণের মাধ্যমে ট্রেডিং সিগন্যালের নির্ভরযোগ্যতা বাড়ায়। ঝুঁকি ব্যবস্থাপনার জন্য কৌশলটি নির্দিষ্ট ২% স্টপ-লস এবং একটি সমন্বয়যোগ্য টেক-প্রফিট অনুপাত (ডিফল্ট ৩%) ব্যবহার করে।

কৌশলের মূলনীতি

- সাপোর্ট/রেজিস্ট্যান্স শনাক্তকরণ: নির্দিষ্ট পিরিয়ডে (pivotLen) কী মূল্য স্তর শনাক্ত করতে

ta.pivothigh()এবংta.pivotlow()ফাংশন ব্যবহার করে। যখন মূল্য রেজিস্ট্যান্স এলাকা ভেঙ্গে যায় (১% উপরে) বা সাপোর্ট এলাকা থেকে বাউন্স করে (নিচে নেমে ফিরে আসে) তখন সিগন্যাল ট্রিগার হয়। - ভলিউম ফিল্টার: ভলিউমের SMA (volSmaLength পিরিয়ড) গণনা করা হয়, যখন বর্তমান ভলিউম SMA-এর volMultiplier গুণ (ডিফল্ট ১.৫ গুণ) ছাড়িয়ে যায় তখন তা বৈধ নিশ্চিতকরণ হিসেবে বিবেচিত হয়।

- বুলিশ ও বেয়ারিশ লজিক:

- বুলিশ শর্ত: মূল্য রেজিস্ট্যান্স জোন ভেঙে গেলে (close > resZone*1.01) এবং উচ্চ ভলিউম থাকলে, অথবা মূল্য সাপোর্ট জোনের কাছাকাছি (±১% সীমার মধ্যে) থাকলে "ফলস ব্রেকডাউন" (low ≤ supZone হলেও ক্লোজ ফিরে আসে) এবং ভলিউম বেড়ে গেলে।

- বেয়ারিশ শর্ত: মূল্য সাপোর্ট জোন ভেঙে গেলে (close < supZone*0.99) এবং উচ্চ ভলিউম থাকলে, অথবা মূল্য রেজিস্ট্যান্স জোনের কাছাকাছি (±১% সীমার মধ্যে) থাকলে "ফলস ব্রেকআউট" (high ≥ resZone হলেও ক্লোজ ফিরে আসে) এবং ভলিউম বেড়ে গেলে।

- ঝুঁকি ব্যবস্থাপনা: নির্দিষ্ট ২% স্টপ-লস এবং সমন্বয়যোগ্য টেক-প্রফিট (ডিফল্ট ৩%)

strategy.exit()ব্যবহার করে বাস্তবায়িত হয়।

সুবিধা বিশ্লেষণ

- মাল্টি-ফ্যাক্টর যাচাইকরণ: মূল্যের কাঠামো (S/R), ভলিউম এবং বাজার আচরণ (ফলস ব্রেকআউট/ফলস ব্রেকডাউন) একত্রিত হওয়ায় মিথ্যা সিগন্যালের সম্ভাবনা উল্লেখযোগ্যভাবে কমে যায়।

- গতিশীল অভিযোজন: সাপোর্ট/রেজিস্ট্যান্স লেভেল স্বয়ংক্রিয়ভাবে আপডেট হয়, বাজারের পরিবর্তনের সাথে খাপ খায়।

- কঠোর ঝুঁকি নিয়ন্ত্রণ: নির্দিষ্ট স্টপ-লস প্রতিটি ট্রেডে অতিরিক্ত ক্ষতি রোধ করে এবং টেক-প্রফিট অনুপাত বিভিন্ন অস্থিরতাপূর্ণ বাজারের জন্য সামঞ্জস্যযোগ্য।

- শক্তিশালী ভিজুয়ালাইজেশন: রিয়েল-টাইমে সাপোর্ট/রেজিস্ট্যান্স লাইন প্লট হয় এবং ট্রেডিং সিগন্যালগুলি স্পষ্টভাবে চিহ্নিত হয়।

- অ্যালার্ম ইন্টিগ্রেশন: অটোমেটেড ট্রেডিং সিস্টেমের সাথে যুক্ত করা যায়, যা বিভিন্ন ট্রেডিং পরিস্থিতির জন্য উপযুক্ত।

ঝুঁকি বিশ্লেষণ

- রেঞ্জ-বাউন্ড মার্কেটের ঝুঁকি: ট্রেন্ডহীন বাজারে ঘন ঘন মিথ্যা ব্রেকআউট ট্রিগার হয়ে একাধিক স্টপ-লস ঘটে। সমাধান: ADX বা EMA এর মতো ট্রেন্ড ফিল্টার ইন্ডিকেটর যোগ করা।

- প্যারামিটার সংবেদনশীলতা: pivotLen এবং volMultiplier বাজার অনুযায়ী সামঞ্জস্য করা প্রয়োজন। সমাধান: প্যারামিটার অপ্টিমাইজেশন এবং ওয়াক-ফরোয়ার্ড টেস্টিং করা।

- ভলিউম ল্যাগ: দামের গতিবিধির পরে অস্বাভাবিক ভলিউম দেখা দিতে পারে। সমাধান: অর্ডার বুক ডেটা ব্যবহার করা বা volSmaLength সংক্ষিপ্ত করা।

- গ্যাপের ঝুঁকি: ওপেনিং গ্যাপের কারণে স্টপ-লস লেভেল অতিক্রম করতে পারে। সমাধান: লিমিট অর্ডার ব্যবহার করা বা উচ্চ অস্থিরতার সময় এড়িয়ে চলা।

অপ্টিমাইজেশনের দিকনির্দেশনা

- ট্রেন্ড ফিল্টারিং: ADX>25 শর্ত বা 200EMA দিকনির্দেশনা ফিল্টার যুক্ত করে বিপরীতমুখী ট্রেড এড়ানো।

- ডায়নামিক প্যারামিটার: বাজারের অস্থিরতা (যেমন ATR) অনুসারে pivotLen এবং volMultiplier স্বয়ংক্রিয়ভাবে সামঞ্জস্য করা।

- গ্রেডেড টেক-প্রফিট: দুটি স্তরের টেক-প্রফিট সেট করা (যেমন ২% এ অর্ধেক পজিশন ক্লোজ, বাকি অংশ ট্রেলিং স্টপ-লসের সাথে রাখা) যা রিস্ক-রিওয়ার্ড রেশিও উন্নত করে।

- মেশিন লার্নিং অপ্টিমাইজেশন: ঐতিহাসিক ডেটা ব্যবহার করে volMultiplier এবং tpPerc প্যারামিটার অপ্টিমাইজ করার জন্য মডেল প্রশিক্ষণ দেওয়া।

- ক্রস-টাইমফ্রেম যাচাইকরণ: সিগন্যালের গুণমান বাড়ানোর জন্য উচ্চতর টাইমফ্রেমের S/R নিশ্চিতকরণ অন্তর্ভুক্ত করা।

সারসংক্ষেপ

এই কৌশলটি ট্রিপল ভেরিফিকেশন (মূল্য অবস্থান, ভলিউম, মূল্য আচরণ) এর মাধ্যমে একটি উচ্চ সম্ভাবনাময় ট্রেডিং ফ্রেমওয়ার্ক তৈরি করেছে, যা বিশেষ করে ট্রেন্ডের শুরুতে দাম ধরার জন্য উপযোগী। প্রধান সুবিধা হলো যুক্তি স্বচ্ছ, ঝুঁকি নিয়ন্ত্রণযোগ্য, তবে রেঞ্জ-বাউন্ড বাজারে এর সীমাবদ্ধতা লক্ষ্য রাখা প্রয়োজন। ভবিষ্যৎ অপ্টিমাইজেশনে প্যারামিটার অভিযোজন এবং ট্রেন্ড ফিল্টারিং এর মাধ্যমে স্থিতিশীলতা আরও বাড়ানো যেতে পারে।

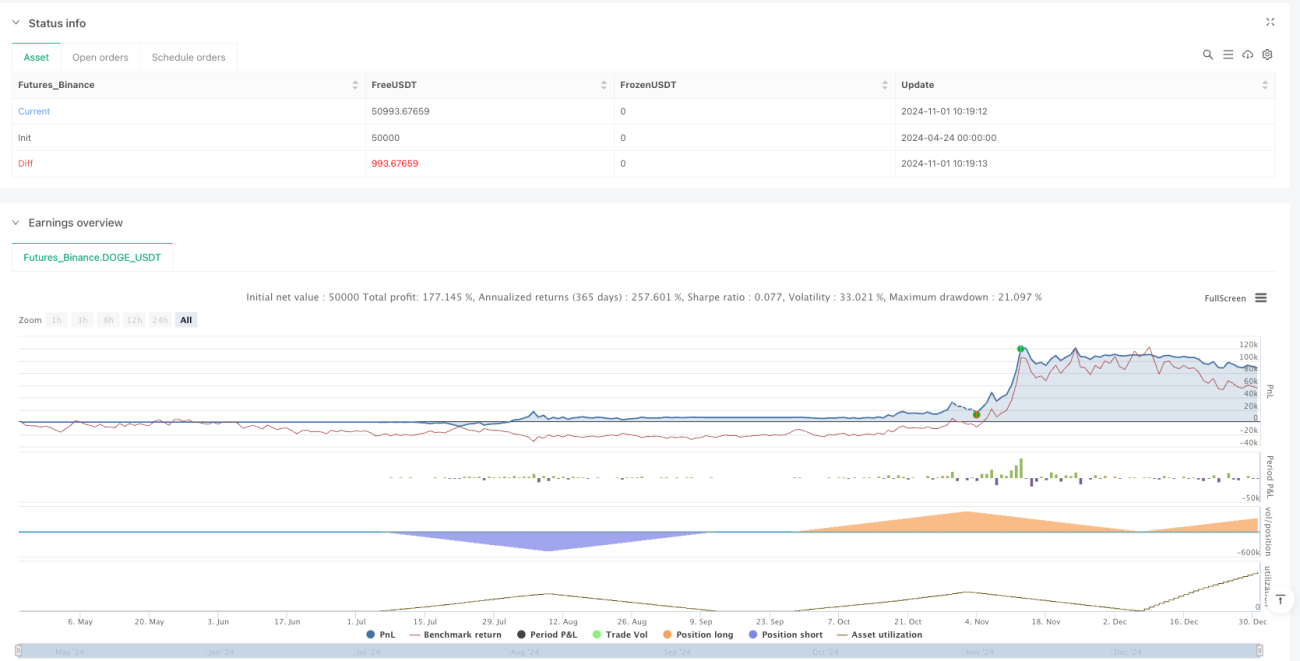

/*backtest

start: 2024-04-24 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=5

strategy("S/R Breakout/Reversal + Volume + Alerts", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===- 1