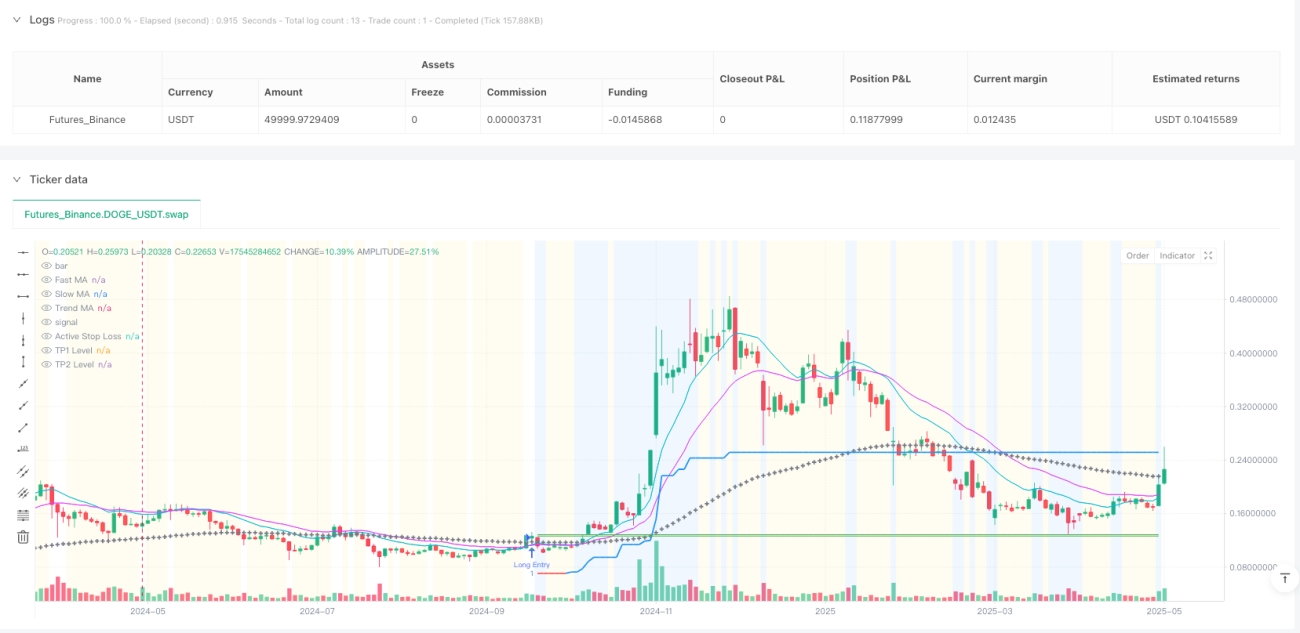

কৌশল সংক্ষিপ্ত বিবরণ

অ্যাডাপটিভ মোভিং এভারেজ ক্রসওভার ভোলাটিলিটি ট্র্যাকিং কোয়ান্টিটেটিভ ট্রেডিং স্ট্র্যাটেজি হল একটি পদ্ধতিগত কৌশল যা উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং এবং স্বল্পমেয়াদী অপারেশনের জন্য ডিজাইন করা হয়েছে। এই কৌশলের মূল ভিত্তি হল দ্রুত গতিশীল গড় (MA) এবং ধীর গতিশীল গড়ের ক্রসওভারকে প্রধান সিগন্যাল ট্রিগার পয়েন্ট হিসেবে ব্যবহার করা, পাশাপাশি একাধিক গুরুত্বপূর্ণ ফিল্টার এবং নির্ভুল ঝুঁকি ব্যবস্থাপনা টুল একীভূত করে ছোট কিন্তু দ্রুত মূল্য ওঠানামা ক্যাপচার করা। কৌশলটির কনফিগারযোগ্যতা অত্যন্ত উচ্চ; ব্যবহারকারীরা নমনীয়ভাবে গতিশীল গড়ের ধরন (EMA, SMA, WMA, HMA, VWMA) এবং তাদের সময়কাল প্যারামিটার নির্বাচন করতে পারেন যাতে বিভিন্ন বাজারের ছন্দের সাথে খাপ খাইয়ে নেওয়া যায়। উপরন্তু, এই কৌশলটি API-এর জন্য প্রস্তুত, স্বয়ংক্রিয় ট্রেডিং সিস্টেমে নির্বিঘ্নে একীভূত হয়ে সিগন্যালের দ্রুত সম্পাদন নিশ্চিত করে, যা উচ্চ-ফ্রিকোয়েন্সি ছোট লাভের জন্য প্রচেষ্টাকারী স্বল্পমেয়াদী ট্রেডারদের জন্য বিশেষভাবে উপযুক্ত।

কৌশলের নীতি

এই কৌশলের মূল লজিক নিম্নলিখিত গুরুত্বপূর্ণ অংশে বিভক্ত:

-

এন্ট্রি সিগন্যাল: প্রধানত দ্রুত গতিশীল গড় এবং ধীর গতিশীল গড়ের ক্রসওভার/ক্রসিংকে এন্ট্রি ট্রিগার শর্ত হিসেবে ব্যবহার করে। ব্যবহারকারীরা নমনীয়ভাবে গতিশীল গড়ের ধরন (EMA, SMA, WMA, HMA, VWMA) এবং সময়কালের দৈর্ঘ্য কনফিগার করতে পারেন সিগন্যাল সংবেদনশীলতা সামঞ্জস্য করতে এবং বিভিন্ন বাজার পরিস্থিতির সাথে খাপ খাইয়ে নিতে।

-

ট্রেন্ড ফিল্টার: কৌশলটি ঐচ্ছিকভাবে দীর্ঘমেয়াদী গতিশীল গড়কে বড় ট্রেন্ড ফিল্টার হিসেবে ব্যবহার করতে পারে, নিশ্চিত করে যে ট্রেডিং শুধুমাত্র বড় ট্রেন্ডের দিকেই পরিচালিত হচ্ছে, শক্তিশালী ডিরেকশনাল বাজারে কাউন্টার-ট্রেন্ড স্বল্পমেয়াদী ট্রেডিং এড়িয়ে।

-

কনফার্মেশন ফিল্টার:

- ATR ভোলাটিলিটি ফিল্টার: অত্যন্ত সমতল বা "নিস্তব্ধ" বাজারে এন্ট্রি স্থগিত করার জন্য ডিজাইন করা হয়েছে, যেখানে অস্থিরতা গতিশীল থ্রেশহোল্ডের (গড় ATR-এর উপর ভিত্তি করে) নিচে থাকে; এটি ট্রেন্ডবিহীন, কম শক্তির অবস্থায় ওয়াশিং এড়াতে সাহায্য করে।

- ভলিউম ফিল্টার: ন্যূনতম বাজার অংশগ্রহণের প্রয়োজনীয়তা (ভলিউম এবং তার গতিশীল গড়ের তুলনা) দ্বারা এন্ট্রি সিগন্যাল যাচাই করে, কম তারল্যের স্পাইক বা গুরুত্বহীন মূল্য আচরণের উপর ভিত্তি করে এন্ট্রি এড়ায়।

-

ঝুঁকি ব্যবস্থাপনা স্যুট:

- প্রাথমিক ভোলাটিলিটি স্টপ লস: ATR-ভিত্তিক প্রাথমিক স্টপ লস প্রতিটি ট্রেডের ঝুঁকি সংজ্ঞায়িত করার জন্য একটি বস্তুনিষ্ঠ সূচনা পয়েন্ট প্রদান করে, সাম্প্রতিক অস্থিরতার সাথে খাপ খাইয়ে নেয়।

- ATR ট্রেলিং স্টপ লস: গতিশীল বাজারের জন্য অত্যাবশ্যক; ট্রেলিং স্টপ লাইন অনুকূল মূল্য আন্দোলনের সাথে সামঞ্জস্য করে, সফল স্বল্পমেয়াদী ট্রেডের লাভ সুরক্ষিত করতে সাহায্য করে, পাশাপাশি উল্টো দিকে যাওয়ার সময় তুলনামূলকভাবে দ্রুত ক্ষতি কমানোর চেষ্টা করে।

- ব্রেকইভেন স্টপ লস (ঐচ্ছিক): TP1 পৌঁছানোর অথবা মূল্য নির্দিষ্ট ATR দূরত্ব সরানোর পরে, স্টপ লস স্বয়ংক্রিয়ভাবে এন্ট্রি মূল্যে (বাফার সহ) সরানো যায়, দ্রুত প্রাথমিক সাফল্য দেখানো ট্রেডের ঝুঁকি নিরপেক্ষ করতে।

- দ্বৈত লাভের স্তর: TP1 এবং TP2 দুটি লাভের লক্ষ্য নির্ধারণ করা হয়েছে; TP1 দ্রুত আংশিক লাভ (যেমন ৫০%) নেওয়ার জন্য ডিজাইন করা হয়েছে, আর TP2 বাকি অবস্থানের জন্য বৃহত্তর লাভের জায়গা তৈরি করে।

-

পজিশন ম্যানেজমেন্ট: স্থির পরিমাণ লট সাইজ ব্যবহার করা হয়, যা প্রতি ট্রেডে অবস্থানের আকারের উপর সুনির্দিষ্ট নিয়ন্ত্রণ নিশ্চিত করে; এটি উচ্চ-ফ্রিকোয়েন্সি পরিবেশে ধারাবাহিক ঝুঁকি প্রয়োগ এবং API কমান্ড জেনারেশনের জন্য অত্যন্ত গুরুত্বপূর্ণ।

কৌশলের সুবিধা

কোডের গভীর বিশ্লেষণের মাধ্যমে, এই কৌশলের নিম্নলিখিত স্পষ্ট সুবিধাগুলি রয়েছে:

-

উচ্চ কনফিগারযোগ্যতা: ব্যবহারকারীরা নমনীয়ভাবে বিভিন্ন প্যারামিটার সামঞ্জস্য করতে পারেন, যার মধ্যে গতিশীল গড়ের ধরন এবং সময়কাল, ফিল্টার সেটিংস এবং ঝুঁকি ব্যবস্থাপনা প্যারামিটার অন্তর্ভুক্ত, যা কৌশলটিকে বিভিন্ন বাজার পরিবেশ এবং ট্রেডিং শৈলীর সাথে খাপ খাইয়ে নিতে দেয়।

-

বহু-স্তরীয় ফিল্টারিং প্রক্রিয়া: ট্রেন্ড, ভোলাটিলিটি এবং ভলিউম ফিল্টার একত্রিত করে কার্যকরভাবে ভুল সিগন্যাল এবং বাজারের শব্দ কমায়, ট্রেডের গুণমান উন্নত করে।

-

সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: কৌশলটিতে একাধিক স্টপ লস প্রক্রিয়া (প্রাথমিক, ট্রেলিং, ব্রেকইভেন) এবং দ্বৈত লাভের লক্ষ্য নির্মিত, যা সূক্ষ্ম ঝুঁকি নিয়ন্ত্রণ এবং লাভ সুরক্ষা প্রদান করে।

-

API-বান্ধব ডিজাইন: স্পষ্ট এবং স্বতন্ত্র এন্ট্রি এবং এক্সিট লজিক দ্ব্যর্থহীন সিগন্যাল তৈরি করে, বহিরাগত ট্রেডিং সিস্টেমের সাথে একীকরণ সহজতর করে এবং প্রায় তাত্ক্ষণিক অর্ডার সম্পাদন সক্ষম করে।

-

সুনির্দিষ্ট পজিশন কন্ট্রোল: স্থির পরিমাণ লট সাইজ API এন্ডপয়েন্টের পেলোড সরল করে, স্বয়ংক্রিয় সম্পাদনকে আরও নির্ভরযোগ্য করে তোলে।

-

অভিযোজন ক্ষমতা: প্যারামিটার সমন্বয়ের মাধ্যমে, কৌশলটি উচ্চ-ফ্রিকোয়েন্সি স্বল্পমেয়াদী ট্রেডিং মোড থেকে দীর্ঘমেয়াদী ট্রেন্ড ফলোয়িং মোডে পরিবর্তিত হতে পারে, বিভিন্ন বাজার পরিস্থিতি এবং ব্যক্তিগত ট্রেডিং পছন্দের সাথে খাপ খাইয়ে নেয়।

কৌশলের ঝুঁকি

যদিও কৌশলটি সুনিপুণভাবে ডিজাইন করা হয়েছে, তবুও কিছু সম্ভাব্য ঝুঁকি এবং চ্যালেঞ্জ রয়েছে:

-

প্যারামিটার অপ্টিমাইজেশন ঝুঁকি: কৌশলটিতে অনেকগুলি কনফিগারযোগ্য প্যারামিটার থাকায়, অতিরিক্ত অপ্টিমাইজেশনের ফলে ব্যাকটেস্টের ফলাফল ভাল হতে পারে কিন্তু প্রকৃত পারফরম্যান্স খারাপ হতে পারে (ওভারফিটিং)। বিনিয়োগকারীদের উচিত আউট-অফ-স্যাম্পল ডেটায় যাচাই করা বা ফরওয়ার্ড টেস্টিংয়ের মাধ্যমে এই ঝুঁকি এড়ানো।

-

ট্রেডিং খরচের প্রভাব: উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং মানে বিপুল সংখ্যক ট্রেড; সঞ্চিত কমিশন এবং স্লিপেজ নিট লাভজনকতাকে উল্লেখযোগ্যভাবে প্রভাবিত করতে পারে। ব্যবহারের আগে সেটআপ এবং ব্যাকটেস্টে এই খরচগুলি সঠিকভাবে গণনা করা অপরিহার্য।

-

সিগন্যাল মানের ওঠানামা: বিভিন্ন বাজার পরিস্থিতিতে, গতিশীল গড় ক্রসওভার সিগন্যালের নির্ভরযোগ্যতা পরিবর্তিত হতে পারে, বিশেষ করে সাইডওয়ে রেঞ্জ বা অত্যন্ত অস্থির বাজারে।

-

প্রযুক্তিগত নির্ভরতা: API-প্রস্তুত কৌশল হিসেবে, এর কার্যকারিতা আংশিকভাবে সম্পাদনের গতি এবং প্রযুক্তিগত স্থিতিশীলতার উপর নির্ভরশীল; সিস্টেম বিলম্ব বা ব্যর্থতার কারণে সুযোগ হারানো বা সম্পাদনের বিচ্যুতি ঘটতে পারে।

-

মূলধন স্কেল সীমাবদ্ধতা: স্থির পরিমাণের পজিশন সাইজ সব অ্যাকাউন্টের আকারের জন্য উপযুক্ত নাও হতে পারে; ছোট অ্যাকাউন্টগুলি অত্যধিক ঝুঁকির মুখে পড়তে পারে, অন্যদিকে বড় অ্যাকাউন্টগুলি সম্পূর্ণ মূলধন ব্যবহার করতে সক্ষম নাও হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

কৌশল নকশা এবং সম্ভাব্য ঝুঁকির উপর ভিত্তি করে, এখানে কয়েকটি সম্ভাব্য অপ্টিমাইজেশন দিক রয়েছে:

-

অভিযোজিত প্যারামিটার: গুরুত্বপূর্ণ প্যারামিটারগুলি (যেমন ATR গুণক এবং গতিশীল গড় সময়কাল) বাজারের অবস্থার উপর ভিত্তি করে স্বয়ংক্রিয়ভাবে সামঞ্জস্য করার জন্য ডিজাইন করা, বিভিন্ন বাজার পর্যায়ে কৌশলের অভিযোজনযোগ্যতা উন্নত করে।

-

বুদ্ধিমান ফিল্টার বর্ধন: অতিরিক্ত বাজার অবস্থা সূচক (যেমন বাজার কাঠামো, অস্থিরতা প্যাটার্ন স্বীকৃতি বা সম্পর্কিত সম্পদের পারস্পরিক সম্পর্ক) একীভূত করে ফিল্টারের নির্ভুলতা আরও উন্নত করা।

-

গতিশীল পজিশন ম্যানেজমেন্ট: স্থির পরিমাণের পজিশনের পরিবর্তে অ্যাকাউন্টের আকার, বর্তমান অস্থিরতা এবং সাম্প্রতিক কৌশল কর্মক্ষমতার উপর ভিত্তি করে গতিশীল পজিশন ক্যালকুলেশন ব্যবহার, আরও বুদ্ধিমান তহবিল ব্যবস্থাপনা নিশ্চিত করে।

-

মাল্টি-টাইমফ্রেম কনফার্মেশন: বিভিন্ন টাইমফ্রেমে সিগন্যাল যাচাই করা, নিশ্চিত করা যে ট্রেডের দিক বড় বাজার কাঠামোর সাথে সামঞ্জস্যপূর্ণ, অপ্রয়োজনীয় ট্রেড হ্রাস করে।

-

মেশিন লার্নিং ইন্টিগ্রেশন: ঐতিহাসিক সিগন্যাল কর্মক্ষমতা বিশ্লেষণ করতে মেশিন লার্নিং অ্যালগরিদম ব্যবহার করা, ভবিষ্যতের সিগন্যালের সাফল্যের সম্ভাবনা পূর্বাভাস দেওয়া এবং উচ্চ-জয়রেট ট্রেডকে অগ্রাধিকার দেওয়া।

-

ট্রেডিং সেশন ম্যানেজমেন্ট: কম তারল্য বা উচ্চ অস্থিরতার সময় এড়াতে এবং বাজারের সবচেয়ে কার্যকর ট্রেডিং উইন্ডোতে ফোকাস করতে ট্রেডিং সময় ফিল্টার যুক্ত করা।

-

পারস্পরিক সম্পর্ক ফিল্টার: মাল্টি-অ্যাসেট ট্রেডিংয়ের জন্য, সম্পর্কিত বাজারের সাথে পারস্পরিক সম্পর্ক বিশ্লেষণ যুক্ত করা, নির্দিষ্ট ঝুঁকির কারণগুলির প্রতি অত্যধিক এক্সপোজার এড়ানো।

সারসংক্ষেপ

অ্যাডাপটিভ মোভিং এভারেজ ক্রসওভার ভোলাটিলিটি ট্র্যাকিং কোয়ান্টিটেটিভ ট্রেডিং স্ট্র্যাটেজি হল একটি পূর্ণাঙ্গ উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং সিস্টেম যা মোভিং এভারেজ ক্রসওভার সিগন্যালের মাধ্যমে ট্রিগার হয় এবং একাধিক গুরুত্বপূর্ণ ফিল্টার ও নির্ভুল ঝুঁকি ব্যবস্থাপনা টুল একীভূত করে, বিশেষ করে ছোট কিন্তু দ্রুত মূল্য ওঠানামা ক্যাপচার করার জন্য ডিজাইন করা হয়েছে। এই কৌশলের শক্তি তার উচ্চ কনফিগারযোগ্যতা এবং সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা কাঠামোর মধ্যে নিহিত, যা ট্রেডারদের তাদের ব্যক্তিগত ঝুঁকি সহনশীলতা এবং বাজার পরিস্থিতি অনুসারে ট্রেডিং প্যারামিটার সূক্ষ্মভাবে সামঞ্জস্য করতে দেয়।

উচ্চ-ফ্রিকোয়েন্সি ট্রেডারদের জন্য, এই কৌশলটি স্পষ্ট এন্ট্রি এবং এক্সিট লজিক, পাশাপাশি বহিরাগত সম্পাদন প্ল্যাটফর্মের সাথে নির্বিঘ্ন একীকরণের ক্ষমতা প্রদান করে, যা দ্রুত পরিবর্তনশীল বাজারে দ্রুত সিদ্ধান্ত সম্পাদনের জন্য অত্যন্ত গুরুত্বপূর্ণ। তবে, এই কৌশলটি ব্যবহার করার সময়, ট্রেডিং খরচ জমা হওয়া এবং অত্যধিক অপ্টিমাইজেশনের ঝুঁকির দিকে বিশেষ মনোযোগ দেওয়া উচিত, প্রকৃত ট্রেডিংয়ে কৌশলটির শক্ততা এবং লাভজনকতা নিশ্চিত করা উচিত।

সর্বশেষে, এই কৌশলটি একটি সুষম পদ্ধতির প্রতিনিধিত্ব করে - প্রযুক্তিগত সূচক এবং ঝুঁকি ব্যবস্থাপনা সরঞ্জামের শক্তি কাজে লাগানো, পাশাপাশি পরিবর্তনশীল বাজার পরিস্থিতির সাথে খাপ খাইয়ে নেওয়ার জন্য যথেষ্ট নমনীয়তা বজায় রাখা। সতর্ক প্যারামিটার সমন্বয় এবং ধারাবাহিক পর্যবেক্ষণ ও উন্নতির মাধ্যমে, এই কৌশলটি একটি পরিমাণগত ট্রেডিং পোর্টফোলিওর একটি মূল্যবান উপাদান হয়ে উঠতে পারে।

- 1